AUD/USD, EUR/USD, USD Analysis & News

- Euro Talked Down by ECB

- US Dollar Heading Higher Ahead of FOMC

- AUD Fails to Find Support From Firmer Inflation

QUICK TAKE: ECB Elevating Currency War Risks, Retail Traders Claim Short Squeeze Victory

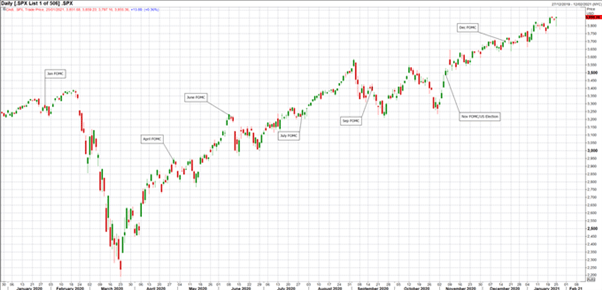

Equities: In recent weeks and particularly this week, market exuberance stemming from the retail side has been garnering attention, raising concerns of elevated bubble risks.The PBoC have also grown concerned over asset bubbles with the central banks advisor stating that bubbles will remain (in the stock or property market) if China does not shift its focus. In turn, the PBoC have drained a net CNY 178bln via open market operations over the past two sessions. That said, the increasing sense of a frothy market is somewhat similar to last June, where the announcement of company bankruptcies resulted in shares soaring, the prime example being Hertz. The graph below shows last years Fed meeting’s (excluding March crisis meetings) and the subsequent price action in the S&P 500. Notably, the post-June meeting saw a sharp 6-7% drawdown.

S&P 500 AND FOMC MEETINGS

Source:Refinitiv

Euro Stoxx 50 Sector Breakdown

Outperformers: Consumer Staples (-0.9%), Healthcare (-1.1%), Real Estate (-1.2%)

Laggards: Utilities (-2.8%), IT (-2.2%), Financials (-2%)

US Futures: S&P 500 (-1.1%), DJIA (-1%), Nasdaq 100 (-0.%)

Intra-day FX Performance

Source: Refinitiv

EUR: The Euro is under pressure this morning following surprisingly dovish comments from ECB’s Knot, going against his typically more hawkish stance. The ECB member stated that Euro strength will take prominence for the ECB if it threatens inflation outlook, adding that they have the tools to act on Euro strength. Alongside this, Knot stated that the ECB had not reached the lower bound and that there was still room to cut rates. That said, renewed rhetoric of the Euro is somewhat of a surprise given that the ECB had seemingly cut back on their commentary on the currency at last week’s meeting. However, the comments from Knot does come after yesterday’s source reports that the ECB would study the impact of ECB vs Fed policy on exchange rates.

USD: While the media are placing their attention to the seismic gains across retail trading favourites (AMC and Gamestop), broader markets have been de-risking ahead of the FOMC with the VIX creeping higher up and breaking above its 200DMA, which in turn has seen the USD on the front-foot. For analysis on the Fed, click here.

AUD: The Australian Dollar has failed to benefit from the higher than expected inflation figures overnight with the currency breaking below 0.7700 as weaker risk sentiment weighs. The headline figure rose 0.2ppts to 0.9% (Exp. 0.7%), however, the RBA’s preferred trimmed mean measure rose in line with expectations at 1.2%. That said, I still favour an extension in the move lower in AUD/NZD

Looking ahead focus is on the FOMC meeting with corporate earnings from Apple, Facebook, Telsa due after the US close.

REPORTS OF NOTE

- US Dollar Technical Outlook Turning Positive: USD Charts to Watch by Paul Robinson, Strategist

- British Pound (GBP) Latest: GBP/USD Highest Since May 2018, Uptrend Intact by Martin Essex, MSTA, Analyst

- Crude Oil Price Grinding Back to Multi-Month High on Positive Fundamentals by Nick Cawley, Strategist