S&P 500, Best Buy, Nasdaq 100, Dollar and USDTRY Talking Points

- We are heading into the final, full-liquidity day of the week; and the S&P 500 has shown little propensity for spurring a last minute trend

- While there is a run of US event risk on tap, the Fed’s favorite inflation indicator – the PCE deflator – is Wednesday’s top event risk

- Market setups that take into consideration the liquidity dip immediately ahead are top of my mind, but outliers like the USDTRY should still be watched closely

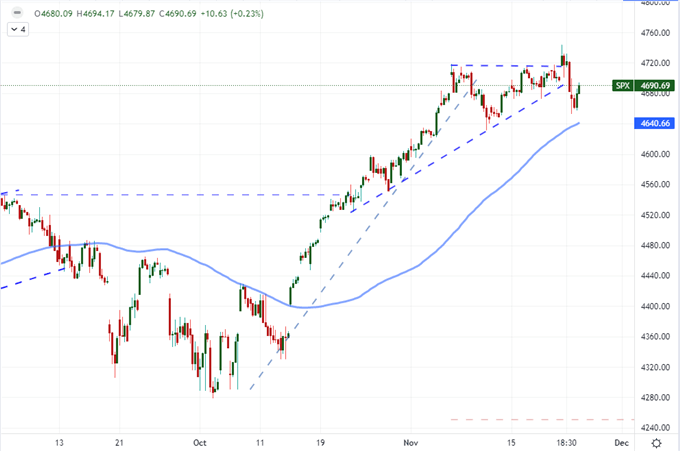

A Lot of Light But No Fire

We have seen the S&P 500 produce two significant technical breaks in opposing speculative directions in just the past 48 hours without committing to a trend in either course charting. That fits the liquidity backdrop pretty well. It is important to remember that we are heading into a well-known market drain in the form of holiday trade with Thursday’s US Thanksgiving holiday dead ahead. While not impossible, it is very difficult to develop a clear conviction when risk appetite is attempting to establish roots on a market stretched on external influence when fundamentals are under considerable duress. For pure technical traders this week has been a serious frustration. Monday’s opening bullish break collapsed by the end of the day, while the subsequent reversal through Tuesday wouldn’t be able to capitalize on clearing the floor of the pre-established rising wedge. It will be very difficult to clarify resolve before this week concludes.

| Change in | Longs | Shorts | OI |

| Daily | 1% | -1% | 0% |

| Weekly | 15% | -13% | -1% |

Chart of S&P 500 with 20-Day SMA (2-Hour)

Chart Created on Tradingview Platform

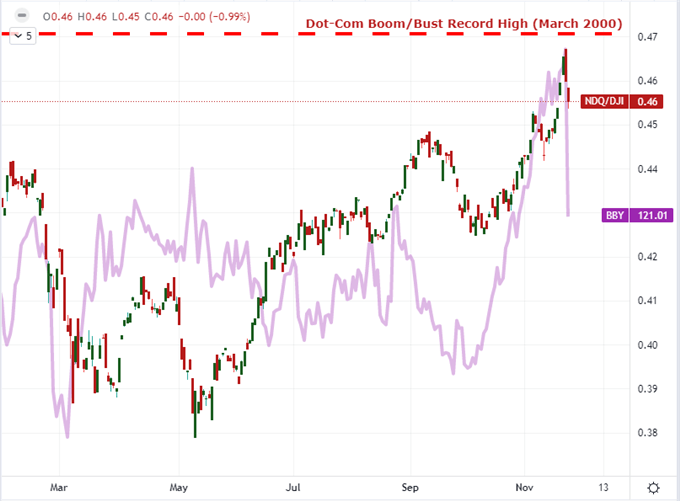

While the S&P 500 is unlikely to commit to a full fledged trend before the Thanksgiving drain and subsequent weekend, it would be foolish not to acknowledge the stretched risk position that the markets find themselves regardless of the seasonal ups and downs. When heading into a period of known quiet, there is often an effort to rein in overextended speculative positioning. The charge for momentum-fueled assets personifies those exorbitant appetites. Equities have outperformed other higher risk/return assets, while US indices have been driven to record highs relative to their international counterparts. Within the American equity market, the appeal of the tech sector has pushed the Nasdaq 100 to within easy reach of the record high of its ratio to the Dow Jones Industrial Average stretching back to the Dot-com peak back in March 2000. Yet, over these past 48-hours, we have seen the fastest retreat since May. How far will this tumble higher up the mountain stretch?

Chart of Nasdaq-to-Dow Ratio Overlaid with Best Buy (Daily)

Chart Created on Tradingview Platform

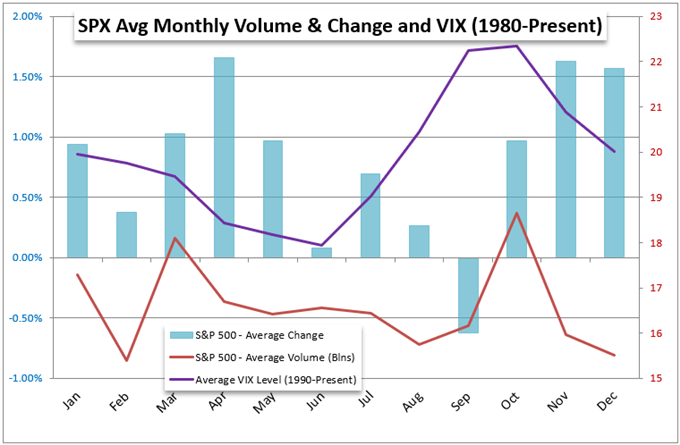

Looking ahead to the midpoint of this trading week, it is important to recognize that we are wading into a well-known liquidity drain. The Thanksgiving holiday is a US event, but it is nevertheless a big enough and consistent a gap in speculative continuity that it tends to stretch over the global financial markets. That is not to say that there weren’t certain times in history when external influences were driving market decisions such as 2011 or 2008. In generally, however, the month of November is a well established period for a drop in both volatility (via the VIX) and turnover (via S&P 500 volume).

Chart of S&P 500 Monthly Historical Performance, Volume and Volatility

Chart Created on John Kicklighter with Data from S&P

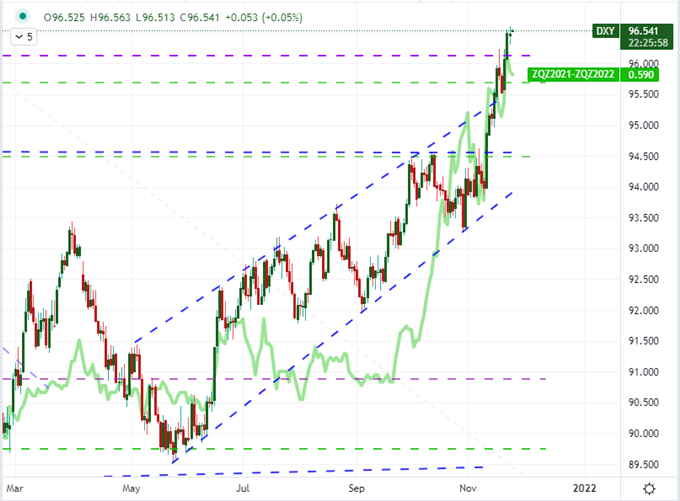

The Dollar Focuses the Fundamental Potential Through Wednesday

As we see the market’s volatility concentrate into the last practical liquidity day of the week, the Dollar looks to be the lightning rod for most of the fundamental potential. While there is plenty of event risk to digest through the upcoming session, the capacity for volatility is best served through the currency’s backdrop performance. The greenback is on pace for a fifth consecutive week’s rally to match the strongest charge since 2014 as the trade-weighted DXY Dollar Index forges fresh 16-month highs. This drive is securely founded on the basis of hawkish interest rate expectations for the Fed – and an effective market conversion to action. Fully pricing in two standard rate hikes (25bp) for the US central bank in the coming year seems to be a far more productive market mover than the RBNZ’s actual two rate hikes this year …

Chart of DXY Dollar Index Overlaid with Implied Rate Forecast for 2022 from Fed Fund Futures (Daily)

Chart Created on Tradingview Platform

Top event risk on the docket through these final 72 hours is the concentration of US event risk on Wednesday alone. There are two themes to focus on in the economic run: growth and monetary policy projection. Following the November PMIs this past session (which the US and other developed economies bested expectations on), there is a run of data that will reflect on US health through durable goods, trade balance, consumer spending and new home sales (all for October). As comprehensive as that look may be, I consider the PCE deflator to have far greater potential all on its own. This is the Fed’s preferred interest rate reading and we are now seeing a heavy pricing for a rate hike by June in futures – well ahead of the central bank’s own allowance in its previous forward guidance. There is discord that the market needs settled. That said, I think there is greater short-term market potential via the Dollar should the inflation reading offer significant relief to cut down the recent rally.

Calendar of Major Macro Event Risk Friday and Early Next Week

Calendar Created by John Kicklighter

Don’t Forget About the Outliers

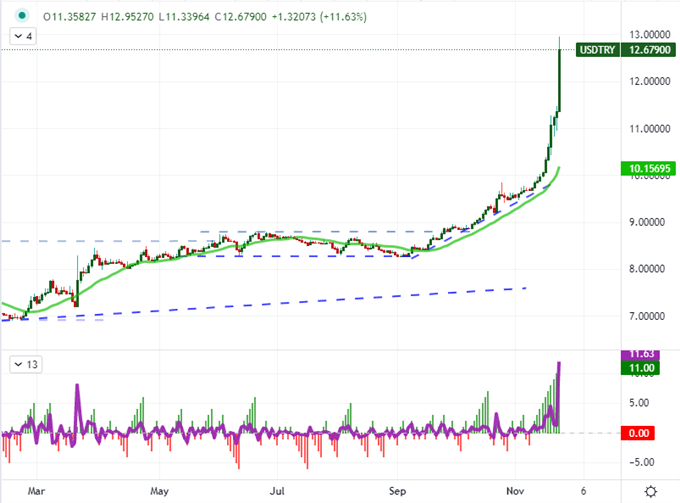

While my attention will always come back to general risk trends and the Dollar as a pilot to developed world monetary policy influence, I will never allow the potential there to distract me from the productivity of active outliers. The crypto market is one such segment of the market that is interesting given its concentration among speculative players and its unique condition of trading through holidays and weekends. Yet, as volatile as this market may be, it has fallen behind of the activity readings for the emerging FX market. The Turkish Lira’s plunge this past week is an obvious highlight. This past session alone, USDTRY surged another 12 percent making for an 11th straight day’s climb to record highs. We are navigating into a possible currency crisis scenario. While not as dramatic, I would be remiss not to mention the impressive continuation from the likes of USDMXN and USDRUB. USDCNH seems to be of no interest at all given its steadfastness, but that is a manufactured quiet that will eventually end.

Chart of USDTRY with 20-Day Moving Average, 1-Day Rate of Change and Consecutive Candles (Daily)

Chart Created by John Kicklighter with Data from IHS Markit

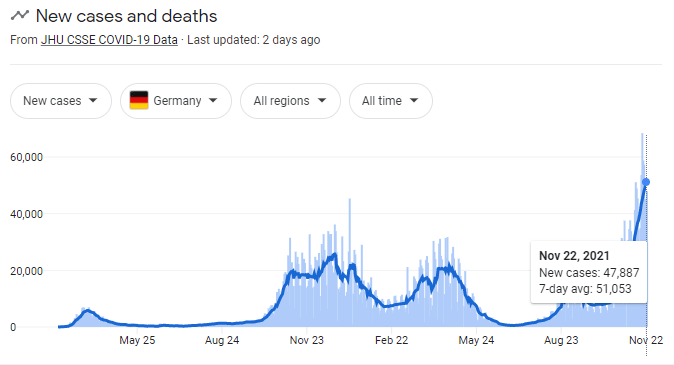

China’s financial struggles are a matter that I will never let idle in the back of my mind. The country has yet to resolve its Evergrande and broader housing development market issues, and it is trying to level out bad loans while proving to the world that defaults can occur without pulling down the system. This is an opportunity to pass on losses to investors without causing all-out economic and social fallout. Then there is the heavily covered charge in covid cases. While a worldwide problem for countries like the US and UK, the most acute pressure is registered in Europe. Austria has shut down while riots have broken out in the Netherlands. Yet, a more systemic tipping point would be if Germany decided it necessary to shutter the economies for a number of weeks during the holiday period.

Chart of New Covid Cases in Germany (Daily)

Chart from Google.com with Data from an Aggregate of Sources