US Dollar Fundamental Forecast Talking Points:

- The DXY Dollar Index dropped -1.7 percent this past week – the second biggest drop in a year – but the top CPI release rendered much less traction than in November

- Moderating interest rate forecasts from the Fed and a tempered risk aversion current have helped extend the Dollar’s retreat from two-decade highs three months ago

- With the market’s own Fed Fund futures holding level and the VIX already pushing 12-month lows, the risk is more acute for a bullish fundamental charge for the Greenback

Fundamental Forecast for the US Dollar: Bullish

We have closed out the second week of 2023, and it was not a good period for the benchmark Dollar. Seemingly building on the failed recovery and subsequent retreat of the previous period, the DXY Dollar Index put in for a distinct -1.7 percent drop through this past week. Not only was that the biggest slide for the currency over that interval, it would also push the benchmark to its lowest level in seven months. Over the past three months, the Dollar has dropped over -11 percent from its peak, two-decade high in late September. Given its starting point, there was likely considerable premium behind the currency which was founded largely on the pace of relative benefits from Fed rate forecasts to economic potential to its position as a safe haven amid a struggling equity market. Yet, with the capital markets leveling out and the outlook for the benchmark US rate leveling out, much of that tangible charge has evaporated. The question is how much of that bullish premium was ‘loosely held’?

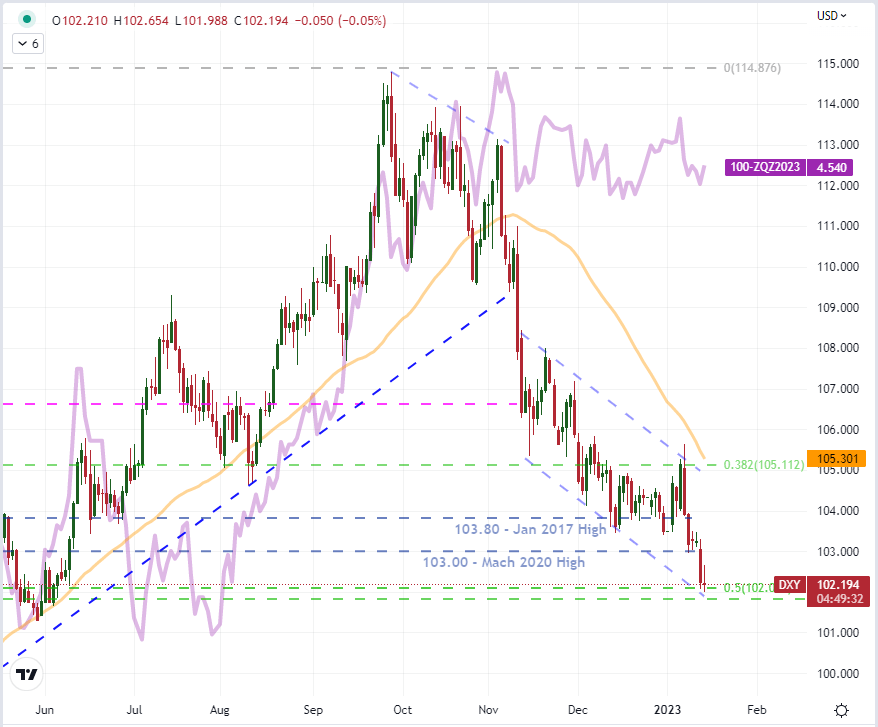

From the technical side of things, it is worth noting that we will enter the holiday shortened week with the DXY at the midpoint of its 2021 to 2022 bullish charge (an incredible 28 percent climb over 16 months). Pulling the market back below the 2016 and March 2020 peaks, it is likely that sheer momentum will start to shift to tangible fundamental assessment. In terms of the deflating benefit of a hawkish Federal Reserve, the market’s challenge of the central bank’s credibility in projecting a terminal rate around 5.1 percent this year with possible cuts later in the year is significant. On the other hand, even the market’s view of the US rate forecast has leveled out rather than significantly retreated over the past few months. As you can see below, the disparity is growing significant.

Chart of DXY Dollar Index with 50-Day SMA, Overlaid with Fed Funds Implied Rate for Dec 2023 (Daily)

Chart Created on Tradingview Platform

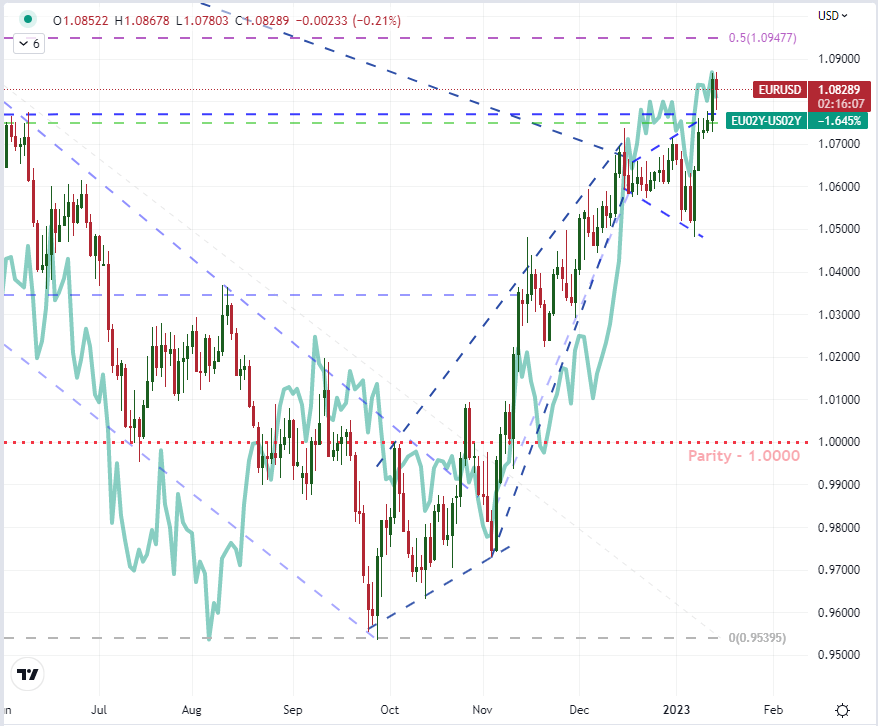

Of course, when it comes to a relative value metric like interest rates, it is important to consider the counterpart to the US forecast. Given that the DXY is trade-weighted and thereby heavily weighted towards EURUSD, we can see where some of the more recent headwinds for the Greenback have come through. The rate forecast for the ECB was previously grounded at its negative rate as the central bank delayed in following its global peers, prioritizing recession risks over the inflation fight. Yet, the European group eventually capitulated and found itself in a position of catch up – and the market having to quickly reprice its outlook. That comparison considered, the question for EURUSD, and thereby the principal component for the Dollar, rests more with how much discount there is still built into the Euro’s backdrop. There isn’t a lot of event risk on tap for this week to clarify that side of things, which undermine the recent technical break and traders appetite for momentum.

| Change in | Longs | Shorts | OI |

| Daily | -1% | -4% | -3% |

| Weekly | 4% | -10% | -5% |

Chart of EURUSD Overlaid with the EU – US 2-Year Yield Spread (Daily)

Chart Created on Tradingview Platform

The other important fundamental undercurrent for the Dollar moving forward is the general sentiment of the global markets. Often referred to as ‘risk trends’, this general mood of the financial system tends to be a universal influence that can represent a bulk of the market’s evolution over time. Given the Dollar is the world’s most heavily used currency (by far) and is the pricing basis for the top risk-free asset (Treasuries), its connection to risk as a safe haven is meaningful. Below, the relationship between DXY and the VIX volatility index (strongly inversely correlated to its underlying S&P 500 index) is clear and strong. The technical relationship does wax and wane in intensity over time, but at present it seems to be high given the rebound in equities. Yet, where is the potential most intense moving forward? A further recovery in confidence is possible, but it would likely be slow as the onus of inflation, interest rates and troubled growth untangle. Alternatively, the chances of a sudden slump associated to just a jump in probability of future recession make for a more loaded scenario (though that doesn’t speak to probability of outcome). In short, if the VIX jumps and risk assets swoon ahead, it could help boost the Dollar from its lows.

Chart of DXY Dollar Index Overlaid with the VIX Volatility Index (Daily)

Chart Created on Tradingview Platform

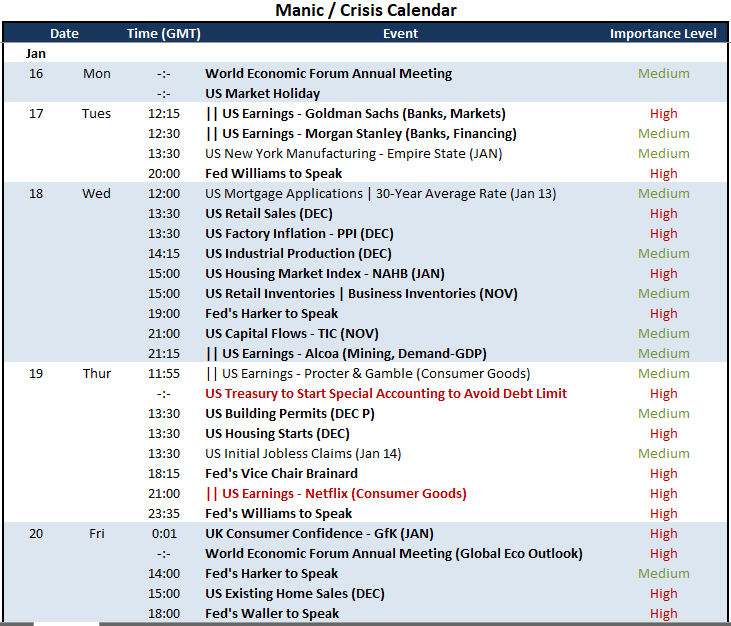

For top scheduled event risk over the coming week, the US docket is not stocked with the highest possible event risk. There is no datapoint with the same anticipation equivalence of a CPI or NFPs nor is there any official monetary policy update to hone in on. Furthermore, US exchanges are close Monday for the Martin Luther King Jr holiday, which will impact liquidity and temper any nascent or errant fundamental swells. Aside from Fed speak and some second tier monthly economic reports (retail sales, NAHB housing market), I will be watching earnings with Netflix playing an uneven usher of the top tech stocks which will report a following week. Then there is also the wild card threat of the US debt limit being hit on the 19th. The Treasury can use account tricks to avoid default for a while, but don’t underestimate the risk this represents. The Standard & Poor’s downgrade of the US sovereign credit rating from its AAA peak is a lesson on what can happen with brinkmanship in the markets.

Top US and Global Macro Event Risk Next Week

Calendar Created by John Kicklighter