Talking Points:

- The final high-impact data release for this week saw U.S. GDP come-in at 2.6%, removing some pressure from the Dollar after yesterday’s Durables release.

- Next week is loaded with drivers for a number of economies. Below, we focus on three of the bigger global themes.

- If you’re looking for trade ideas, please check out our Trading Guides. And if you’re looking for shorter-term trade ideas, please check out our IG Client Sentiment.

To receive James Stanley’s Analysis directly via email, please sign up here.

Next week marks the open of August, and that means the first Friday of the month is circled for Non-Farm Payrolls out of the United States. But we have quite a bit of data to go through before we get there, as a rather busy schedule throughout much of the week can keep some of the more pensive macro themes on the move.

On Monday, we get European inflation figures, Tuesday brings a rate decision from the Reserve Bank of Australia followed by Euro-Zone GDP. On Thursday, we get a pivotal Bank of England rate decision, and this meeting will also see the bank update inflation forecasts, which will likely steal the show as it may signal just how dovish or hawkish the BoE might be after the recent ramp-higher in inflation. And on Friday – we get employment figures released concurrently from both the United States and Canada at 8:30 a.m. Eastern Time. So next week is fairly busy, and we’re coming off a week that saw considerable interest build around some rather pertinent items.

Recap of This Week

The big item on the calendar for this week was the FOMC rate decision on Wednesday. The bank made no move in rates, but the more pertinent item was the insertion of the phrase ‘relatively soon’ in reference to balance sheet reduction. This gives the appearance that the bank is ready to start balance sheet reduction as early as their next rate decision in September. The idea that the Fed might be looking to tighten the money supply via balance sheet reduction has hit rate expectations, as the concept of a dual-tightening mandate in the face of the slower growth and inflationary forces currently being seen in the United States doesn’t make much sense.

On that topic of growth and inflation – the Fed remarked on this in their statement accompanying the rate decision, and this helped to bring another gust of weakness into a heavily-oversold USD. And it’s that oversold nature of the Dollar that makes the potential for a turn a realistic idea at the moment, as a brutal 2017 has seen more than 10% shaved off USD, and sentiment has made an extreme shift after coming into the year heavily-long.

That additional wave of selling in the Dollar drove the Greenback down to fresh one-year lows while EUR/USD popped-up to fresh 2.5 year highs. The Aussie also continued a bullish move on the back of that Dollar weakness, breaking above the .80-level, albeit temporarily, to set a fresh one-year high. Below, we’re going to discuss three of the most pressing FX themes in a bit more depth while pointing to what could be the pertinent drivers for next week around each.

The Euro

The new 2.5 year high caught quite a bit of attention this week, and the run of strength in the Euro is a primary culprit for the troubling descent in the Dollar this year. As U.S. data has been coming in softer than expectations through much of the year, European data has started to surprise to the upside and we’re now seeing rate expectations move-higher. Traders have begun to shift rate-hike bets towards Europe as this stronger trend in the data alludes to the fact that we may soon see the ECB leave behind their stimulus program. This initial act of invoking ‘less loose’ monetary policy is a logical first step to tightening. And even though Mario Draghi has made numerous attempts to talk matters down, reiterating numerous times that the bank hasn’t yet discussed stimulus exit, markets seem to care little as the Euro has just continued to gain.

Next week is big for the Euro: The inflation figures released early Monday morning are very much the focal point, as this alludes to just how quickly the ECB may need to abandon stimulus in favor of tighter policy options. German unemployment and Euro-Zone GDP released on Tuesday will likely have some impact as well, although it will probably be a bit less than the focus we see paid to inflation figures. The bar for the Euro is relatively high as price action remains elevated, and the most trader-friendly scenario would likely be an in-line or slight miss on the inflation print on Monday to bring EUR/USD down to support. On the four-hour chart below, we’re looking at a series of potential support levels to follow as we move in to next week.

EUR/USD Four-Hour Chart with Potential Support Zones Applied

Chart prepared by James Stanley

The British Pound

Next week for GBP is all about the Bank of England. The BoE hosts their quarterly Super Thursday event on Thursday, and this rate decision will also be accompanied by an updated QIF (Quarterly Inflation Forecast) as well as a press conference from BoE Governor, Mr. Mark Carney.

The reason that this meeting is so important is because of Brexit. Ahead of the referendum, Mr. Carney took the unusual stance of voicing an opinion around a political matter, and this is pertinent because Central Banks generally stay far away for politics for fear of exactly what is happening. Mr. Carney said that a decision by British voters to leave the EU would bring about a whole host of unsavory events for the U.K. economy, such as a ‘sharp repricing’ in the value of the British Pound along with higher rates of unemployment and inflation and slower rates of growth. This dizzying scenario puts the Central Bank in a very awkward position because they have to make a very difficult choice at that point: Either a) cut rates to try to support growth and employment at risk of higher rates of inflation or b) hike rates to try to control inflation, even at the behest of growth and employment.

It wasn’t more than a week after the referendum that the Bank of England showed their hand. Mark Carney announced that the bank wasn’t taking risks around Brexit lightly, and would look to support the market with ample liquidity. In August, the BoE launched a bazooka of stimulus far before data could show any signs of slowdown from Brexit, and this helped to further crater the British Pound as investors had little confidence that the BoE’s overly-accommodative stance would change anytime soon.

GBP/USD Daily: Are We Seeing a Thematic Shift in the British Pound?

Chart prepared by James Stanley

But as the British Pound remained near lows for an extended period of time, in part due to both the overhang of Brexit as well as the ultra-dovish stance of the BoE, inflationary forces began to build. In May, the Bank of England reiterated their uber-dove stance at that Super Thursday announcement, but when inflation for the month was released later in June, pulses began to race that inflation may be getting out of control. Inflation for the month of May printed at 2.9%, and at the BoE rate decision following that print, we saw three votes for a rate hike, which would be the most at the MPC since 2011.

This inflation print combined with the three dissenting votes for a rate hike helped to bring some strength into Sterling as GBP/USD ran-above the vaulted psychological level of 1.3000. The interesting prospect here was whether or not we’d see the Bank of England pose a larger shift so that, eventually, we might able to forecast a rate hike for the U.K. economy. When Mark Carney himself opined on the matter in latter June, it seemed as though this was becoming a much more realistic prospect.

As we came into July, hopes were relatively high for a return of strength into the British Pound. But when June inflation figures were released below expectations, we saw that theme of strength soften as a bit of pressure was removed from the bank. On Thursday of next week, we get our first set of updated inflation forecasts since that spike-higher in inflation came-in, and the big question is whether or not we see a greater shift within the MPC looking for higher rates and, further, whether Mr. Carney might be ready to capitulate from the BoE’s uber-dovish stance.

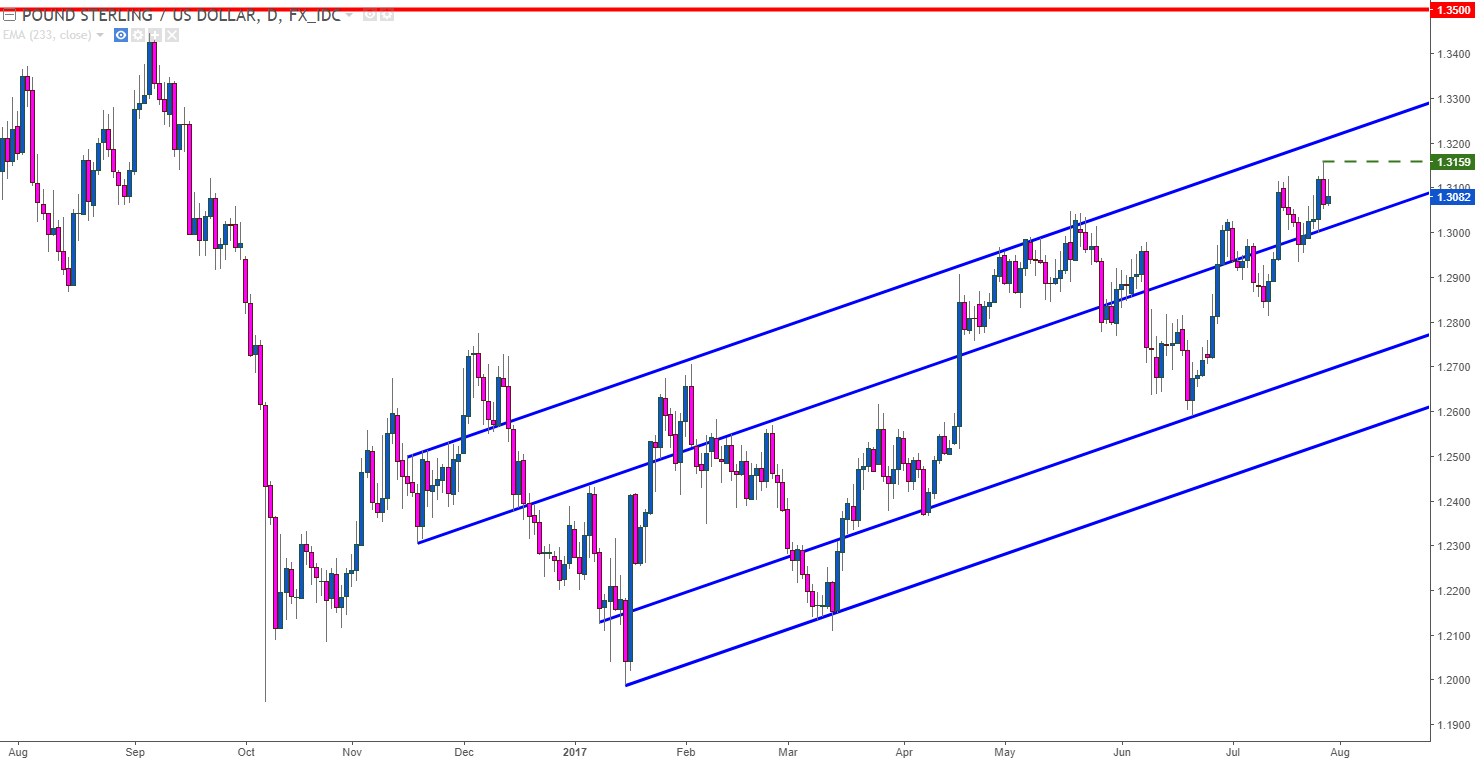

GBP/USD Daily: Emphasis on 2017 Trend-Channel Approaching Key Level of 1.3500

Chart prepared by James Stanley

The U.S. Dollar

The pain trade in the Dollar has continued for another week as the Greenback has now fallen by as much as 10.2% so far in 2017. The primary driver this week was the Fed as a fresh low was set following the rate decision, but as we’ve discussed from a few different angles– the focus for the Greenback appears to be squarely set on U.S. data. As we came into 2017 riding the wave of the ‘reflation trade’, expectations were jumping-higher for U.S. economic activity. This drove the U.S. Dollar to fresh 14-year highs, and that growth even began to show-up with key trade partners in Europe and Asia. But data so far out of the U.S. in 2017 has been unable to keep pace with those elevated expectations. This has removed some pressure from the higher U.S. rates theme, and after the Fed began talking about the prospect of balance sheet reduction in March, the Dollar has simply been unable to catch a bid. The apparent takeaway being that markets are dubious of the prospect of higher rates from the Fed along with balance sheet reduction.

This has driven the U.S. Dollar to deep oversold levels. Sentiment has gotten slammed-lower as this move has continued to develop for now almost a full seven months, and at this point, with such a meager showing on the demand side of the Dollar, it might not take much to create a bout of strength. Expectations are cyclical just like markets, and as U.S. data has disappointed throughout much of the year those expectations have begun to drop. The big question is if we’re at the point where data may be able to beat those lowered-expectations to bring any element of strength into USD.

Next week brings one of the more pertinent data points for U.S. markets with the release of Non-Farm Payrolls on Friday. The expectation is currently for 175k jobs to have been added in the month of July, but perhaps as important if not even more-so will be the impact on wages, as this is a direct precursor to inflation. If we see wage growth pose a strong showing, combined with a print above +175k, we could see USD-strength begin to show as a heavily-short market gets squeezed by higher prices. On the chart below, we’re looking at four potential resistance areas to follow in order to evaluate how well this theme is or is not showing.

U.S. Dollar Hourly Chart via ‘DXY’: Resistance Breaks to Highlight Bullish Price Action

Chart prepared by James Stanley

--- Written by James Stanley, Strategist for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX