Global market mood soured last week, extending a slump since November. On Wall Street, Dow Jones, S&P 500 and Nasdaq futures slipped 0.89%, 1.42% and 2.25% respectively. The VIX market ‘fear gauge’ closed at its highest since February. In the Asia-Pacific region, the Nikkei 225, Hang Seng and ASX 200 dropped 1.98%, 1.27% and 2.20% respectively. Conditions were relatively tame in Europe, with the FTSE 100 gaining 0.39% as the DAX 40 fell 0.67%.

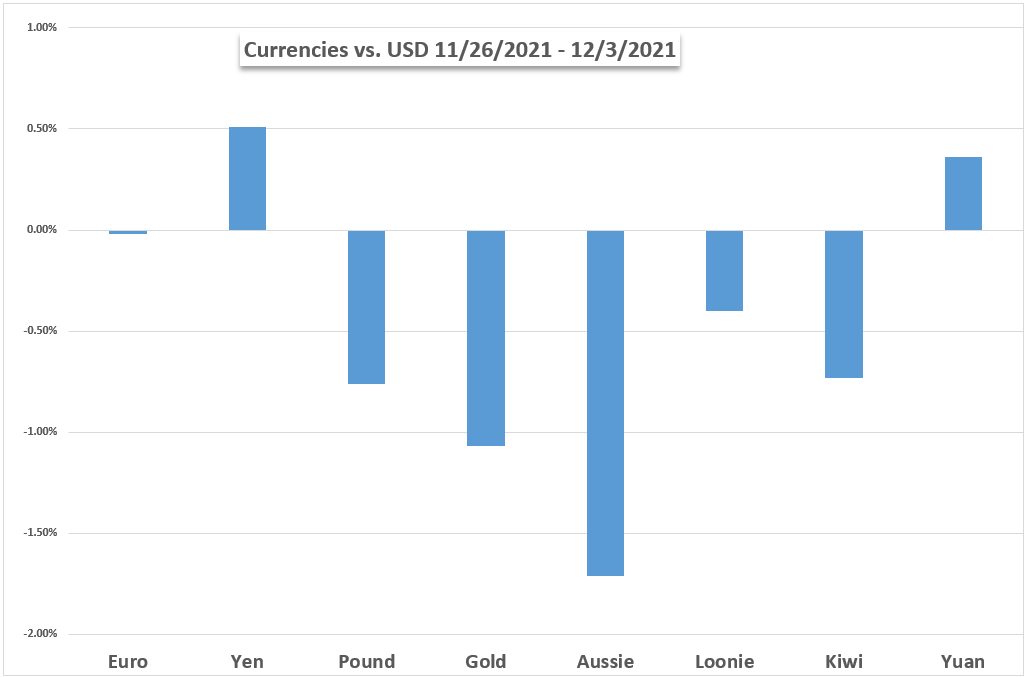

Risk aversion meant that forex traders flocked into the safety of the highly liquid US Dollar, which soared against the Australian and New Zealand Dollars. The similarly-behaving Japanese Yen and Swiss Franc also outperformed. Taking a look at commodities, growth-linked crude oil prices softened, extending a bear market. Gold prices managed to hold some ground, capitalizing on a further decline in longer-term Treasury yields.

Driving the worrying mood in sentiment appears to be a combination of the emerging Omicron Covid-19 variant and the Federal Reserve’s hawkish pivot. This past week, Chair Jerome Powell retired the word ‘transitory’ from describing inflation estimates. Policymakers at the central bank have also expressed the possibility for tapering quantitative easing faster than anticipated. This follows persistently elevated inflation readings in the world’s largest economy.

Speaking of inflation, the US will release the next CPI report on December 10th. Headline inflation is expected at a whopping 6.8% y/y in November, up from 6.2% in October. That would be the highest rate in almost 40 years. The core reading, which excludes energy and food items, is estimated at 4.9% y/y from 4.6% prior. Further upside surprise could increase hawkish Fed policy bets for 2022, risking volatility in markets.

Outside of the US, AUD/USD traders will be eyeing the Reserve Bank of Australia’s last interest rate decision of the year. For USD/CAD investors, the Bank of Canada is also on tap. Both central banks are not expected to adjust benchmark lending rates, so investors will be tuning in to gauge their outlook for 2022 and how policy could shape up. Meanwhile, Chinese stocks that are listed on US exchanges continue bracing for volatility on delisting concerns. What else is in store ahead?

US DOLLAR WEEKLY PERFORMANCE AGAINST CURRENCIES AND GOLD

Fundamental Forecasts:

US Dollar Fundamental Forecast: DXY Primed Ahead of CPI Data

The US Dollar index closed higher for the sixth consecutive week as fundamental tailwinds buoy the Greenback. This week’s CPI data may push the Greenback higher.

Euro Week Ahead Forecast: EUR/USD Bounce May Be Over Already

EUR/USD was relatively stable last week but it is still hard to see a stronger recovery unless the European Central Bank reverses its position that a tightening of Eurozone monetary policy is not necessary.

Gold Makes Third Successive Weekly Decline As General Market Sentiment Whipsaws

Gold, much like many other markets this week, witnessed a change in sentiment as Omicron fears and questions over aggressive tapering bets eased.

GBP Forecast: Omicron Adds Uncertainty to BoE Rate Rise

Scientific data on vaccine efficacy a trigger for a BoE rate rise this month.

Australian Dollar May Wobble on RBA Rate Decision, Omicron Variant and US CPI

The Australian Dollar remains vulnerable ahead of the last RBA rate decision of 2022. The Omicron Covid-19 variant poses a risk if strict lockdowns ensue. Will AUD/USD’s decline extend?

USD/CAD Outlook Hinges on Bank of Canada (BoC) Rate Decision

The Bank of Canada’s (BoC) last interest rate decision for 2021 may keep USD/CAD afloat as the central bank is expected to retain the current policy.

S&P 500 Weekly Forecast: Omicron Fears May Weigh on US Stocks; Reopening Trade at Risk

U.S. stocks, particularly the reopening basket, may come under more pressure in the near term as traders trim positions in risk assets amid omicron variant uncertainty and fragile sentiment.

USD/JPY on the Cusp of Reversal as All Yen Crosses Yield to Risk Trends

The volatility that has stirred in the broader financial markets doesn’t full encompass the retreat in a range of ‘risk’ assets that we have seen for some weeks. That erosion has hit many of the Yen crosses, but the recent volatility and rate forecast uncertainty now threatens USDJPY.

Technical Forecasts:

Gold Price Forecast – XAU/USD Testing Big Level of ‘Hidden’ Support

Gold has been generally weak and at a big level; a price pattern on the short-term chart is seen as dictating the next move.

Dow, Nasdaq 100, S&P 500 Forecasts for the Week Ahead

Stocks stumbled as Omicron and FOMC policy became focal points, and this may lead to a deeper pullback as equities incorporate these new risk factors.

Crude Oil Drops a 6th Straight Week Amid Extreme Volatility

Crude oil managed to stabilize its dramatic bearish trend this past week, but the current continues to carry the commodity lower. The tipping point for this commodity stands very prominently at 62.50/61.50.