S&P500, Dollar, Treasury Yield, Gold, EURGBP and USDJPY Talking Points

- We are entering Tuesday with a distinct run of risk aversion that sent the US indices to sharp intraday reversals – leaving SPX with its biggest upper wick in 7 months

- USDJPY has charged to multi-year highs with a broad Yen cross rally fed by carry trade, but the Dollar has struggled to break elsewhere despite a surge in Fed rate forecasts

- Top event risk for the coming 48 hours includes US inflation data, critical IMF updates for the globe and the start of the US earnings season

Risk Aversion Due To – Or In Spite Of – Firming Monetary Policy Forecasts

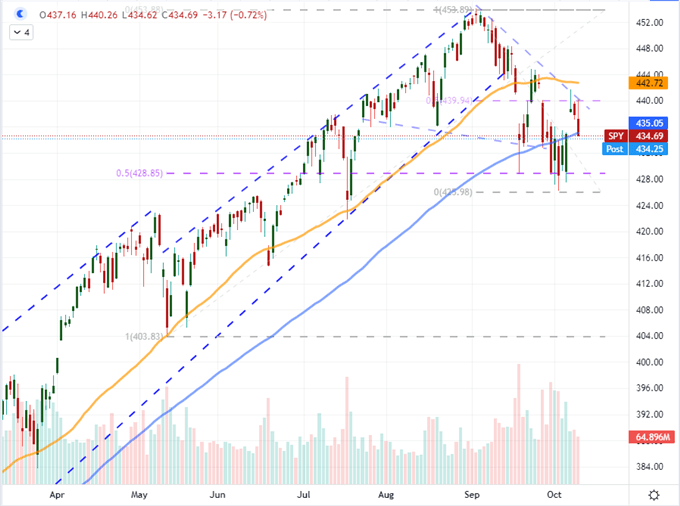

The opening session of the trading week took a notable turn for the worse as the US session took control of the yoke. Through the first 16 hours of the Monday’s trading session, there was a tentative bullish bearing to the speculative backdrop that overrode the uncertainties of last week’s NFPs and the tangible recognition that monetary policy was firming across the board. With a light economic docket, we could have squeezed out an even more productive drift, but the US session turned the ship. US indices took a dive which amplified latent concern around US interest rate forecasts and anticipation for growth updates from the IMF among other scheduled event risk. On a sentiment basis, there was a notable consistency in the sentiment swoon that we experienced through this past New York session, but critical self-sustaining momentum has yet to solidify itself. While there are many comprehensive measures of sentiment, the S&P 500’s slide back below 4,380 with the biggest ‘upper wick’ (daily bearish reversal sign) in 7 months stands out. With the proper fundamental motivation, we may see this turn spark a genuine trend; but I would not set my expectations on that course setting just yet. Perhaps the heavy event risk ahead will solidify the move.

Chart of SPY S&P 500 ETF with 50 and 100-Day Moving Averages with Volume (Daily)

Chart Created on Tradingview Platform

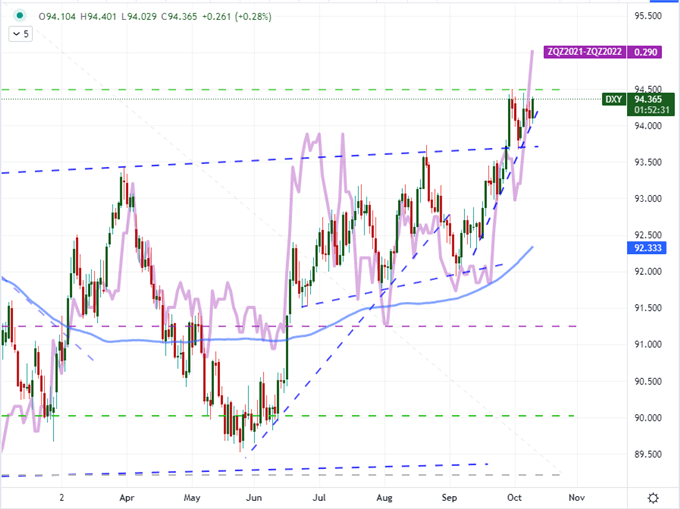

The cracks in the foundation of over-extended risk appetite are many, but monetary policy may be the most systemically unsettling. Most notably, the US interest rate forecast found the greatest charge through the opening session of the week. An extension of the hawkish build up through the end of last week, the Fed forecast through 2022 jumped another 2.5 basis points. Without context that may not be very impressive, but we have seen in a week’s time the probability of a single 25 basis point rate hike from the Fed rise from approximately 70 percent to certainty with an additional 16 percent chance of two hikes. That is certainly a source of deep concern for investors who have relied on the belief that the world’s central banks would act as backstops for extravagant risk taking at any sign of trouble (otherwise known as ‘moral hazard’). That said, it is notable that despite the hawkish interpretation of our bearings on the ‘risk’ side, the Dollar has not benefit their perspective either through its relative yield advantage nor its safe haven status.

Chart of DXY Dollar Index Overlaid with Fed Forecasts 2022 (Daily)

Chart Created on Tradingview Platform

Monetary Policy as a Theme

As we move into a more active fundamental docket through the next 48 hours, my priority list will remain fixed on the relative aspects of monetary policy. That is owing to the fact that it is a more global theme with many of the individual events tracing back to its particular influence. While there is a lot of attention paid to the relative course settings of a central bank like the Fed relative to the intentions of the Bank of Japan, I believe the greater market moving capacity is in the collective shift in policy and its influence over risk trends. While the market’s boosts its forecasts for Fed rate forecasts, we have also seen the RBNZ hike while speculation over a BOE and BOC first hike grow heartier by the month. Do not underestimate the effect that a tipping point of ‘dovish’ to ‘normalizing’ monetary policy views can have of the global financial system.

Poll: Which Major Central Bank Will be the First To Hike?

Poll from Twitter.com, @JohnKicklighter

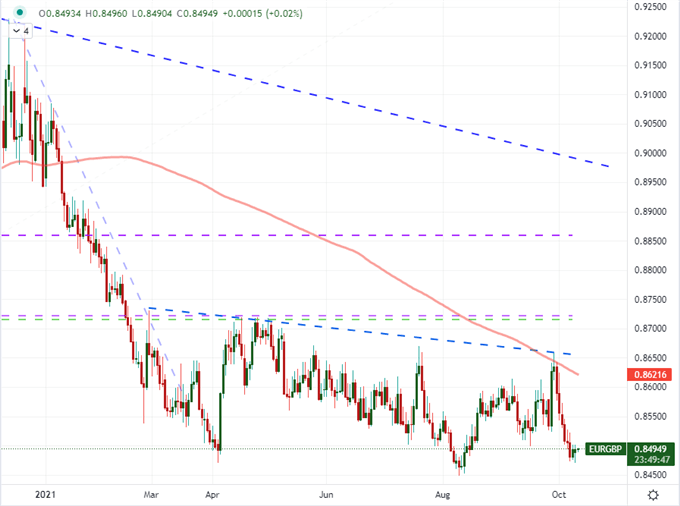

As much potential exists in monetary policy speculation, not all updates are going to lead to a distinct and long-lasting speculative charge for relevant capital market benchmarks and currencies. The recent RBNZ rate hike didn’t translate into an immediate rally for the Kiwi Dollar and there has been little trend to speak of since. More recently, the Bank of England’s outlook seems to have received a material upgrade to its intent according to market pricing. Looking to swaps, the probability that the BOE will hike this year – rather than the prevailing forecast of February which we had escalated to just recently – has climbed following the remarks of a few central bank officials and their concerns over persistent inflation. While GBPJPY certainly rallied, that seemed to be more the by-productive of the Yen’s tumble than the favorable winds for the Sterling. In fact, EURGBP actually rose this past session even though the ECB has taken pains to present a dovish façade to the global markets.

Chart of EURGBP with 200-Day Moving Average (Daily)

Chart Created on Tradingview Platform

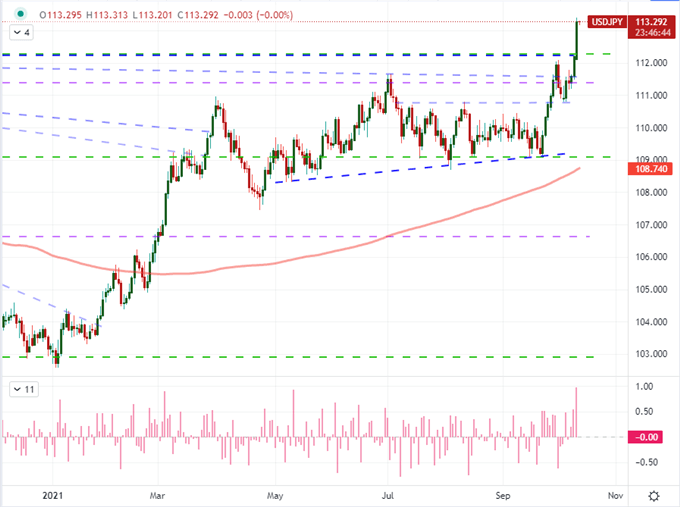

USDJPY Leads the Charge - But We Need a Movement, Not Just a Leader

There was some notable market movement to open this week, but nothing that I would highlight as a definitive signal of intent in a more macro perspective. One of the more remarkable developments for me was the rally in the Yen crosses. GBPJPY managed to break a multi-year trendline resistance which seemed to align to the BOE commentary, but it was the USDJPY that truly impressed. The charge through 112.25 cleared range resistance stretching back years. That said, it wasn’t clear that this was a broad risk appetite move nor a Dollar bid – as evidenced above. That matters because follow through need to have foundations that will continue to play through. How likely is it that this one trend continues in direct contrast to broader uncertainties?

Chart of USDJPY with 200-Day SMA and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

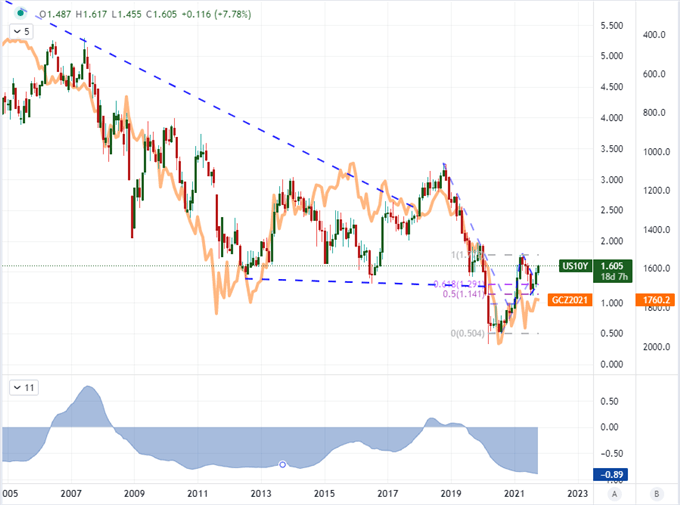

While the Dollar and Sterling may not be immediately conforming to their respective interest rate bearings, it is a trend that is likely to take over control eventually should it persist. And, while I will be watching the US, UK and New Zealand currencies as leading players on the ‘hawkish’ side of scale, this isn’t my only interest around this thematic matter. Putting aside the abstract perspective of risk assets, I believe Gold is one of the most sensitive assets to the normalizing of extreme accommodation. Below is a monthly chart of the US 10-year Treasury yield (a sensitive gauge for US interest rate forecasts) overlaid with an inverted gold chart. The 5-year rolling correlation chart between these two is the most extreme that it has been on record. In other words, if interest rate forecasts continue to rise, we may soon see an end to the metal’s bull trend.

Chart of US 10-Year Yield Overlaid with Gold Futures (Monthly)

Chart Created on Tradingview Platform

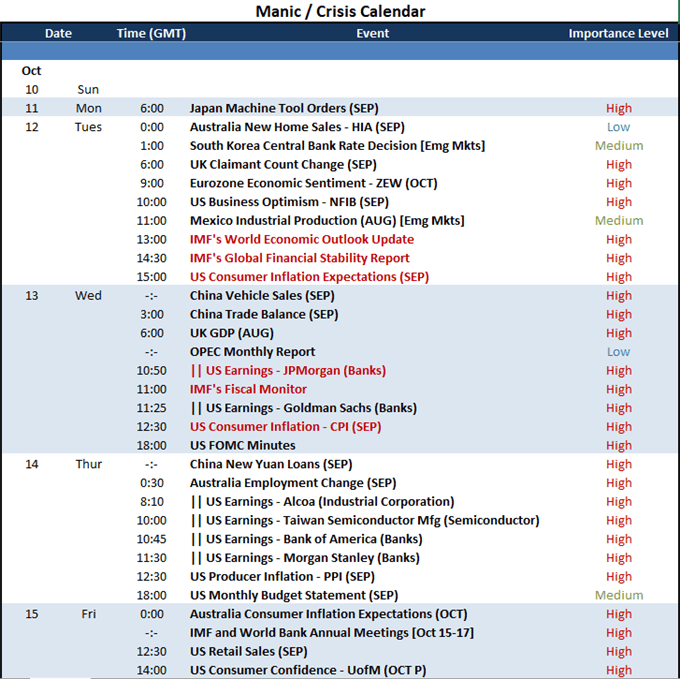

Interest rate forecasts will be a top consideration for me over the next 48 hours of the trading week. While there is plenty of off-docket potential from headlines, the US consumer inflation expectations and CPI data for September will be of principal interest. These are the market’s favorite data points to consider the price aspect to the Fed’s dual mandate. If the pressure continues to build, we may find a more tangible bull trend develop in risk assets like the SPX and find the Dollar’s combo safe haven and yield advantage appeal push a genuine rally. Other themes to watch over the coming two sessions are the IMF’s updates on growth forecasts, global financial stability and fiscal health as well as the start of the US earnings season starting with JPMorgan and Goldman Sachs.

Calendar of Major Event Risk

Calendar Created by John Kicklighter