EURUSD, SPDR S&P 500 ETF, Ukraine, US Dollar and CADJPY Talking Points

- The Trade Perspective: SPY Rang Between 440 and 420; CADJPY Bearish Below 91.50; EURUSD Bullish Above 1.1000

- Russia’s invasion of the Ukraine continues and so do the West’s sanctions, but risk measures like US indices aren’t ready to simply collapse

- The Dollar is trading off its role as safe haven amid bouts of extreme concern and a carry benefactor as Powell warns hikes are still on the menu

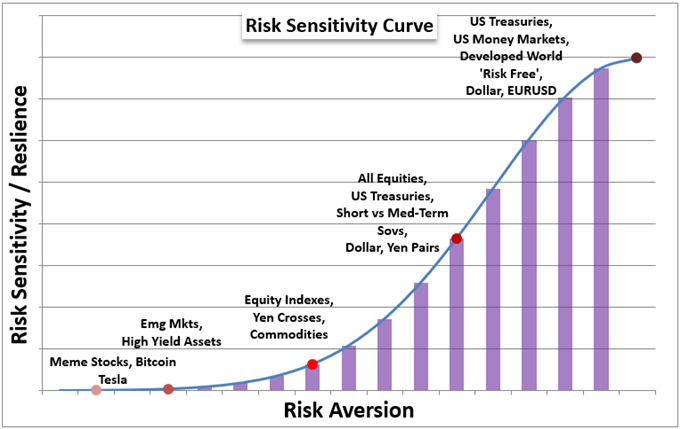

A Reflection of Risk Trends

Typically, I prefer to gauge the market’s current bearings around risk trends through the performance of the US indices; but I think the EURUSD may be a better barometer at the moment. As far as sensitivity to every ebb and flow in confidence unfolds, there are far more reactive measures via meme stocks or crypto, but it is important to extract the signal from the noise. To a significant extent, the US indices are far better measures of intent for my own analysis. In recent years, the likes of the S&P 500 and Nasdaq 100 have proven particularly notorious for tracking out significant ‘risk off’ moves as there has been an unshakable speculative appetite infused into this particular market. Yet, as overwhelming as the ‘buy the dip’ mentality may be for the popular benchmarks, there is a readiness to move with significant sentiment moves. When its comes to the risk spectrum, we don’t expect the likes of the Dollar and EURUSD to show a distinct speculative connection unless the winds are severe. So, the recent slide from the benchmark cross should raise some serious questions from speculative observers who have been too willing to play down the elevated S&P 500 ATR and the implied-based VIX index.

Chart of Risk Trend Intensity

Chart Created by John Kicklighter

I think there is a lot of reticence to the notion that we are seeing a market pining for a ‘safe haven of last resort’ – essentially the litmus test for the Dollar’s safe haven status. Considering there isn’t a progressive deleveraging across US indices – much less global speculative assets – it would seem unreasonable to gauge serious risk aversion. However, the realized volatility in measures like the S&P 500 tell a different story. The instability in the financial system is almost as unnerving as a productive slide from the markets-at-large. We pick up on that haven demand in the choppy progress from the Greenback. The DYX Dollar Index has edged higher to multi-month highs which has in turn translated into EURUSD’s drop to and below 1.1100. There is some serious technical weight that we are moving into with this slide. More than just a symbolic move and 10-month low, this benchmark cross is moving into support (in the 1.10 to 1.09 area) that represents the floor of a lifetime wedge for this relatively young pair. So, while I’ll be watching this pair’s interest rate disparity for guidance, the bearing for risk appetite will earn an equal place at the table for me.

Chart of EURUSD with 10-Day ATR (Daily)

Chart Created on Tradingview Platform

What is Driving the Markets

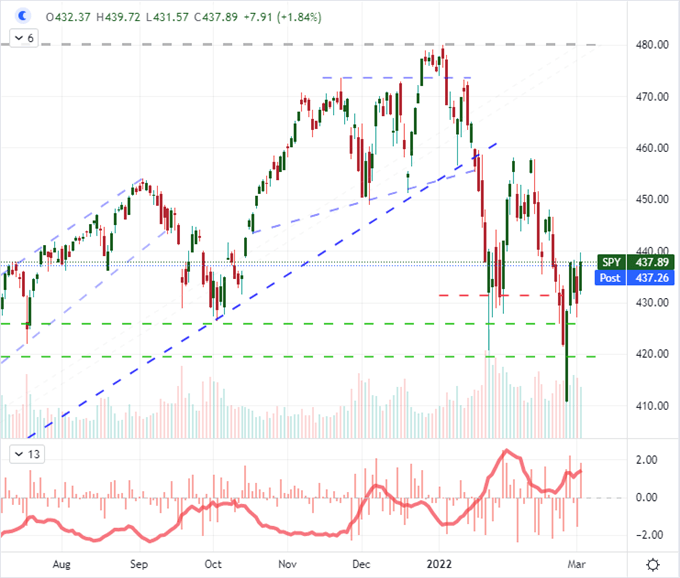

Putting aside the EURUSD’s pressure this past session, there was a more encouraging view of risk assets to be drawn across the spectrum this past session. Notably, the S&P 500 gained 1.8 percent while the Nasdaq 100 and Dow were more on the order of a 1.7 percent climb. That is impressive performance and it was loosely backed by other sentiment measures like global equities, emerging market assets and carry trade. That said, there isn’t much in the way of progress to champion in any of the major risk-leaning measures. From the SPDR S&P 500 ETF below, we can see that the robust close-over-close advance didn’t do much in the way of clearing overhead. We are simply seeing the ill-effects of sustained, high volatility. This situation only pushes me deeper into my inherent skepticism. Where would the bullish handholds come for market participants? A relief rally from tamed Ukraine actions and/or moderation in hawkish monetary policy could offer a boost, but nether is currently playing out.

Chart of SPY S&P 500 ETF with Volume, Daily Gaps and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

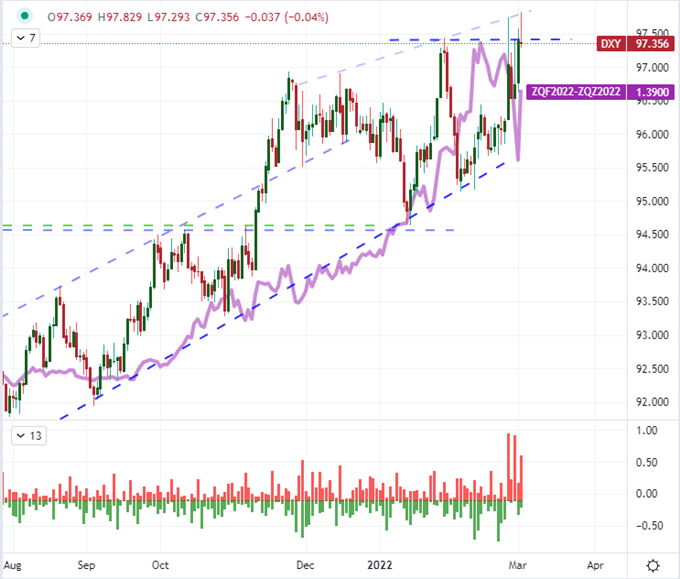

Of course, the biggest overall driver for the market this week and through the indefinite future is the situation in Ukraine. Russia has pushed its offensive on its neighbor for a 7th consecutive day. Sanctions by the US and the West also seem to be rising in tandem. The effort to ban Russian institutions to the SWIFT financial system was clarified this past session – though it the spared Sberbank, Russia’s biggest lender, which saw its UK and Germany stock values extend a full 95 percent retreat from the all-time highs late last night. Meanwhile, the UK’s NIESR has warned that the Ukraine war could cost the world economy $1 trillion and add another 3 percentage points to global inflation. That is a pressure for which the Fed and other major central banks need to respond. Fed Chair Jerome Powell was talking to Congress this past session which seemed to hold more speculative water than the ADP private payrolls surprise (+475k vs 388K expected) or the Beige Book report. Though Powell acknowledged the uncertainty factor in Ukraine moving forward, he also suggested inflation warranted a series of hikes moving forward. Notably, Fed Fund forecasts came close to discounting only 4 full rate hikes this year just yesterday, but we are once again back up to a five or six meeting run.

Chart of DXY Dollar Index Overlaid with 2022 Fed Fund Rate Forecast (Daily)

Chart Created on Tradingview Platform

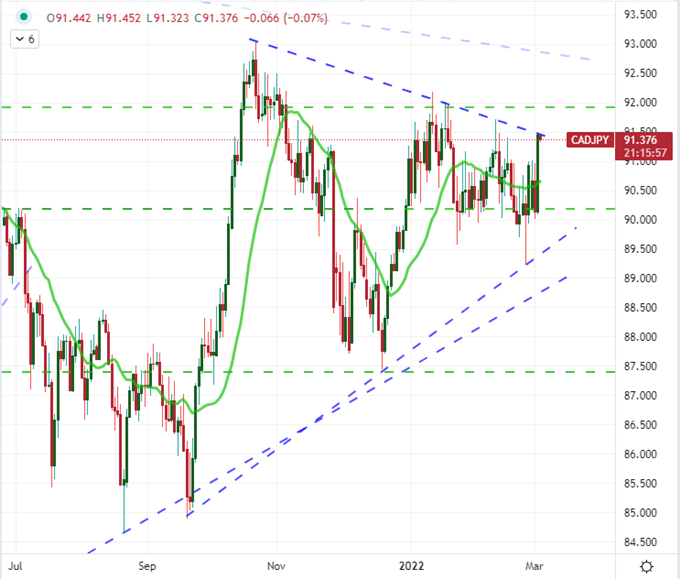

Between disparate interest rate forecasts (carry trade) and speculative roleplaying, the Dollar will be a metric to watch for broader fundamental commitments. We have Powell’s second day of testimony due later today, but I am dubious that he will blaze much of a new trail after yesterday’s remarks. Instead, my focus on the US side will shift back to the docket – though Ukraine headline density matters. On tap for Thursday, we are looking at the ISM’s service sector activity report which is a great proxy of growth in the world’s largest economy. Beyond the Thursday’s sign post, traders should be mindful that the February NFPs are on tap for Friday release. It is worth reminding here that the ADP’s payroll figure is notoriously contradictory to the official government payrolls figure. Meanwhile, the US market isn’t the only one having to deal with unquenchable inflation. The Bank of Canada (BOC) announced its first rate hike in years this past session. What is remarkable to me is that the Canadian Dollar rallied despite this outcome being fully expected. How far does this rate view go – especially with a first concern in Ukraine. CADJPY will be a good pair to watch for this debate as it has rallied into major resistance over the past months and is just as exposed to broader risk trends should forces mobilize. ?

Chart of CADJPY with 20-Day Moving Average

Chart Created on Tradingview Platform

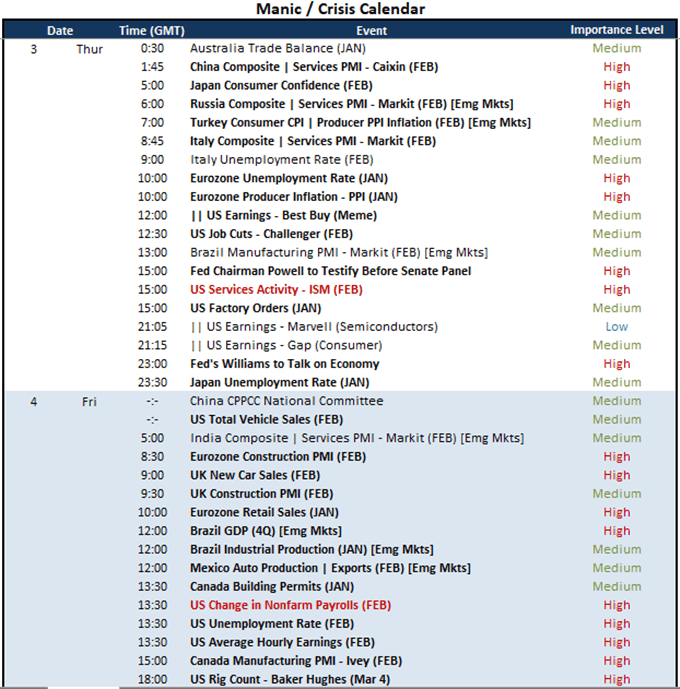

Plotting out the traditional fundamental stepping stones through the remaining 48 hours of the week, we a fairly heavy event docket ahead of us. Emerging Market PMIs are important localized growth potential. The second day of testimony and US service sector activity report will hold more profound weight over these markets. Consumer inflation and activity packs will be another cadre of updates on deck for Thursday. Looking just a little farther afield, traders watching US markets will keep in mind that Friday is NFPs day. If you are looking for eveent-driven volatility, there are few updates that compete with this singular data series.

Chart of Major Macro Economic Event Risk

Table Created by John Kicklighter