S&P 500, Dow, GBPUSD, VIX, EURUSD and USDCNH Talking Points:

- The Market Perspective: USDJPY Bearish Below 141.50; Gold Bearish Below 1,680

- Markets continued to suffer under the strain of risk aversion this past session, but technical moves like the S&P 500’s new 22-month low didn’t really evoke a sense of a true ‘break’

- Event risk looks to thin out over the next 24 hours; but undercurrents of recession fears, volatility and engrained risk aversion can keep the market sliding

S&P 500 and Volatility: Risk Aversion Without Critical Technical Milestones

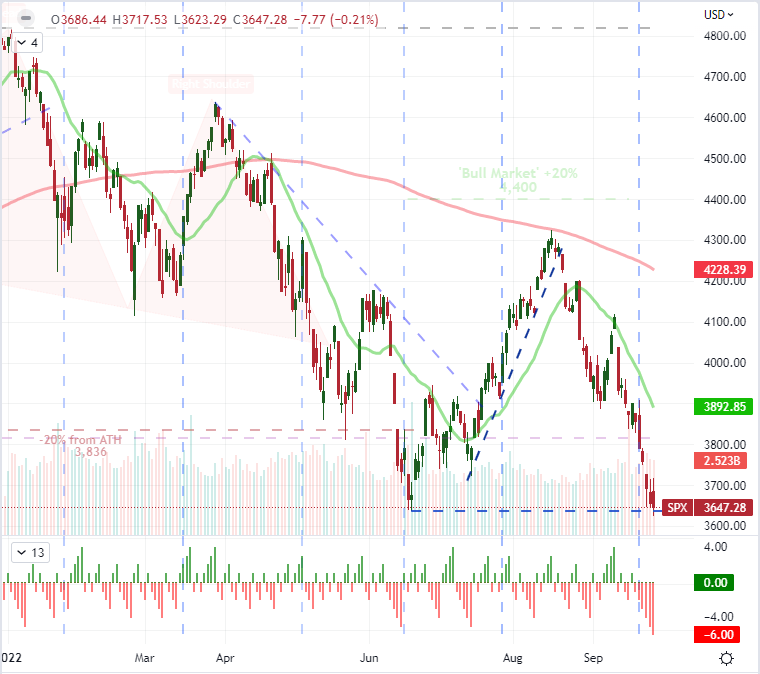

While there are hallmarks for a financial backdrop that can usher in a self-sustaining risk aversion, markets rarely move in a straight line. For the progress in risk benchmarks this past week and throughout 2022, it is not a stretch to say that bears have exerted serious control. On the other hand, there wasn’t a whole-hearted collapse to be found through the typical sentiment channels that I monitor. Freshly securing its official ‘bear market’ designation at the start of this week, the Dow Jones Industrial Average extended its slide alongside the German DAX, UK FTSE 100 and Hong Kong Hang Seng indices. Add to that mix the drop form the EEM emerging market ETF, HYG junk bond measure and a range of Yen-based carry trades; and the winds seem fairly clear. That said, the S&P 500 couldn’t truly clear the June 17 swing long. Tuesday’s close was lower than that of June 16th and its intraday low surpassed the reach of the 17th. Yet, it doesn’t register as a clean break from a technical perspective – and that is on the back of a six-day slide, the longest since February 2020. Is it merely a matter of time for momentum to drag it lower or is this symbolic reticence due to spread.

Chart of S&P 500 20 and 200 Day SMAs with Consecutive Candles (Daily)

Chart Created on Tradingview Platform

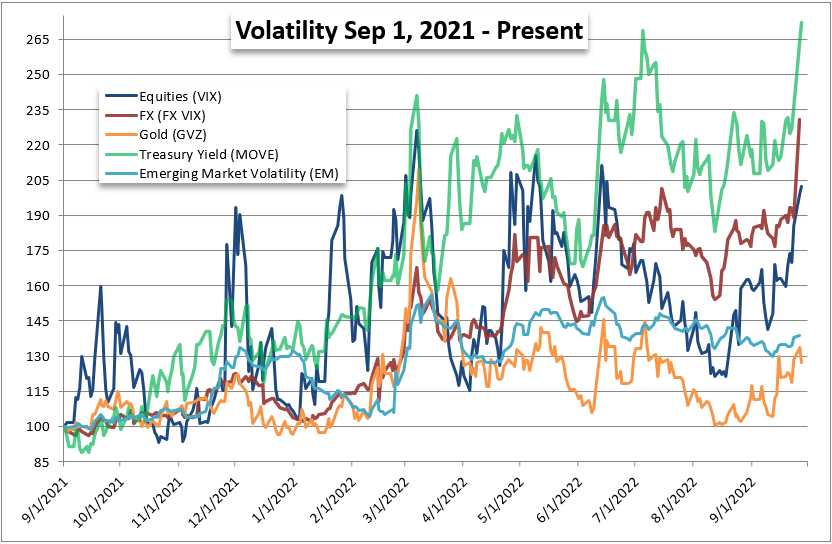

Technical barriers can prove their own catalyzing points for the market, but it seems that systemic fundamental themes and more element market conditions are exacting a greater influence on the financial system at the moment. Where my concern is most focused at the moment is the state of stability in core asset classes. Liquidity plays a role in that core health, but volatility is just as important a factor. And when it comes to activity levels, conditions are remarkably extreme. Equities and the VIX volatility index represent they greatest recognition amongst traders, but the asset’s expected (implied) levels are far from the capitulation that so many are trying to spot. The measure is above 32 and at its highest levels in three months, but I consider a ‘flush’ more associated to charges closer to the 50 mark. More interesting at the moment is the level of implied volatility reflected in the FX market and Treasury yields which speaks to troubles closer to the core of the financial system.

Chart of Different Asset Class’s Volatility Measures Year-Over-Year

Chart Created by John Kicklighter

US Data Facile Improvement and Dollar Is Still the Safe Haven

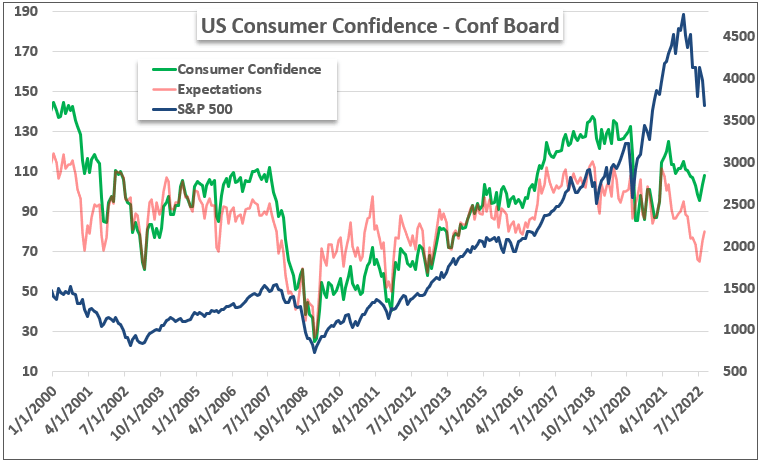

There is a phenomenon in markets whereby good news can render ‘negative’ market response and vice versa. That atypical response is less often a deep complexity in the data and more frequently a skew in underlying priorities that I consider a sign of ‘market conditions’. This past session, there were two important US economic updates that could have been readily designated fuel for the bears. The Conference Board’s consumer confidence survey for September improved more than expected (from 103.6 to 108) while new home sales through August increased a remarkable 29 percent (the second biggest leap in notional change on record). That could be seen as a boon for keeping the economy bolstered, but there is plenty of skepticism around the course of both data streams and it could collective been seen as further motivation for the Fed to keep up its aggressive inflation fight.

Chart of S&P 500 overlaid with Conference Board Consumer Confidence Survey (Monthly)

Chart Created by John Kicklighter with Data from Conference Board

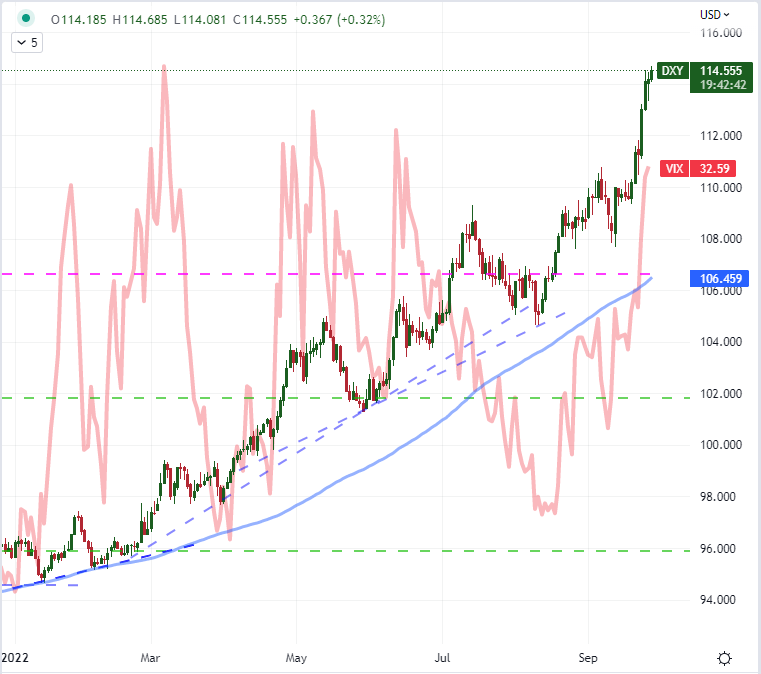

Notably, with the data released this past session, the DXY Dollar Index ultimately pushed to fresh two-decade highs for a third successive session through Tuesday. There are a few key roles that the Greenback plays, and determining which course we are ultimately following can offer meaningful insight into the financial system. Interest rate differentials are important but the fourth 75bp rate hike at the November 2nd meeting has actually dropped back 15 percentage points (to 57 percent probability) through this past session. As for the relative growth advantage that has kept EURUSD under power, there is serious skepticism that the housing and sentiment data will hold out for the world’s largest economy. That leaves the safe haven appeal of the US currency. As volatility rises, there is intensified appetite for the harbor that the Dollar (with a destination of Treasuries and money markets) represents. I’ll keep tabs on the VIX and EVZ in its relationship to the DXY.

Chart of DXY Dollar Index with 100-Day SMA Overlaid with VIX Volatility Index (Daily)

Chart Created on Tradingview Platform

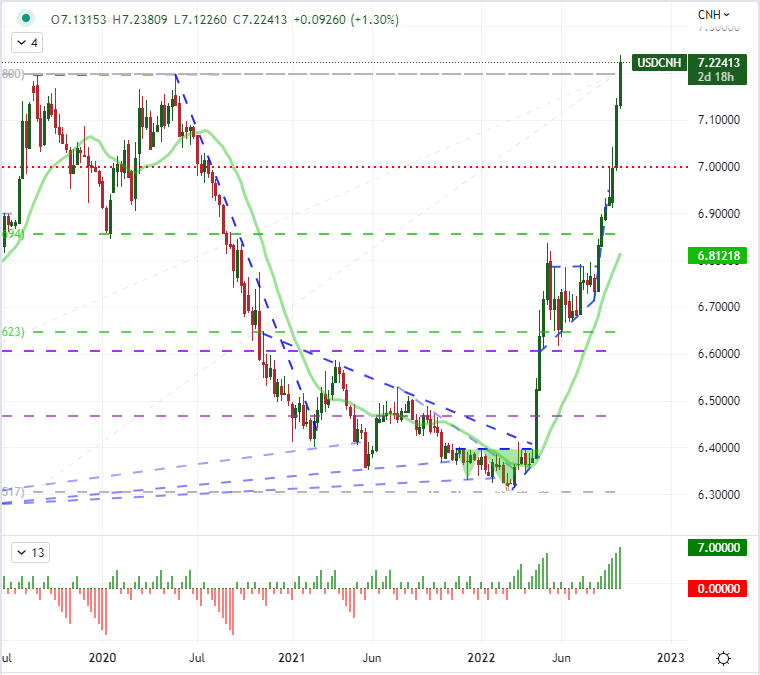

USDCNH and Other Dollar Crosses, Event Risk Ahead

When its comes to the fundamental insight that the Dollar offers, I still believe that different pairs present a different priority. For EURUSD, the relative economic consideration remains a principal focus considering the ECB is attempting to accelerate its own rate forecasts and the safe haven – risk comparison is still suppressed owing to the liquidity of the two currencies. USDJPY is a function of all three of the terms at once while GBPUSD has similar moorings though its recent volatility puts the onus on the safe haven function. The pair that is more interesting to me at the moment is USDCNH. The US Dollar extended its seven week rally with a seven-day climb that has now cleared the highs just below 7.20 set back in 2019 and 2020. Back then, crossing through 7.0000 was considered political move by Chinese authorities to offset the impact of sanctions. They may be ‘allowing’ the Yuan depreciation now as a means to bolster trade in strained times, but it is just as likely that they are struggling to keep the tide back. Whether through intent or incapacity, this pair’s climb is telling.

Chart of USDCNH with 20-Week SMA and Consecutive Weekly Moves (Weekly)

Chart Created on Tradingview Platform

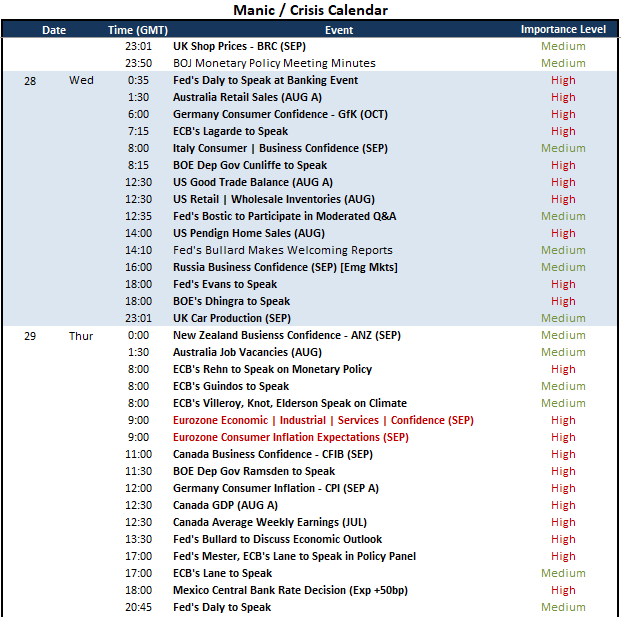

Looking for the fundamental motivation to spur full technical breaks and inflame the market conditions that have created such perilous backdrop, there is notably less in the way of overwhelming fundamental event risk set for Wednesday release. I will be watching the run of US data that can offer insight on the economy such as the trade balance, retail and wholesale inventories and pending home sales figures. Yet, that is not top tier and timely event risk. Central bank speak is another area of interest – particularly for the Fed, ECB and BOE; but it will take serious escalation to further the fear – or reverse it. For priority, I will be looking to systemic discussions, then headlines and finally the economic calendar.

Critical Macro Event Risk on Global Economic Calendar for the Next 48 Hours

Calendar Created by John Kicklighter

{{NEWSLETTER}}