Talking Points:

- As we move towards the Jackson Hole Economic Symposium, the prospect of Quantitative Tightening becomes closer to reality, and this has the potential to create a change in conditions across global markets.

- After the Fed’s last meeting in July, we’ve seen a bit of stability show in the U.S. Dollar, but this has also brought a bit of pressure to U.S. stocks. This is something European equities have been facing for a few months now, and we look at the prospect of reversals in four markets below.

- If you’re looking for trade ideas, check out our Trading Guides. And if you’re looking for shorter-term ideas, please check out our IG Client Sentiment.

To receive James Stanley’s Analysis directly via email, please sign up here.

Since the beginning of August, we’ve seen a slight bit of change in global markets. The U.S. Dollar has been steadily building on a series of higher-lows, so while bulls haven’t exactly taken-over here, we have seen bearish drive begin to recede. And while the Dollar appears to be *trying* to carve out a bottom, global stocks have started to move-lower. Tomorrow marks the start of the Jackson Hole Economic Symposium, and on the top of traders’ minds will be the prospect of Quantitative Tightening. Quantitative Tightening, or ‘QT’ for short, is basically the opposite of QE. While QE is used to add liquidity to a market in times of duress as a form of additional accommodation, essentially by flushing the financial system with cash while removing bonds (sterilized QE), QT is the process of removing that liquidity.

Since March, this has been the elephant in the room for the Federal Reserve. The bank said that they were looking at starting balance sheet reduction, or QT, by the end of the year, and since then – the U.S. Dollar has gotten crushed as investors appear skeptical of the Fed’s ability to continue hiking rates whilst also tightening liquidity via balance sheet reduction. This is likely at least a contributing factor to the Dollar’s more than 10% decline so far in 2017.

Over the past few months, the Fed has grown more vocal around balance sheet reduction. At the bank’s last rate decision, in July, they said that they envision starting balance sheet reduction ‘relatively soon’. Markets inferred that to mean September, or the Fed’s next rate decision. Since then, we’ve seen a bit of pressure develop in equities.

Why Might This Matter?

Bond prices. When a Central Bank announces that they’ll be constant buyers of bonds, bond traders get a gust of wind behind their sails as one of the biggest possible participants in a market openly-announces that they’re going to get long. This additional demand pushes bond prices higher (and yields accordingly lower); and for traders in these markets, that extra demand coming from the Central Bank provides a pretty comfortable backdrop for holding a position. This is why most of the Euro-weakness around ECB QE was priced-in far before a single Euro of ECB money was spent on bond purchases (in early March, 2015).

But when that demand reverses, via QT, bond markets lose a key element of support. And traders in fixed income are as proactive as any other market if not more so; and the simple fact that this support is being removed can portend a chain of selling as investors look to ‘get out of the door at the same time’. This disconnect can create worry in other markets, like stocks, and this is likely at least partly responsible for the pullback that we’ve seen in global equities so far in August. Below, we’re looking at four of the bigger equity markets out of Europe and the United States to look at the prospect of a continued reversal.

The S&P 500 remains elevated by a number of different metrics. But this isn’t anything new, and valuation isn’t necessarily a short-side trigger. U.S. stocks are expensive by many metrics, but as Chair Yellen has opined in the past, given the current backdrop for monetary policy and rates, stock valuations aren’t necessarily too outlandish. But –we also know that the Fed wants to make that backdrop less comfortable or forgiving in the effort of moving the U.S. economy away from ‘emergency-like accommodation’.

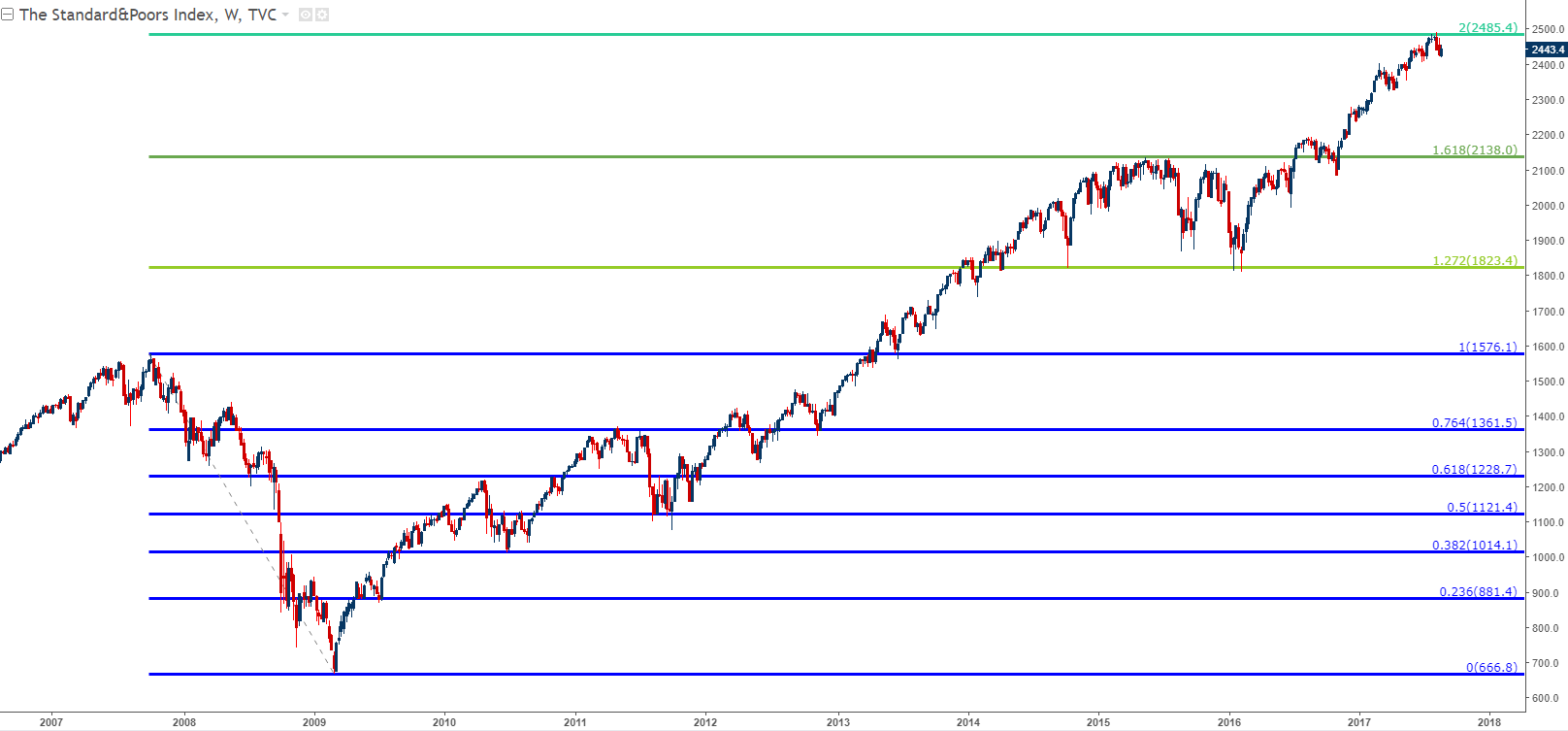

Since early August, the S&P has had a difficult time setting new highs. This is somewhat of an abnormality given the past few months as U.S. stocks were continuing to trudge higher. Current resistance is showing at an interesting level around 2485, which is the 100% measured move of the Financial Collapse.

S&P 500 Monthly Chart: Resistance at 100% Measured Move from Financial Collapse

Chart prepared by James Stanley

Since that resistance came into play in early-August, price action in the S&P 500 has been moving lower. The psychological level at 2,400 is interesting, and a break-below can open the door for short-side strategies with targets cast towards prior support levels (shown below in red).

Chart prepared by James Stanley

Nasdaq 100

The move in U.S. tech stocks has been a little cleaner when matched up with this recent them around the Fed. The Fed’s most recent rate decision was on July 25-26. The morning of the 27th, the Nasdaq 100 gapped-up to a new high, but has since continued to move-lower. Tech is often the eye of the storm when we see reversals or sell-offs, as the slower economic backdrop is generally a bit less forgiving to low-margin, high cash burn tech companies.

Nasdaq 100 Monthly: Current Resistance at the 27.2% Extension of the ‘Dot Com Bust’

Chart prepared by James Stanley

The pullback since that last FOMC meeting has created a bearish channel in the Nasdaq 100. This would still be a bull flag formation as the bullish trend remains intact. But a break below May/July support around 5564-5585 would open the door for ‘bigger picture’ short themes.

Nasdaq 100 Hourly: Bearish Channel After July FOMC

Chart prepared by James Stanley

German DAX

While U.S. stocks have been supported with the backdrop of a falling Dollar thus far in 2017, matters haven’t been so kind to European issues. While the Dollar has continued to drop dramatically, the Euro has continued its top-side run, and this has started to impact European equities.

Similar to the S&P 500, the DAX is currently seeing resistance at the measured move of the financial collapse, and this resistance has held for the past few months after first coming into play in May of this year.

DAX Monthly: Resistance at 100% Measured Move of Financial Collapse

Chart prepared by James Stanley

France - CAC 40

Earlier in the year, it appeared as though the stage was set for a run of strength in French stocks after the prospect of a Marine Le Pen presidency faded into the background. But alas, after the bullish breakout in March and April, buyers were unable to continue pushing prices higher, and as Euro strength became more of a concern, French stocks have started to channel lower. On the monthly chart below, we’re looking at that previous breakout around French elections earlier in the year.

CAC 40 Monthly: Bullish Breakout Unable to Continue as Euro Strength Rages

Chart prepared by James Stanley

The past 3.5 months have seen the CAC 40 trend-lower within a relatively consistent bearish channel, giving us a longer-term bull flag formation.

CAC 40 Daily: Bull Flag Formation Building Past 3.5 Months

Chart prepared by James Stanley

--- Written by James Stanley, Strategist for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX