S&P 500, Dollar, EURUSD, USDCAD and AUDNZD Talking Points:

- Chinese GDP and other growth-oriented data points this past session did little to charge the financial system as risk assets generally slipped

- Monetary policy remains the most tapped-in fundamental theme, but the scheduled event risk that could override complacency is noticeably thinning

- Top scheduled event risk for Friday is the US retail sales and consumer confidence report from the UofM as consumption and inflation expectations

Monetary Policy Remains the Most Prolific Fundamental Influence but Winds are Dying Down

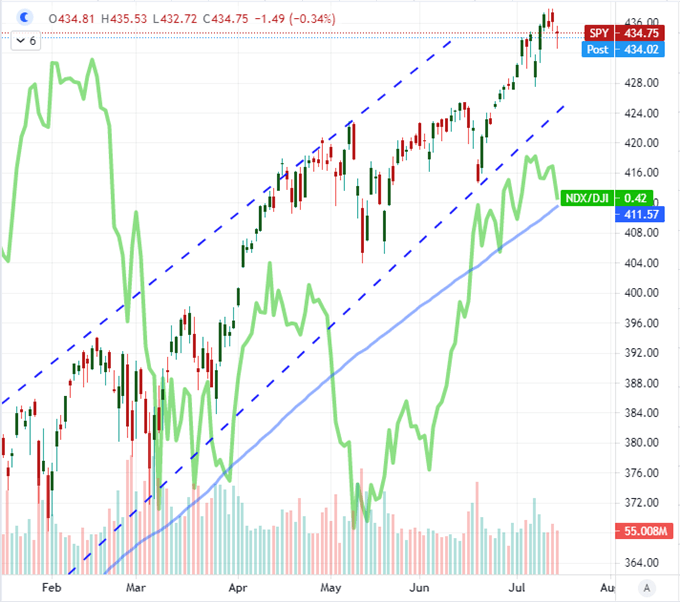

Global equities and other risk-sensitive assets are heading into Friday with a broad pullback clouding the outlook. Yet, as wide as the ‘risk off’ influence may be, it remains a relatively reserved move. Thus far this week, I’ve noted the unmistakable ‘hawkish’ shift in monetary policy which poses an existential threat to speculative assets that have used the assumption of easy capital and exceptionally supportive cabal of central banks to build up enormous exposure to compensate for the lack of yield to be made. Benchmarks like the S&P 500 and Dow managed to ride out the fear when it peaked Tuesday and Wednesday, but the ebb of the fundamental tide hasn’t in turn unleashed the bulls. Complacency cuts both ways. Notably from risk trends this past session to carry forward to Friday analysis, volume (from the SPY ETF) and volatility (VIX) were under strict control this past session. Further, it is worth noting that there was a distinct contrast between the ‘growth’ Nasdaq 100 and ‘value’ Dow with the ratio taking a notable retreat on the -0.7 percent NDX drop. Where should we look for the next charge in risk? I will be marking US retail sales and consumer confidence as the next volatility threat.

Chart of the S&P 500 with 20 and 100-Day Moving Avgs and 3-Day Range (Daily)

Chart Created on Tradingview Platform

Monetary Policy Traction Requires Regular Reinforcement

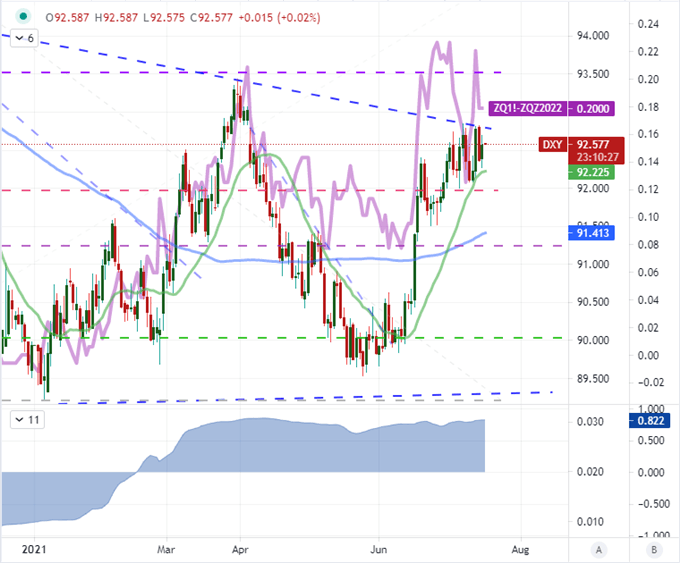

While my focus for these final 24 hours of trading this week is shifting back to localized economic-focused data, I believe monetary policy remains the most capable theme for driving the market on a full-scale trend. However, we are at the very beginning of a normalization shift in which the standard rhetoric from central bankers the world over that ‘interest rates will remain exceptionally low for an extended period’. Technically, that would be true even if we had seen benchmarks rates increase 100 basis points considering yields are currently at ground level. Market participants nevertheless are glad to accept the assurances. This past session, Fed Chairman Jerome Powell gave his second day of testimony before Congress (the Senate); but despite the different faces and questions, the content of his remarks didn’t change materially. He maintained the ‘transitory’ inflation view and that interest rates are a ways off, but he did suggest the Fed would be talking taper timeline at the next meeting (July 27-28) and that there was evidence of “froth” in the markets. The Dollar checked higher before seriously testing the 20-day moving average, but implied Fed Funds rates held at 20 basis points of hikes through 2022.

Chart of DXY Dollar with 20, 100-DMAs, Implied Fed Hikes Through 2022, 20-Day Correl (Daily)

Chart Created on Tradingview Platform

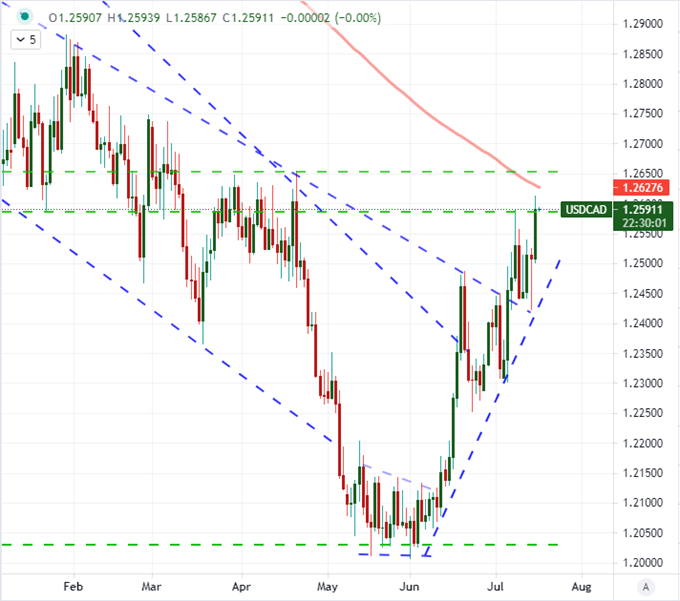

While the market chewed on the familiar dovish views of the Fed Chairman, there was the contrast of recent tangible hawkish moves from some of the US bank’s comm bloc counterparts. The Bank of Canada (BOC) tapered the second time this year on Wednesday, so it would seem to technically have a strong lever against the Greenback. Instead, the Canadian Dollar slid against most of its counterparts this past session to generate a few notable bearish breaks for the currency. USDCAD was the most prominent given the fundamental split as it advanced above the midpoint of the 2002-2008 historical range at 1.2585. The next critical milestone is the 200-day moving average at 1.2625.

Chart of the USDCAD with 200-Day Moving Average (Daily)

Chart Created on Tradingview Platform

For sheer, immediate impact, the New Zealand central bank’s (RBNZ) announcement that it was ending its stimulus program leveraged the biggest overall move from a monetary policy perspective this week. The Kiwi Dollar soared the day of the shift but stalled out immediately afterwards. Even excluding the check from the US counterpart on NZDUSD, there was a disappointing reversal across the board. Even NZDJPY would see a drop despite the otherwise mild backdrop for risk trends. Perhaps the most neutral of the Kiwi crosses for reference was AUDNZD. This pair tends to balance out risk implications and has close economic ties. It is therefore much more consistent a relative monetary policy gauge for either. The hold on a broader range speaks volumes on the market’s condition at present.

Chart of the AUDNZD with 100-Day Moving Average (Daily)

Chart Created on Tradingview Platform

The Effective Motivations on Monetary Policy and Friday’s Top Event Risk

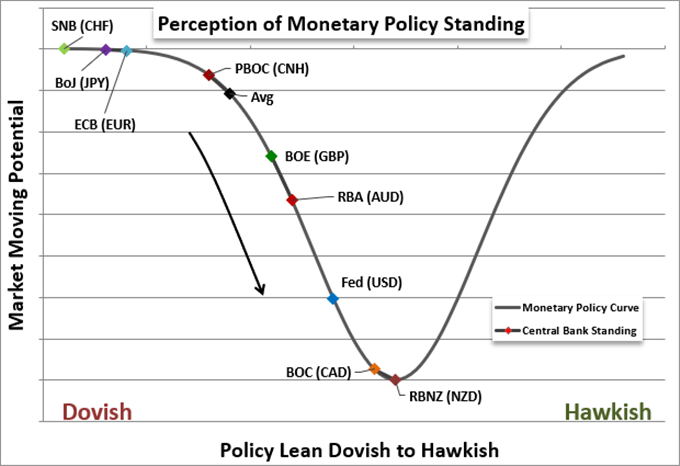

It is tempting to look at the Dollar, Loonie and Kiwi’s price action these past few days and conclude that monetary policy simply doesn’t matter to the markets. I would not go that far. The relative aspects of monetary are a powerful market mover in the FX market in particular given the projection of relative returns it represents between two different countries. That said, what does the contrast look like when the collective seems to be slowly tightening the reigns in tandem? While it was an official taper for the BOC and RBNZ, the rate outlook for the Fed is its own hawkish influence. Relative appeal may be suppressed medium-term, but consider the implications of monetary policy in the developed world shifting in favor of the hawks. There is enormous dependency on the generosity of deep-pocketed central banks. If and when markets start to rest their attention on the course of external support, the pain could be disproportionate.

Chart of Relative Monetary Policy Standing of Major Central Banks

Chart Created by John Kicklighter

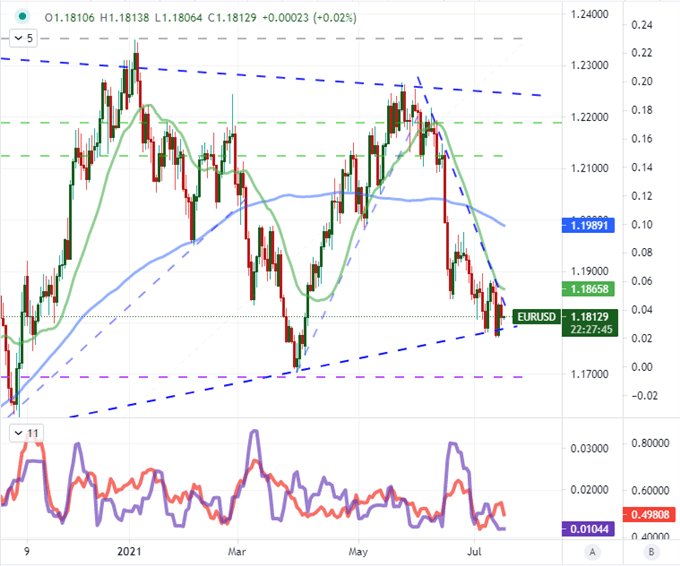

Themes may carry a lot of potency when activated, but constrained liquidity means the energy remains largely potential. For more tangible impact, I will be watching the economic docket Friday for catalysts. There is heavy mix in the Asian session between the New Zealand 2Q CPI, Australia consumer inflation expectations and Bank of Japan rate decision (BOJ); but despite the attention paid to monetary policy, these are likely to struggle to spark imagination where tapers and US inflation could not. I will pay closer attention to the US retail sales and University of Michigan consumer confidence survey. These could certainly be interpreted as central bank fodder, but I believe the direct view in the US consumer’s consumption habits is more palpable in economic terms. A sufficient surprise could earn a technical break that sets up a bigger commitment next week. For guidelines, I am watching EURUSD closely as the pair has carved out its smallest 10-day (2 week) trading range since January 2020 while its 10-day ATR reflect comparative volatility. An active market with vary narrow boundaries is a reasonable mix for breakout potential.

| Change in | Longs | Shorts | OI |

| Daily | -1% | -4% | -3% |

| Weekly | 4% | -10% | -5% |

Chart of the EURUSD with 20 and 100-Day Moving Averages (Daily)

Chart Created on Tradingview Platform

.