S&P 500, Dollar, DAX and Bitcoin Talking Points

- There is a very material gap in risk trends through the rest of this week owing to the US Thanksgiving holiday, which will materially undermine trend development

- Thinned liquidity can amplify volatility in risk outlets; and I will be referring to the DAX 40, Bitcoin and Turkish Lira for a guide on speculative activity

- Thematically, monetary policy remains a key theme for the markets with Fed intent shifting to the policies of the ECB, BOE, South Korea central bank and more

Market Conditions Amplify Volatility but Curb Trend Potential

We are heading into the a well-known liquidity drain for the US markets, and the absence of this big player in global sentiment historically distorts global markets. In more normalized conditions, this past session’s data run could have very well generated more substantial trend out of the otherwise directionless volatility that we would ultimately register. The US docket in particular was thick with meaningful event risk. The October trade deficit dropped sharply, initial jobless claims dropped to a half century low and consumer spending swelled a greater than expected 1.3 percent. The growth implications from this mix though was outstripped by the Fed’s favorite inflation indicator: the PCE deflator. The price gauge accelerated to a 5.0 percent clip – the fastest in three decades – which gave serious context to the FOMC minutes which showed serious debate over the tempo of the central bank’s tempo for tapering and openness to earlier rate hikes. Monetary policy will continue to be a prominent market theme moving forward, but the United States’ focus will blur for at least a few days. But that shouldn’t be read as a cap on volatility and market development across the spectrum through the rest of the week.

| Change in | Longs | Shorts | OI |

| Daily | 1% | -1% | 0% |

| Weekly | 15% | -13% | -1% |

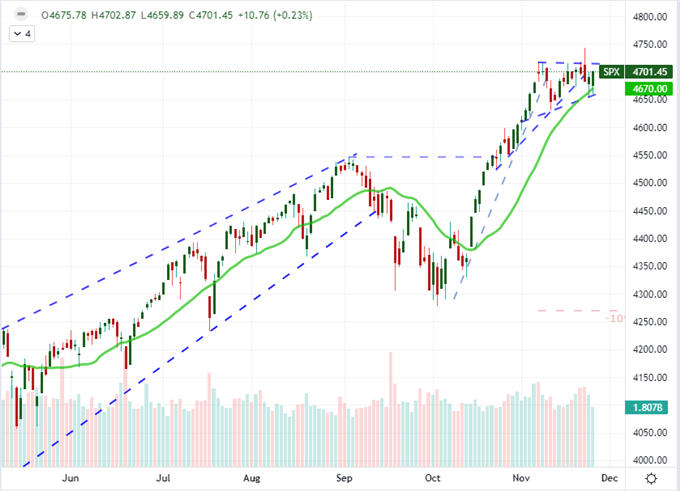

Chart of S&P 500 with 20-Day SMA, 5-Day Historical Range and Daily Wicks (Daily)

Chart Created on Tradingview Platform

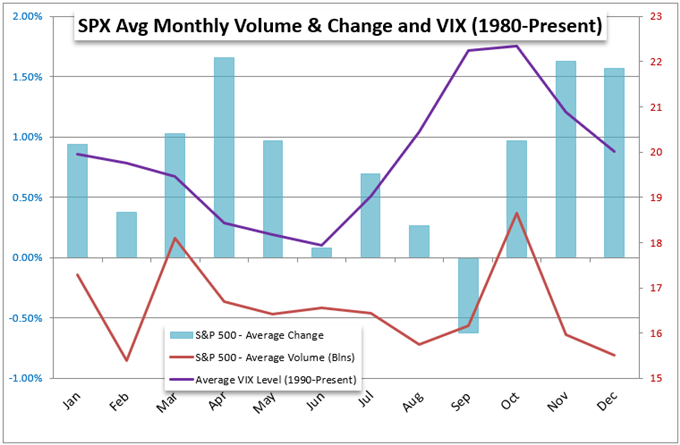

To be sure, the number one market influence that I’m considering for the final 48 hours of trade this week is the influence that liquidity will have over activity. US exchanges are closed across the board Thursday, but they do reopen on Friday. History suggests that there is limited traction to be found in the second half of this holiday week, but it is by no means certain. One of the very important by-products of thin liquidity is a propensity for sharper volatility events. When there are fewer market participants on hand, an unexpected development can rip through the entire market very quickly; and the lack of ‘the other side’ to absorb the interest can translate into more dramatic but short-lived action. We registered some of that phenomena through the first half of this week as the S&P 500 produced a bullish and bearish break on a terminal wedge without committing to direction on either move. It’s also important to recognize that next week brings the new – and final – trading month. While similarly plastered with bullish expectations that earn the ‘Santa Claus rally’ moniker, it comes with noticeably lower volume and volatility expectations.

Chart of S&P 500 Monthly Performance, Volume and Volatility

Chart Created on John Kicklighter with Data from S&P

Top Themes and Event Risk Through Week’s End

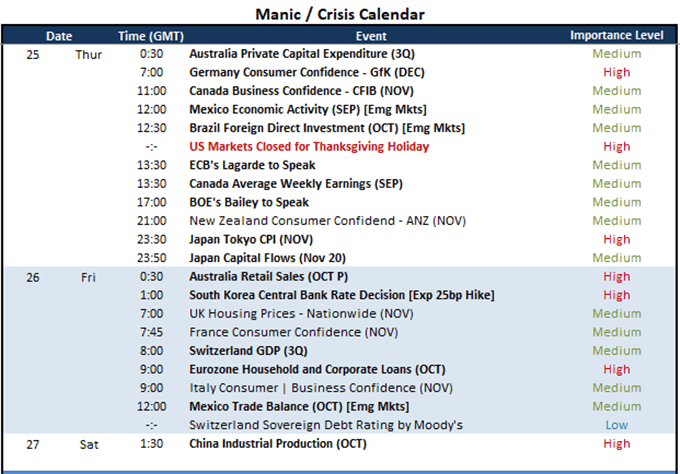

Looking for fundamental activity through the final 48 hours of trade this week, there is both scheduled event risk and generally unresolved systemic themes to consider. On the data side, today’s session hosts the sentiment surveys from Germany (consumer), Canada (Business) and Mexico (economic). Through Friday, Australian retail sales, Swiss 3Q GDP and Eurozone loans is much more specific in localized event risk. Through all of this data, EURCHF will be the most interesting target given the data will test a pair that very notably slipped below 1.05 – what was generally considered to be an unspoken floor for the SNB given their experience with trying to hold up 1.20.

Calendar of Major Macro Event Risk Through Week End

Calendar Created by John Kicklighter

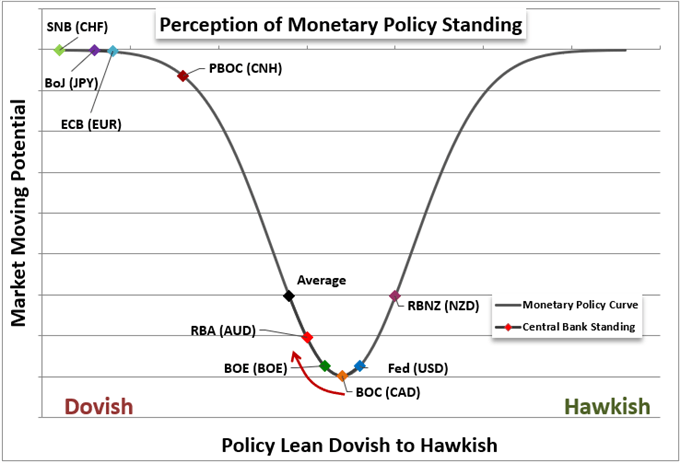

For general theme, the holistic ‘risk trends’ will always be on my radar. That said, it seems improbable that that investing rank still active in the market will be able to meaningfully change the course of the complacent bullish interest that has kept US indices Fed. That said, there are many fundamental tributaries that will eventually carve out a new course for markets further down river. Monetary policy remains my principal concern. With Fed Funds futures projecting more than two full hikes from the US central bank next year, there is a propensity for other major groups to share in this speculation. ECB President Christine Lagarde has actively tried to push back on the hawkishness at her own door, and she is likely to do so in scheduled speeches Thursday and Friday. BOE Governor Andrew Bailey is more on the fence, so his remarks at 17:00 GMT Thursday should be watched closely.

Chart of Perception of Relative Monetary Policy of Major Central Banks

Chart Created by John Kicklighter

Alternative Risk Measures: DAX 40; Bitcoin and USDTRY

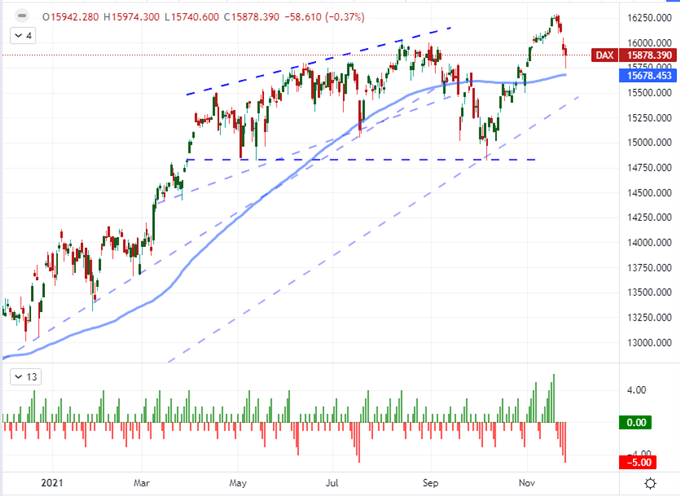

With the US markets taking a step back, it is important to keep tabs on other measures that can stand in for acting as a barometer for broader sentiment trends. Equities remains one of the top performing assets across the financial system over the past decade; but in the absence of the leading S&P 500 and crew, we could get a very different impression of market sentiment. That’s because the relative US to ‘rest of world’ comparison has pushed to a record high through Wednesday. Nevertheless, I will be watching the likes of the Nikkei 225 (Japan), Shanghai Composite (China) and FTSE 100 (UK) moving forward. My top lister though will be the DAX 40 (Germany) given that index has slid for five consecutive sessions while covid cases and deaths have soared to pressure a political decision on the keeping the economy fully open.

Chart of German DAX 40 Index with 100-Day SMA and Consecutive Candles (Daily)

Chart Created on Tradingview Platform

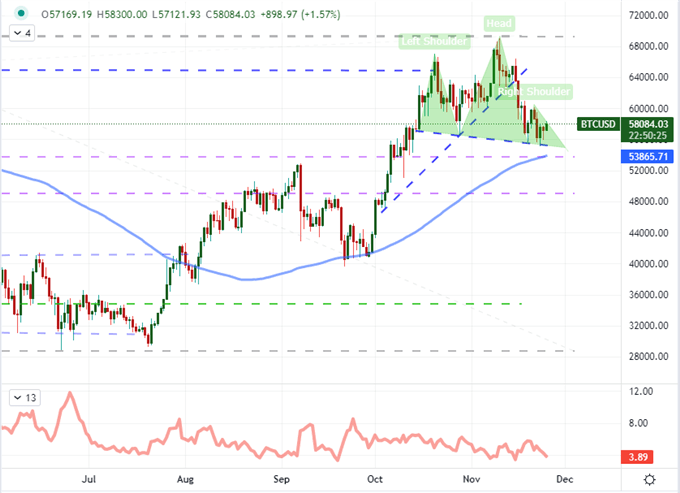

My other milestone for sentiment straight through the weekend is the crypto market. While there are many that believe this is the future of finance; for now, there is a disproportionate interest from speculators for the time being. In fact, Bitcoin’s 60-day (three month) correlation to the S&P 500 is a robust +0.69 (meaning the two tend to move in the same direction at generally the same tempo. What’s more, there is a unique characteristic of this market whereby it is not based on a centralized exchange; so there is active trading through holidays and the weekend. This makes it an appealing outlet for traders that are looking for a volatile outlet during a liquidity drain.

Chart of Bitcoin with 100-Day SMA and 20-Day ATR (Daily)

Chart Created on Tradingview Platform