S&P 500, Dollar, Fed Forecast, Recession Risks and Liquidity Talking Points:

- The Market Perspective: USDJPY Bullish Above 141; EURUSD Bullish Above 1.0000; Gold Bearish Below 1,750

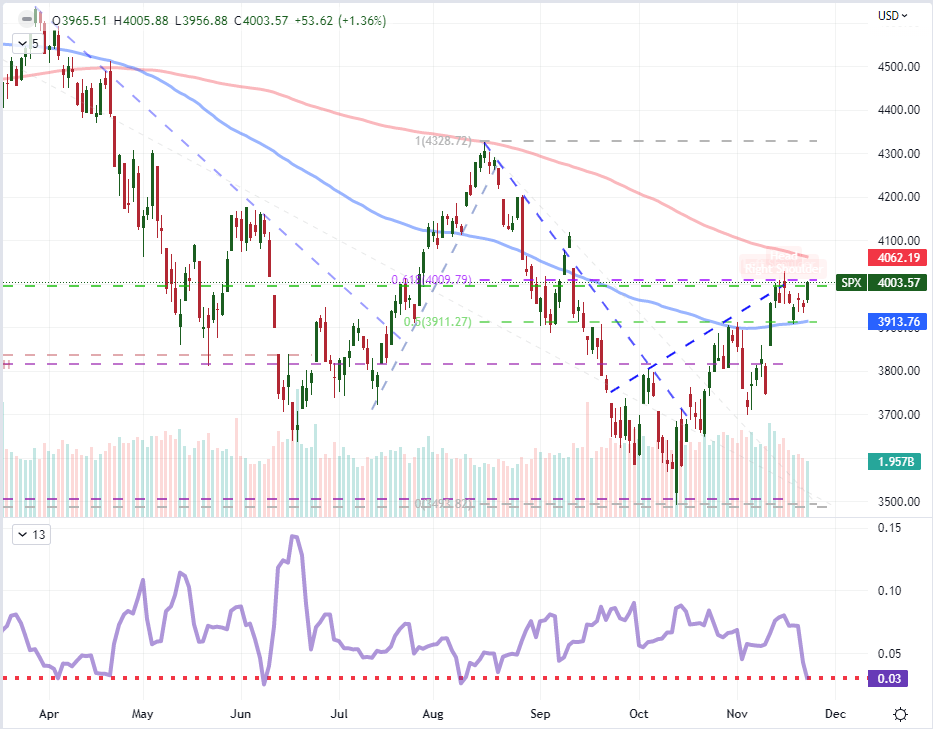

- The consolidation continues for the S&P 500 with an 8 day range that is among the smallest we have seen in 2022

- Headlines around recession risks are elevated between the OECD’s forecasts and November PMIs ahead, but is that enough for a pre-liquidity drain break for capital markets?

We are starting to see the markets pulled between two perspectives. On the one hand, there is the narrow technical patterns developing for benchmarks like the S&P 500 along with some smattering of systemically-important macro updates. Alternatively, there is the consuming expectations of a known liquidity drain this week in the Thursday Thanksgiving holiday. These are contrasting forces that can translate into difficult conditions for the short-term oriented trader. Heading into Wednesday trade, the risk of a technical break from the SPX seems high. The 10-day (two week) average true range on the index is 1.8 percent and the past 8-day range is the smallest we have seen in over three months. Thin liquidity can amplify volatility and we are near the upper threshold of the range. However, if there is a break, the immediate loss of liquidity for the following holiday in the US (Thanksgiving) will leave us with a long break to contemplate the true conviction of any provocative moves. If on the other hand, volatility caters to ‘risk aversion’ it could be a move within an establish congestion which markets may be more willing to evaluate in the short-term and then take up a new perspective when liquidity is restored.

Chart of the S&P 500 with 100 and 200-Day SMAs and 1-Day Historical Range (Daily)

Chart Created on Tradingview Platform

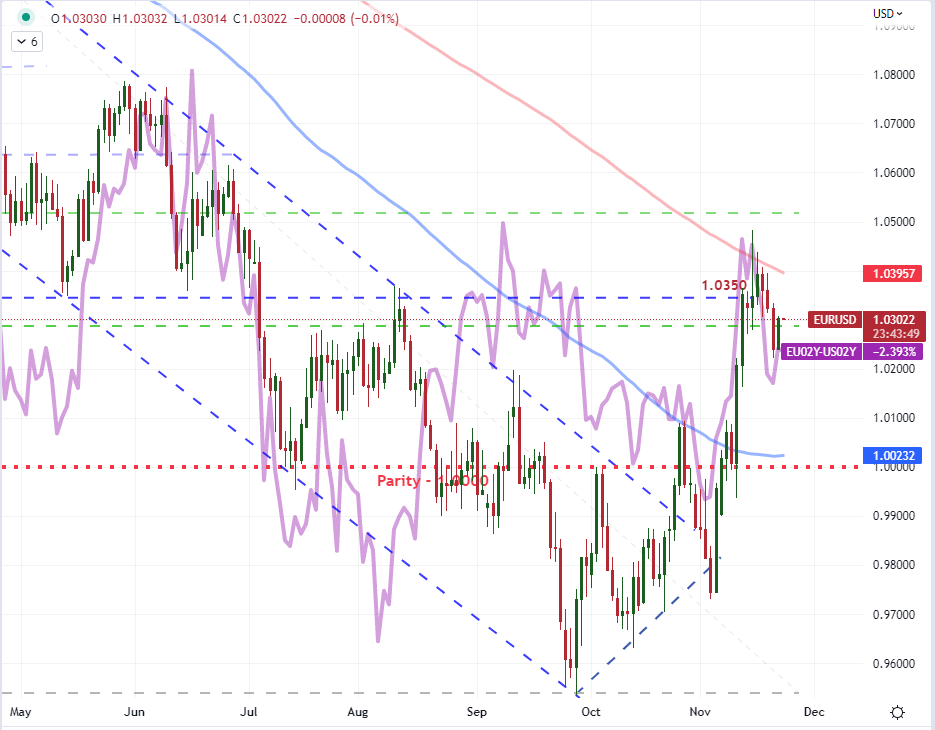

For fundamental motivation, there remain two themes of interest and capacity to move markets. Interest rate expectations has been one of the more productive drivers for the US Dollar of late, but the Greenback seemed to waver in its recover this past session. That could a mirror of the equities rally as the Dollar reflects upon its safe haven status, but that is a weak fundamental hold of late. Perhaps the OECD’s update carried some specific weight for the greenback and EURUSD specifically. Among their growth forecasts, the economic group would also upgrade their inflation forecasts. Through 2023, the OECD expects inflation worldwide to be 6.6 percent. Most major central banks target 2 percent, which is strong incentive for hawkish policy groups to stay their course. That would seem more a driver for the Dollar than any other central bank considering it is leading the way; however, the OECD called out the ECB in particular saying it needs to close the gap between its rate and that of its US counterpart’s. Will they heed the call?

| Change in | Longs | Shorts | OI |

| Daily | -9% | 1% | -4% |

| Weekly | -24% | 41% | -2% |

Chart of the EURUSD with 100 and 200-Day SMAs Overlaid with EU-US 2-Year Yield Spread (Daily)

Chart Created on Tradingview Platform

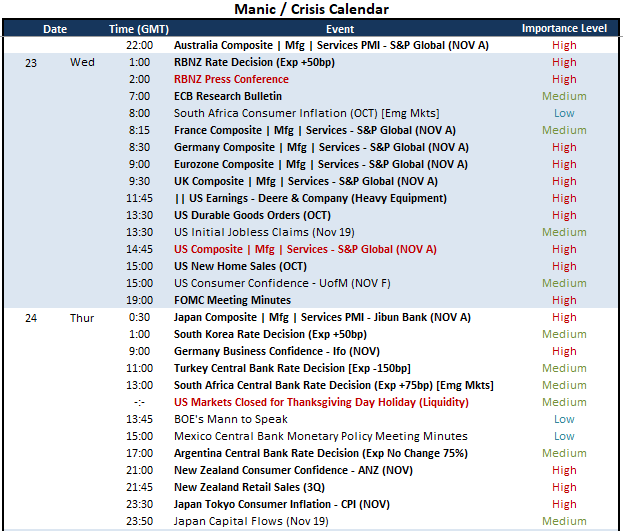

For scheduled event risk over the next 24 hours, there is more fodder for both rate forecasts and growth assessment. Yet, I believe the interest rate speculation will likely take a back seat, with the exception perhaps of the market’s reaction to the RBNZ’s rate decision. That is a direct policy update, they are expected to hike 50 basis points and the New Zealand Dollar has spent a few steady months of trying to recover lost ground to its discounted role as a renowned carry currency. More representative of a fundamental theme Wednesday is economic health. We have a few key earnings (Deere) as well as a smattering of US economic data that is worthy of observation (durable goods and new home sales). However, there is something more comprehensive we may find the market more inclined to digest.

Critical Macro Event Risk on Global Economic Calendar for the Next 48 Hours

Calendar Created by John Kicklighter

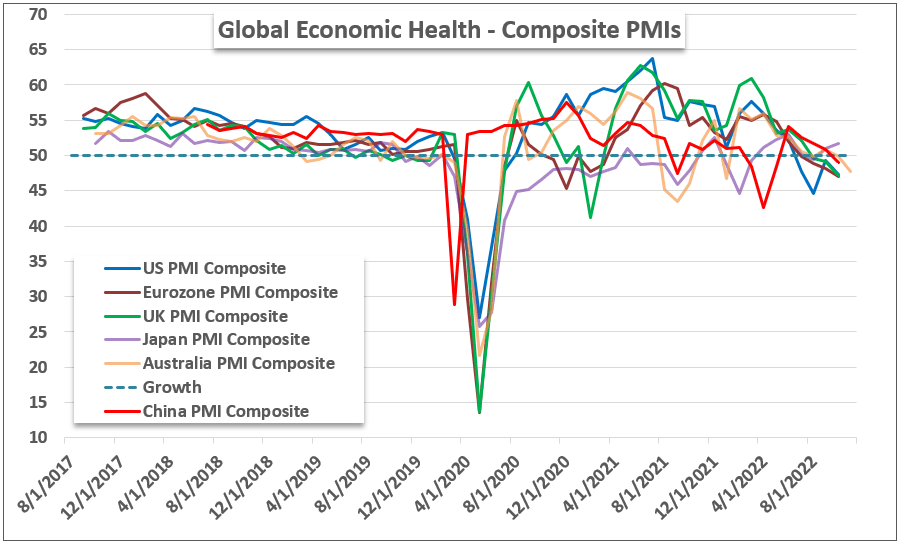

More comprehensive on the growth side of things is the insight we are set to receive on the current actual health of a group of major developed world economies. The S&P Global PMIs are closely watched and timely proxies of GDP for the target economies. At the time of writing, the Australian data was already released and the slide in the composite figure from 49.3 to 47.2 is not a favorable start. All but Japan was in contractionary territory (below 50), so the backdrop will carry some fear in its anticipation. That may make for a greater surprise should the data ‘beat’, but starting a risk run in the twilight of liquidity would likely be more difficult to muster than seeing an unwinding of loosely held risk exposure before Thanksgiving liquidity sets in.

Chart of Global Economic Activity from Monthly PMIs (Monthly)

Chart Created by John Kicklighter with Data from S&P Global

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team