Will the Dollar recover some of its steep declines this past year in 2018? Will risk appetite cool following years of liquidity drain? Read more in our first quarter 2018 forecasts.

Watch for the 2018 Technical Forecast for the US Dollar on the Trading Guides page to be released soon.

US Dollar Q1 Forecast: Dollar’s Options for Recovery Fade Into 2018 Open

John Kicklighter, Chief Strategist and James Stanley, Strategist for DailyFX.com

As Its Yield Appeal Fades and Political Risks Rise, Dollar’s Path Looks Difficult

All told, 2017 was a terrible year for the US Dollar. In percentage terms, the ICE Dollar Index (DXY) suffered its largest decline since 2003. However, there was a silver lining to be found in the closing quarter of the period. In the fourth quarter specifically, the currency managed to level out – notably at significant support. There is so much potential in a consolidation phases. They can represent the foundation for a recovery or merely signify a pause while speculative interests work up the nerve to forge the next move.

Typically, technical progress measured against the fundamental backdrop leaves us with a sense of speculative reach or over-reach that sets the stage for the next phase. There is little to suggest that the Dollar is chomping at the bit for a recovery through the opening quarter of 2018. On the technical side, indecision colored the previous three-month stretch with the smallest range since 2Q 2014. Fundamentally, the currency had every reason to advance on the basis of its monetary policy advantage but that ‘value’ seemed to be deprecated by speculators. Regardless, it took on the garb of a carry currency that wouldn’t offer material return, but would nevertheless expose it to the elements should risk aversion sweep in.

There are certainly means for the Dollar to mount a meaningful recovery moving forward. However, those scenarios are increasingly improbable or so convoluted to be poor foundation for bulls to draw confidence. Moving forward, we must still pay close attention to relative monetary policy and the discussion surrounding the Greenback’s safe haven role. Yet, novelty may translate into greater emphasis on a troubling shift in political stability or the performance of the USD’s largest counterparts.

Political Risk and Global Withdrawal

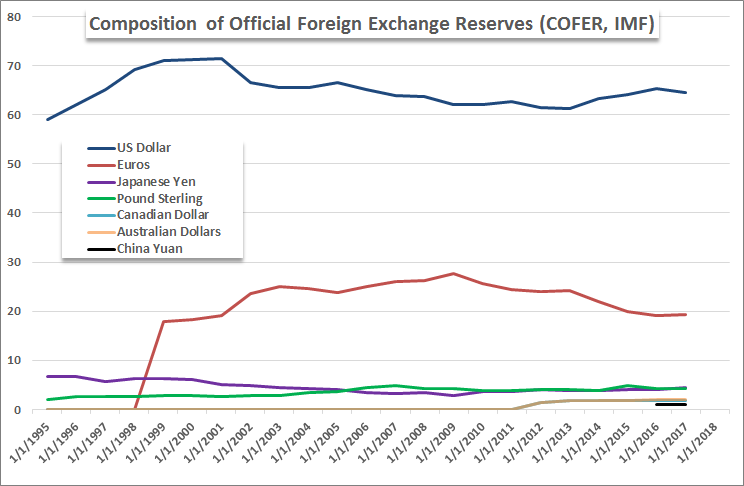

Immediately following the 2016 US Presidential election, the Dollar and US capital markets climbed sharply. Equities continued to advance through the preceding year, but the currency quickly lost its lift and soon plunged into the bear trend with which we are now so acquainted. Donald Trump was seen as the candidate of dramatic change, and he has so far delivered on that characterization. In change, there is uncertainty; and investors are not particularly fond of an outlook for which they cannot comfortably project. While the promises of a reduced deficit, roll back of regulation, tax break and infrastructure program still hang in the air; what has actually made its way through the legislative process looks very different. A particular concern that is also troubling underappreciated is the risk that the proposed tax plan could sharply inflate the United States deficit over 10 years which in turn would likely lead to downgrades from the major ratings agencies. Losing AAA status from Moody’s and Fitch – while likely receiving another cut by Standard & Poor’s – would render a permanent loss of altitude from the Dollar and upgrade in volatility as reserve capital is diversified.

Chart prepared by John Kicklighter, Chief Strategist for DailyFX.com. Data from Bloomberg Terminal

A further concern in the political vein is the isolationism that follows political instability that seems both manufactured and coincidental. The investigation into foreign meddling in US elections has already roped a few people in the President’s circles, and there is substantial risk that additional critical players in the administration may eventually be indicted. If this runs too deep, it could push global investors away from the US – moreso than the government’s purposeful trade crackdowns which have led to modest shifts to isolationism that naturally reduce the use of the Dollar in global transactions. Further, if there is an outright military engagement – such as with North Korea – the global upheaval could truly unmoor the Dollar’s haven standing.

Interest Rate Advantage Turning Into a Weight Around the Dollar’s Neck

Over the past few years, the Federal Reserve has conducted a remarkably hawkish monetary policy campaign. It isn’t that the central bank has lifted rates back to attractive levels of yield in a short time, but rather that the Dollar and US rates have been the ‘only game in town’. Aside from a one-off hike from the Bank of England and 50 basis points of tightening by the Bank of Canada, the major policy authorities have all maintained their extremely accommodative stance. And yet, what has this contrast rendered the Dollar through 2017 when the Fed hiked on three separate occasions? Significant losses. Market participants are not seeking out income in the form of carry, dividend or yield. Even with hikes from the US central bank, rates of return remain extremely low. Speculative appetite is seeking out capital gains – in other words, a ‘buy low, sell high’ mentality. Clearly the Dollar is not providing on that front.

The Fed projected three further rate hikes through 2018 in its December meeting Summary of Economic Projections (SEP), but the expectation of further tightening is heavily priced in. There is little novelty or discount in this policy intention, so there is little in the way of capital gains to be reaped. And, while the risk connection has waned somewhat with time, the Dollar is still the ambiguous carry currency. That could have the unusual side effect of driving the most renowned safe haven lower in the event of broad risk aversion. That said, if a deleveraging wind sweeps over the market, it is likely to turn somewhat disorderly. The depths of complacency are registered in the long stretch of time between even modest (1 percent) S&P 500 declines and persistence of the VIX below 10 are troubling reminders of how much there is to lose. When liquidity and safety of capital is the top concern, there is no stopping to debate the sanctity of US Treasuries and money markets. We should not hope for disaster for favorable opportunities, but that is the state in which the Dollar finds itself.

It’s Still a Relative Market

Aside from a catastrophe in the global financial system, another more practical boon may exist for the Dollar. Exchange rates are a relative market. Value is established in the weakness or strength of the counterparts used to price a single currency. It may seem counterintuitive, that other currencies carry greater influence over the Greenback than the Greenback has over its peers. Yet, that certainly does happen and is very likely to occur should the Dollar otherwise drift. We have witnessed considerable strength from major Dollar counterparts like the Euro and Pound this past year. The former was lifted by anticipation that a monetary policy shift is in the not-so-distant future and thereby the Euro was trading at a serious discount to its future value. For the Sterling, the progress through Brexit is alleviating some of the serious pain inflicted in the hours, days and weeks following the June 2016 Brexit vote.

In the Euro’s lift, the hope for near-term rate hikes has consistently been squashed but the currency has managed to cling to its gains. If political stability in Germany remains an unresolved issue or the exit of an EU member (the UK) inspires others to follow in their wake, it could render massive benefit to the Dollar as the only viable, liquid counterpart that can absorb the exodus. Brexit is a more direct matter for the Pound, and the growing threat to the UK government’s stability can send traders seeking stability elsewhere. It is possible that we even see global speculative unwind whereby a range of currencies receive a quick and cruel discount for their dubious efforts to overtake the Dollar in the pursuit of historically inadequate rates of return.

Watch for the 2018 Technical Forecast for crude oil on the Trading Guides page to be released soon.

Oil Q1 Forecast: Oil Fundamentals Turning Positive

By Tyler Yell, CMT, Analyst and Trading Instructor, and Nick Cawley, Fundamental Analyst for DailyFX.com

The outlook for global oil markets in 2018 is starting to turn positive as the Organization of Petroleum Exporting Countries’ (OPEC) goal of rebalancing supply and demand begins to take shape. OPEC, and other non-OPEC countries, recently agreed to extend their production cuts until the end of 2018, in an effort to clear the global oil glut. OPEC secretary general Mohammad Barkindo recently said that output curbs have cut this oil stockpile to around 130 million barrels over the five-year average - OPEC’s goal is to reduce the oil stockpile back to the five-year average. According to Barkindo, the oil markets are now starting to stabilize, something that has eluded the sector for several years.

The price of oil fell by 80% between mid-2014 and January-2016 due to over-supply from North America, threatening global growth and distorting expansionary prospects. The threat of excessive crude production by US shale oil companies remains however according to the International Energy Agency (IEA) who said that well completion rates have picked up in line with rising oil prices. According to the IEA, 2018 may not be “quite so happy for OPEC producers” and further that oil stockpile may not shrink in line with OPEC’s hopes and forecasts.

Oil markets will be helped in 2018 if the global economy grows as expected with an upswing likely to be seen across the Europe, Japan, the US and emerging markets. Global growth is expected to rise to 3.6% in 2017 and to 3.7% in 2018, according to the International Monetary Fund (IMF), an upgrade of 0.1% from their last report in April. Further, China is expected to overtake the United States as the largest importer of crude oil in 2018 with demand forecast to grow by an additional 300,000 barrels a day in 2018.

Watch for the 2018 Fundamental and Technical Forecasts for the major global equity indices on the Trading Guides page to be released soon.

Equities Q1 Forecast: Stocks May Be More Vulnerable Than They Appear

By Ilya Spivak, Senior Strategist, and Paul Robinson, Market Analyst

At first glance, the global equities landscape looks rather rosy as the calendar turns to 2018. Global economic performance looks robust, with PMI data from JPMorgan putting the pace of manufacturing- and service-sector growth at the highest in almost three years. Meanwhile, numbers from Citigroup show global economic data flow still trends to outperform economists’ forecasts, suggesting markets may still be underpriced relative to realized growth dynamics.

The political landscape is also encouraging. The UK Autumn Budget made fiscal policy more accommodative and Brexit negotiators seem to have a deal on divorce terms, opening the door to talks about a post-split trade deal. A round of worrying elections on the Continent has also passed mostly without incident. Meanwhile, corporate-friendly tax cuts are making headway in the US and the Trump administration has hinted at big-splash infrastructure spending early in the new year.

This masks an important vulnerability however. Broadly speaking, the MSCI World Stock Index has been locked in a nearly one-way uptrend since early 2016. Political and economic trends have waxed and waned over that time, and yet equities continued to march higher all the same. An important constant buoying prices has been the ever-growing size of monetary stimulus outside of the US. Indeed, while the Fed’s balance sheet has been drifting lower, the combined holdings of the ECB and the BOJ have added a dizzying $3.5 trillion just in the past two years.

An important change is looming on this front. The Fed is accelerating the unwinding of its balance sheet while the ECB will halve its QE effort to €30 billion per month starting in January. The BOJ continues to soak up assets with gusto, but its efforts would need to be increased dramatically to make up for what is lost in Fed and ECB support. That hurdle will look even more daunting when the Fed’s monthly asset roll-off begins to exceed the ECB’s purchases mid-year.

Markets are forward-looking. Investors will almost certainly consider the coming liquidity drain when making annual asset allocations at the start of the year though it will not hit critical mass until the second half. Further, the investment grade (lower risk) versus junk (higher risk) bond yield spread is back near pre-Great Recession levels, warning that the removal of monetary support may expose asset misallocation and trigger instability. All this might cool appetite for risky assets including equities.