To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Talking Points:

- Next week brings another FOMC meeting and with USD breaking out to fresh near-term highs, traders are likely pricing-in the prospect of a hawkish (talking up higher rates) stance from the Federal Reserve.

- As U.S. stock prices have surged to fresh all-time highs, with a 9% gain over the past three weeks and a 20% gain in the past five months (in the S&P 500), this may be an opportune time for the bank to transmit the potential for rate hikes in the second half of the year.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

The Fed meets next week and in yesterday’s article, we looked at the prospect of USD strength on the back of a potentially-hawkish or tone from the world’s largest national Central Bank. Given that U.S. stock prices have surged to all-time highs, with American equities now nearing levels as expensive as the world’s ever seen when compared to international stocks, it would make sense for the Fed to, at the very least, tap on the brakes a bit to let markets know that rate hikes may be coming down the road should ‘strength’ persist.

What we’re speaking of here is what’s become known as the ‘Fed Feedback Loop,’ in which the bank is apparently shifting monetary policy stance in response to stock prices. As stocks continued to cling to all-time-highs (at the time) throughout last summer, the Fed continued to talk up a hike in September. But when the Chinese meltdown permeated through the rest of the world in August, pulling American equities lower along with it, the Fed kicked that September hike back. Markets regained momentum and re-surged towards prior highs until, eventually, stock prices were strong enough for the Fed to hike in December along with a warning that a full four rate hikes might be coming in 2016. Within a couple of weeks of that rate hike and the risk aversion and pain was back in global markets with the turn of the New Year; just six weeks later we saw the Fed capitulate on the whole four rate hike idea, and stock prices began to move up, again. In March, they reduced the expectation for rate hikes down to two from the previous four, and this just gave even more momentum to equity prices. Then Brexit happened. The apparent takeaway from Brexit is that the world would likely see more Central Bank support should the need arise, and after last week’s Japanese elections, this idea of ‘more stimulus’ gained additional traction, sending the S&P 500 to even-higher all-time highs.

At this point, the S&P 500 has gained 9% since the post-Brexit lows, and a whopping 20% since the lows in February. And again, this is really just on the back of the anticipation of even more stimulus and the fact that the Fed will likely get more dovish if global risks begin to flare. And given the strength of last month’s jobs report, with employment being a ‘sore spot’ at the previous Fed meeting after the abysmal report of two months ago –we may have the ideal environment for the Fed to talk up rate hikes in the second half of the year.

The meetings in September and December appear to be the most likely targets from here, although the odds of actually getting a rate hike at either meeting, despite what the Fed says next week, are probably pretty slim. More likely we’d see one or more of the litany of global risks flare-up until, eventually, we see the Fed go dovish again; as we’ve now seen multiple times over the past ten months.

But as we approach the July Federal Reserve meeting taking place next week, the bank has an opportune environment to begin talking-up higher rates, similar to what we saw in the month of May just ahead of that abysmal NFP report that seemingly eliminated the prospect of a June hike.

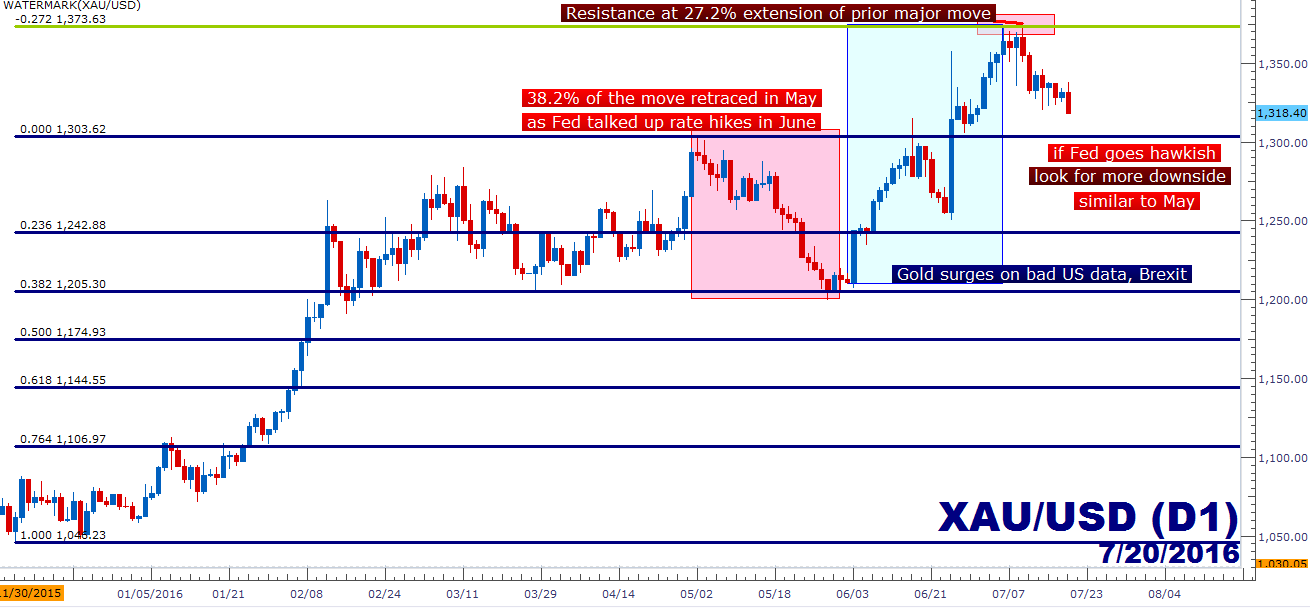

One market that will likely see significant movement in the event of a hawkish Federal Reserve would be Gold. Gold prices took a fairly serious punch throughout May as the Fed was talking up the prospect of a June hike, and should the Fed make a similar such move, we’d likely see a recurring-type of theme in Gold prices. In the month of May Gold prices moved from above $1,300 to below $1,200; and this was after a 4.5 month movement-higher of over $250. But as negative U.S. data began to show and then as Brexit actually happened, Gold prices caught major bid and ran-up to fresh highs. The high happened to come-in right around the 27.2% Fibonacci extension of the prior major move, giving rise to the theory that, long-term, the bullish move isn’t done. But for now, we may see a continued retracement of the up-trend should the Fed take a hawkish stance.

Created with Marketscope/Trading Station II; prepared by James Stanley

The Cable (GBP/USD)

Pound-Dollar is another market that will likely see brisk movements should the Fed take a hawkish stance next week, and the likely catalyst would be further divergence in interest rate expectations between the two economies. The Bank of England did not cut rates last week as many were expecting. As we said, given that next month brings the BOE’s inflation forecasts and economic projections (aka, Super Thursday), it might make more sense for the bank to wait to kick rates lower, as traditionally moves in rates from the BOE have been coupled with Inflation projections; or somewhat of a thesis explaining the context of the move. So we probably haven’t heard any element of finality on U.K. rate cuts from the Bank of England, and should the Fed talk up the prospect of higher rates in the U.S., this only exacerbates the divergence in rate trajectory between the U.S. and the U.K.

Getting short here can be a challenge, as bounces have been vigorously sold in the post-Brexit environment. It’s as if the market knows that something is coming and can’t wait for resistance to come-in before selling more. On the chart below, we take a look at the shorter-term variety in GBP/USD to look at potential jump-off levels for short positions:

Created with Marketscope/Trading Station II; prepared by James Stanley

Swissy

For those looking to make top-side plays in the US Dollar, the pair that we’ve been discussing for that theme of recent has been USD/CHF. On the morning after Brexit, the Swiss National Bank intervened in the spot market to quell a strong Franc. And while this doesn’t necessarily have carry-over tonality, meaning that we don’t know that the SNB will do it again, it does expose the fact that the bank is on-guard for rampant Franc strength. This perceived sense of weakness could be enough, when married up with a strong US Dollar, to allow for a relatively clean trend-side move. At the very least, if looking to push short-USD themes, traders would probably want to look elsewhere. And if we do get a strong USD on the back of a hawkish Fed, this disparity could allow for continued top-side movement.

On the chart below we look at the near-term technical setup in the Swissy with potential support levels to plot re-entry.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX