S&P 500, Earnings, EURUSD and USDCADTalking Points

- Risk trends more than recovered from the Monday plunge this past week with record highs for the S&P 500, Dow and Nasdaq 100 in an otherwise quiet trading period

- Ahead, the docket is overrun in high-level event risk with themes covering US earnings, US and European official GDP readings and a FOMC rate decision among other listings

- Anticipation may prove the greater influence than actual market response, but the EURUSD’s extreme congestion and S&P 500/Dow record high are due some resolution/motivation

Risk Trends are Coasting Higher for Certain Market Markets Into the New Week

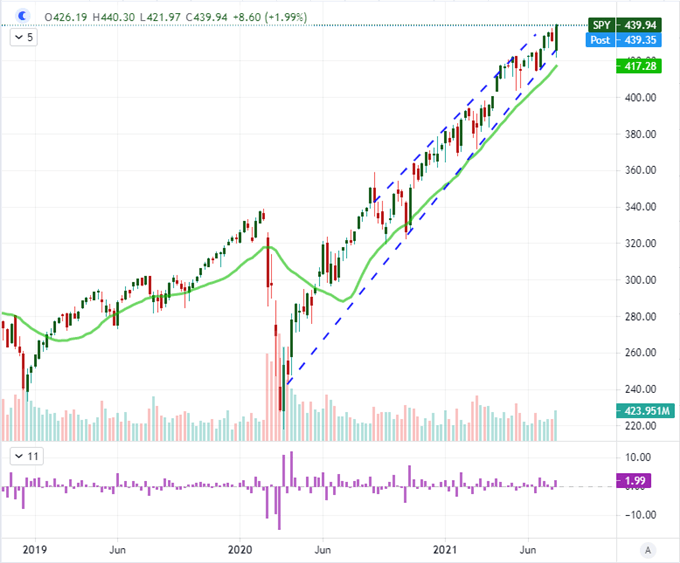

We are smack in the middle of the summer doldrums, but the market’s complacent bid will certainly be put to the test over the coming week with an extraordinarily dense run of event risk on tap. While there are themes without a scheduled release that can stir fear in the financial system – like the rise in Delta variant Covid cases – observant market participants have enough to worry about through the economic docket. Ultimately, it seems clear that risk appetite is reaching well beyond the common course of fundamental backing. The record highs from the S&P 500, Nasdaq 100 and Dow this past week were not inspired by anything in particular; but that is has been the score for these markets. A persistent charge in yield or growth forecasts is not necessary to carry the complacent bid of an investor reassured by years of moral hazard. As we pass through a period known for its low liquidity and turnover – and resultant speculative bid – the burden is on risk trends to break the complacent bid that has nudged the market relentlessly higher these past months.

Chart of the SPY S&P 500 ETF with 20-Week Moving Avgs, Volume and Weekly Change (Weekly)

Chart Created on Tradingview Platform

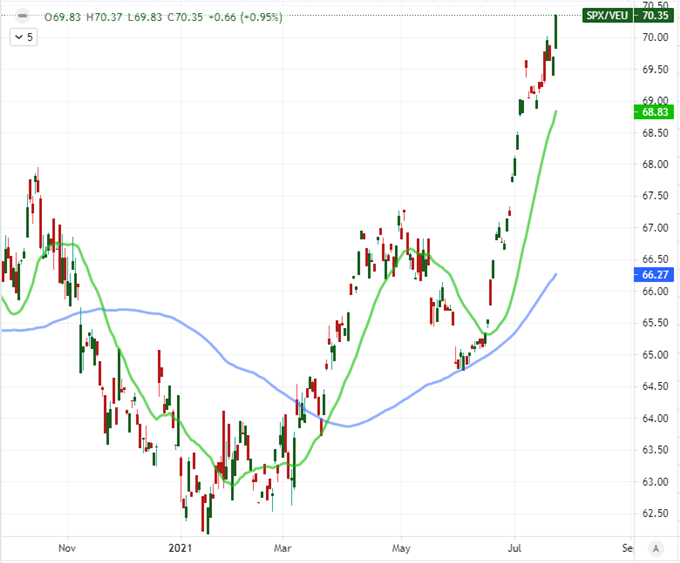

In segmenting risk appetite trends, there seems are particular appetite for the US assets. Below is the S&P 500 relative to the ‘rest of world’ equity ETF (VEU). The ratio has exploded to a record high through the close of the week. What about the US fundamental backdrop was so inspiring to project such speculative favor? I would not say that this is legitimately a fundamental charge but rather the preference for speculative momentum already established. The record highs from the S&P 500 itself draws contrast to the hesitation from the German DAX, UK FTSE 100 and Japanese Nikkei 225. These are principal measures of risk appetite in their own right and region, but the progress simply does not match the inspiration of their US counterparts. Hesitation is truly the more rational perspective given the economic and financial balance at present, but the ‘buy the dip’ mentality can be difficult to throw off without a more systemic threat.

Chart of the Ratio of S&P 500 to VEU ‘Rest of World’ Equity ETF (Daily)

Chart Created on Tradingview Platform

Heavy Event Risk and Systemic Themes: The Difference Between Volatility and Trends Ahead

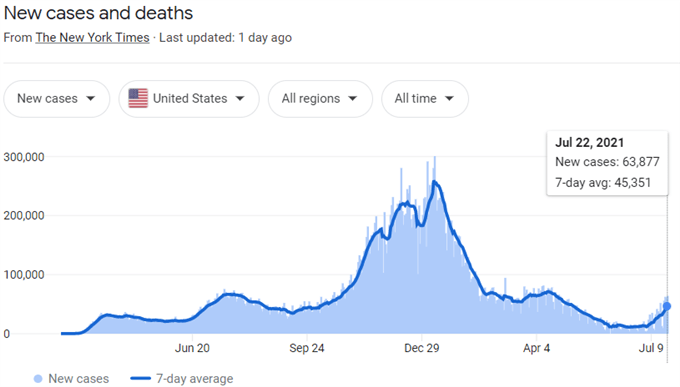

Gauging the potential for volatility ahead, I’m certainly monitoring general market conditions and tracking overt technical patterns; but the economic docket has overt milestones that will stand as benchmarks for which traders can move between. Before referencing the economic docket for its highest-level items, there is the general risks associated to the revival in coronavirus cases worldwide. The delta variant of the virus is proving troublingly virulent and cases are rising in many of the world’s largest economies that are attempting to slowly reopen to support their respective economies. This is a matter that does not have the capacity to be a favorable driver. The best bulls can hope for is a slow leveling out of cases which does little to charge optimism. That said, the faster the case count rises for countries like the US – much less the globe – the more attention it will draw from the latent bears.

Coronavirus Cases Worldwide

Chart from Google.com with Data from Wikipedia

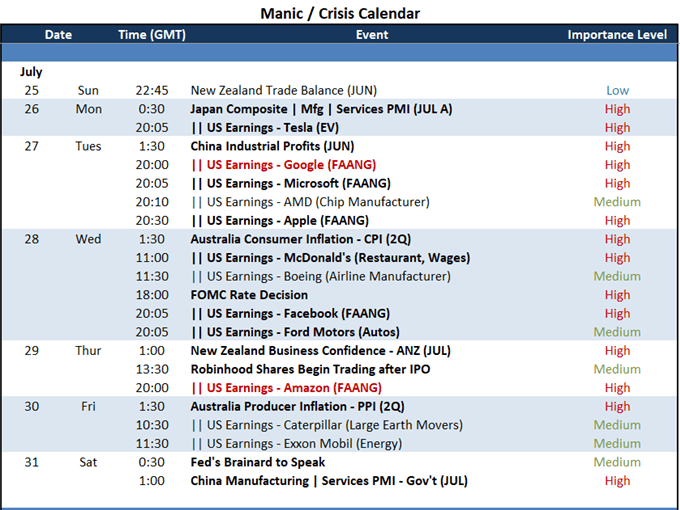

From a scheduled event risk perspective, there is a lot of data on tap and a number of themes that will provide a fundamental charge. Monetary policy and growth set aside for a moment, earnings represents a critical US theme this week. Overall, nearly 40 percent of the S&P 500’s members are due to report their performance from the past quarter this week and amid this list are a host of macro-important companies and bulk of the FAANG members. Among those tickers that I’ll be watching from a macro perspective, Monday offers of Tesla: a company that connects consumer spending trends to climate change to cryptocurrency. More overt will be the vaunted tech leaders due to report through the week: Google, Apple and Microsoft on Monday; Facebook on Tuesday; and Amazon on Thursday. I give the greatest deference to AMZN as it represents pandemic shift towards online spending habits while still monitoring the US consumer’s appetites as a critical global growth driver.

Top Earnings Releases in the Week Ahead

Calendar Created by John Kicklighter

Where the Volatility is Most Productive

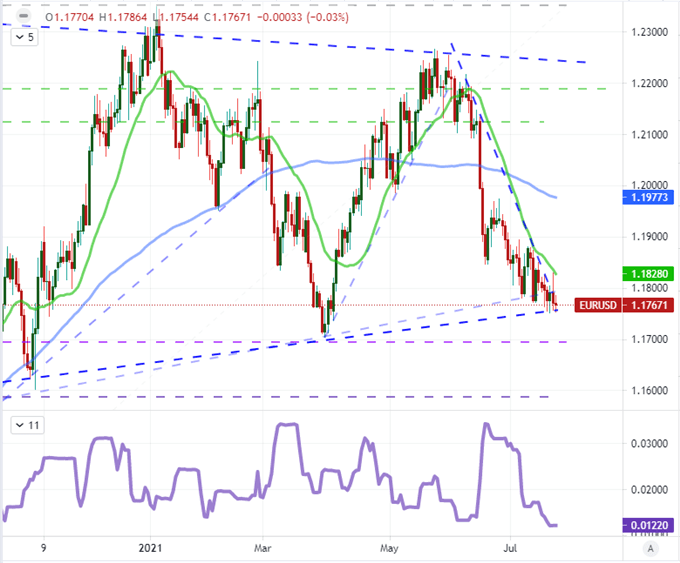

For sheer market movement, the Dollar seems to be one of the most put-upon benchmarks moving forward. The currency’s standings for most major crosses presents a technical and fundamental combo that is at the very least provocative, but it is important to always consider the market conditions. Liquidity creates a backdrop whereby trend development is exceptionally difficult to inspire – though not impossible. While it would certainly be appealing to see a transition from congestion to productive trend, I am not operating under the assumption that such an evolution is at hand. Therefore, my approach to the week ahead will be spotting assets that look primed for short-term resolution but also carry the potential for something more should it arise. EURUSD is a great example of this hybrid picture. The benchmark currency pair is carving out an extraordinarily restrictive 17-day trading range – comparable only to five other periods in the history of the Euro – and a breakout seems highly likely. That said, a trend likely depends on event risk like the FOMC decision or US / Eurozone 2Q GDP releases. This is absolutely a pair to monitor.

Chart of the EURUSD with 20 and 100-Day Moving Average and 17-Day Historical Range (Daily)

Chart Created on Tradingview Platform

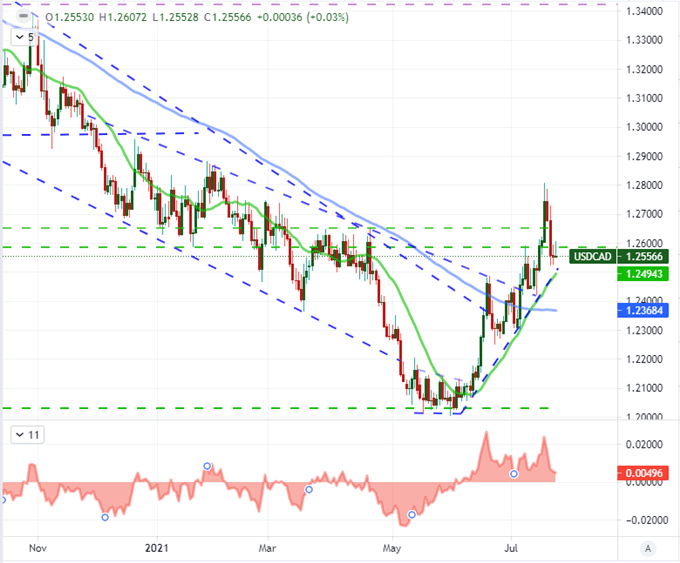

With a more distinct skew in potential for differing market outcomes, USDCAD doesn’t necessarily scream breakout risk’ but it has technical context that seems to support the progression of an unfolding reversal. That may seem a more stable chart pattern, but follow through is not an easy perspective to foster given the broader conditions we have been dealt. This past week’s pullback has pulled us back to the backbone of a reversal effort highlighted by a 20-day moving average and trendline support around 1.2500. While there is a little Canadian event risk on tap, the Dollar is more likely to be the principal driver here – making for a more uniform speculative influence.

Chart of USDCAD with 20 and 100-Day Moving Averages with 20-Day Disparity Index (Daily)

Chart Created on Tradingview Platform