After an incredible 5 quarter climb from the US Dollar to two-decade highs, the market suffered its worst three-month retreat since 3Q 2010 over the final stretch of 2022. To evaluate whether the Greenback has truly turned, it is important to assess what it was that charged the bulls in the first place. There were generally three macro factors that have supported the funnelling of capital towards the United States and its assets: a leading monetary policy advantage; a relative economic stability for a world still dealing with the aftermath of the pandemic and the Russian invasion of Ukraine; and the backdrop appeal for the ‘haven of last resort’. These advantages have shifted materially this past quarter. Fundamental polarity hasn’t necessarily shifted, but the scale of the premium has shrunk while the currency was still trading at rich levels. The questions heading into the opening quarter of 2023 are whether the discount the Dollar has been put through this past three-month leg leaves the market in balance and whether there are any severe ‘risk’ threats on the horizon.

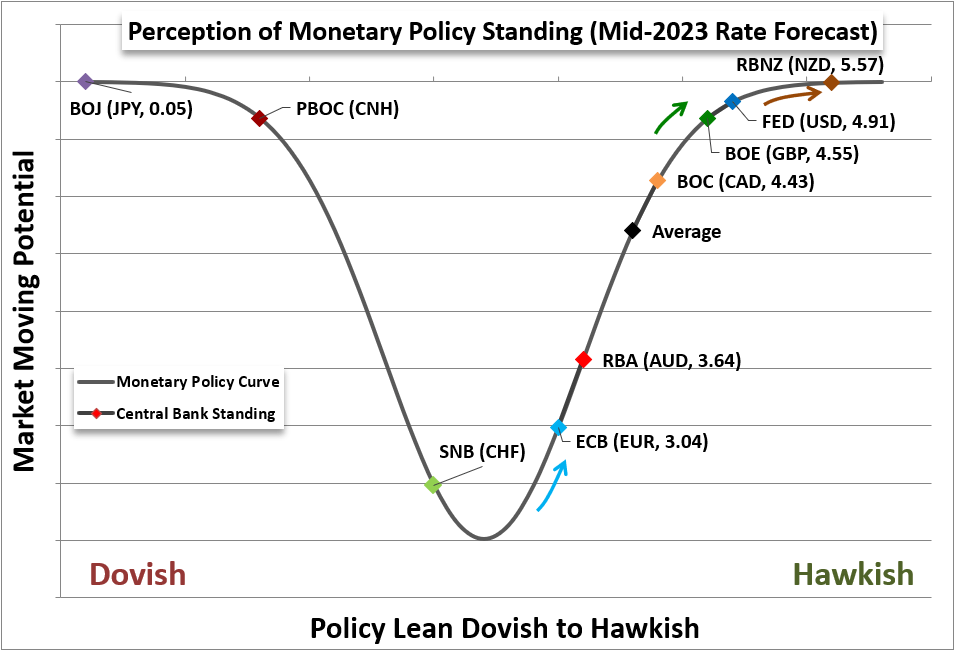

An Interest Rate Advantage That Is Increasingly Marginal

The Federal Reserve carries a greater weight over the global financial system than its peers owing to its size and the collateral of its economy. In the past year, there has been added weight from the lead it has taken amid the aggressive tightening regime from developed world central banks. After reversing course on the view that extreme inflation was ‘transitory’ the FOMC proceeded to increase its benchmark rate by 425 basis points in less than a year. That lifted its target range to 4.25 – 4.50 percent to close out the year at a yield advantage relative to most of its major counterparts, including the likes of the European Central Bank, Bank of England and Reserve Bank of Australia. During peak acceleration of the tightening phase the 75 bp tempo afforded the Greenback serious carry trade appeal – especially when there was an added sense of ‘risk aversion’ through the downward pressure on traditional speculative assets like equities. However, the ‘terminal rate’ is in sight for most major central banks. And, though the peak for the Fed sometime mid-2023 looks to be higher than many counterparts, the differential is increasingly marginal, and some counterparts are more open-ended as to when their inflation fight will end.

Chart 1: Relative Monetary Policy Stance

Created by John Kicklighter

The Lingering Threat of a Recession

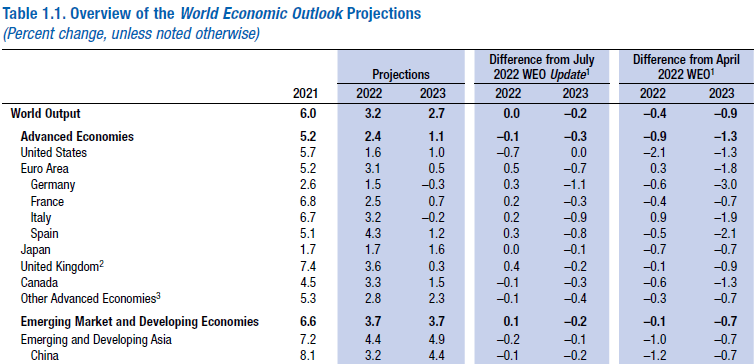

It triggered quite the debate back in the July when the NBER – the group the US government looks to in order to assess the economic situation – ‘clarified’ its determination of recessions. With the US economy heading for its second consecutive quarterly contraction in GDP, the group stated that the evaluation was more nuanced and based on intensity, duration and breadth among other factors. The official group may have adapted the official account, but the fears of economic struggle remain in the open market. With the Federal Reserve forecasting a tepid 0.5 percent GDP for 2023 in its December Summary of Economic Projections (SEP), it looks increasingly dubious to investors and citizens that the authorities are not affixing the label to the environment. That said, when it comes to the US Dollar’s perspective, the picture is relative. The IMF’s forecasts, which compare the major economies of the world, are still putting the United States in the upper half of developed world performance. So long as it maintains that stability and fends off the official recession call, the Greenback may continue to draw capital.

Chart 2: IMF WEO Economic Forecast from October 2022 Update

Source: IMF WEO for October

Your Safe Haven is Showing

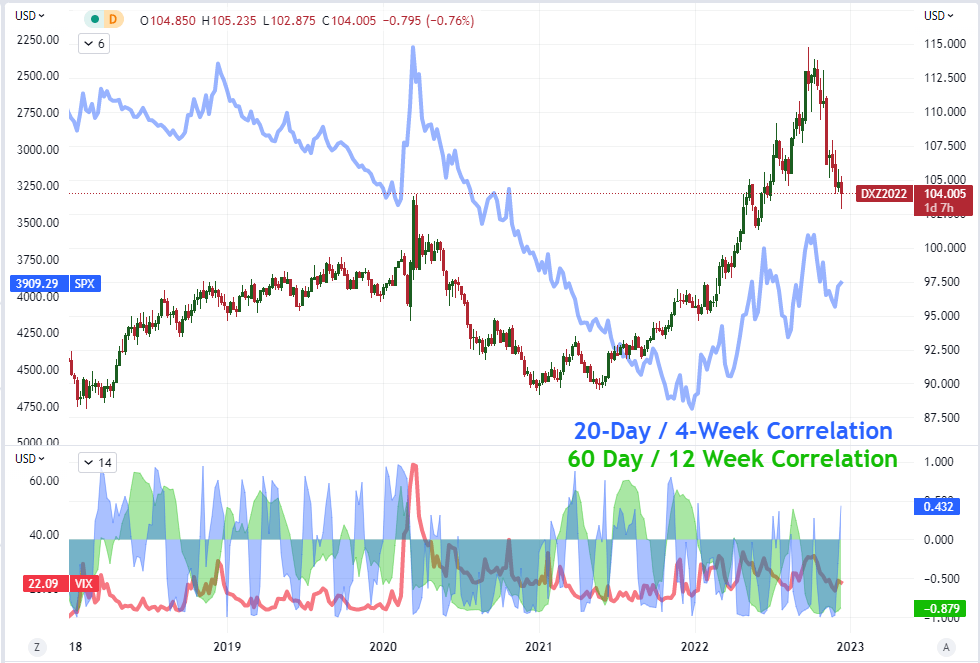

For much of 2022, it seemed that the relative pace of interest rates and rate forecasts was the guiding light for much of the FX market. However, through the final three months of 2022, that picture of influence started to shift. Despite the relative advantage of the Fed’s benchmark rate up through the last rate hike of the year and reiteration of a forecasted yield advantage into the following year, the Dollar continued to struggle. Notably, that divergence happened to occur at the same time the relationship between the Greenback and risk assets was tightening. Below is a chart that shows the relationship between the DXY Dollar Index overlaid with an inverted S&P 500. In general, when risk appetite slides, the Dollar has gained ground as a safe haven – hence one of the dominant trends of the past year. Yet, as the index has bounced in the fourth quarter, the Dollar has suffered its decade-busting drop. The technical correlation through the medium and long-term tends to fluctuate for this fundamental role, but perhaps the defining factor of the ebb and flow of the relationship is the intensity of risk trends themselves. In other words, if we come to a severe episode of fear for the capital markets in the opening quarter of 2023 (or later), it could be the catalyst for a strong Dollar recovery.

Chart 3: Chart of Dollar Index, Inverted S&P 500, 20 and 60-Day Correlation with VIX

Source: TradingView; Prepared by John Kicklighter