Talking Points:

- Seasonality norms suggest the Summer Doldrums are passing and more active market conditions are on the way

- While volatility (VIX) traditionally peaks while SPX suffers on avg its only loss in September, structural issues remain

- Trading a turn in liquidity and more active markets can be done with VIX futures, VXX, XIV, breakouts and risk-linked markets

Want to ask questions about how volatility and participation can alter trading conditions? Curious about what strategies are best adatped to such systemic changes? Bring your market, trading and strategy questions to the weekly Trading Q&A on Tuesday. Sign up on the DailyFX Webinar calendar.

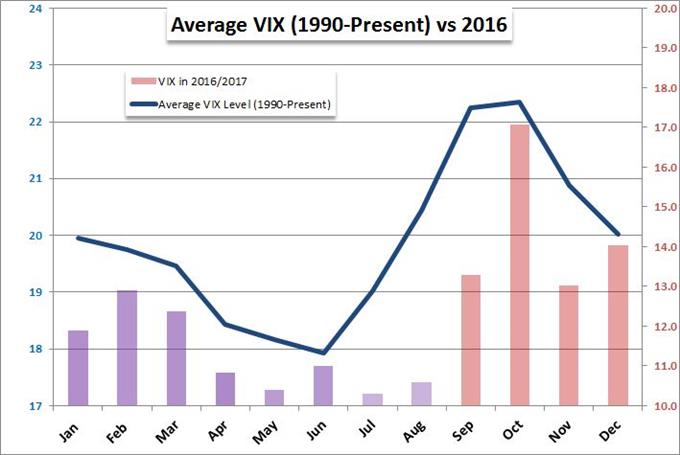

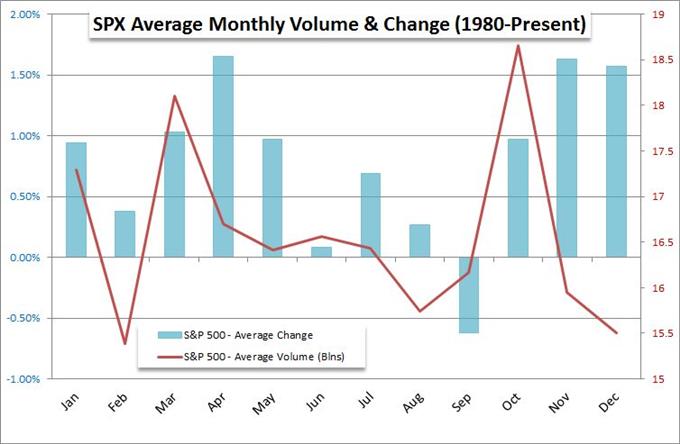

Historically, markets are set to mark a serious reversal in both activity and volume in the coming days and weeks. Seasonality studies - evaluating regular patterns over time - shows that both participation and volatility pick up significantly over the coming month. Using the S&P 500 as a benchmark for 'activity' and risk lean, we find that volume for the benchmark equity index historically rises from the quietest month through the calendar year when adjusted for trading days and holidays (August). More signficant in the comparison though is the fact that on average September marks the only month in which the equity index actually declines. Consider that historical norm with the same monthly breakdown for the VIX volatility index. September and October average the most active months of the year for the 'fear' gauge. That suggests the Labor Day holiday in the US is a transitional period for the markets from quiet to active.

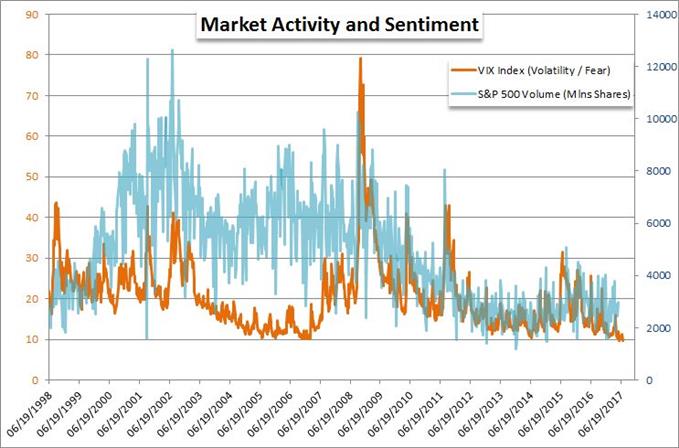

The seasonal norms do not promise an alleviation of the stuctural curbs on the market, but that can help to usher in the ultimate change by facilitating catalysts that come along the way. How many times have we seen high profile events such as US debt cliffs, Chinese financial scares, and sudden bouts of volatility in the financial system seize the markets attention and pass with little lasting influence on bearing or activity level? That complacency has been promoted by deep structural considerations like the ballooning stimulus infusions by the world's largest central banks. However, those conditions are both temporary and changing - effectiveness of monetary policy fading in the case of central banks. What's more, the ability to 'ride out' meaningful developments has been facilitated by stability in the form of low volatility and thin volume that has kept the markets from metabolizing meaningful reversal in course. There is a material, positive relationship in VIX (volatility) and volume (for the S&P 500). There is an even sharper connection between volatility measures and the bearings of traditional 'risk' assets. And, if we are to see a genuine 'risk aversion' move, years of speculative build up will likely make for a substantial move.

For practical trading of this systemic shift, only the most patient and convinced of impending risk bearing change should consider long-term positions on risk aligned benchmarks. The more dynamic approach to our current conditions are those assets with a more levaraged relationship to this dynamic change. The VIX-related assets are among the most direct exposure. Futures representation of the instrument carry the fewest add-on issues. Though popular, the leveraged short-term VXX and inverse XIV ETFs should only be considered by those certain of timing and familiar with the pricing issues related to these and oher ETNs. Options are more familiar with the considerations of implied volatility and time with a market that can run the entire financial system (so long as their are derivatives to be found). That said, a deeper knowledge of the product is necessary to succesfully navigate. For those in the spot market, there are risk-oriented standards that more readily respond to conditions. Global equity indexes, emerging market benchmark and currencies, Yen crosses and even the EUR/USD are good example of what markets can move should they be genuinely motivated. Even strategy can and should be adapted to account for such high profile changes. We discuss how to trade a shift in volatility and volume that seasonal conditions suggest is ahead in today's Quick Take Video.

To receive John’s analysis directly via email, please SIGN UP HERE