Recession Talking Points:

- Anticipation remains the most overpowering influence in the speculative markets with the Fed Symposium anchoring late-in-week top events

- US President Donald Trump remarked Tuesday that a 'two month recession' may be necessary to ensure effective trade pressure on China

- Dollar is fully discounting White House Fed demands, Euro held steady despite Italian PM resigning, Pound traders still aware of Brexit

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Trump Suggests a 'Brief' Recession May be Necessary

The markets are clearly distracted by the fundamental weight of the high-level gatherings scheduled through the end of this week. If it weren't for the Jackson Hole Symposium and G-7 summit scheduled over the weekend - and a considerable amount of market-throttling complacency through seasonal liquidity conditions - some of the headlines that crossed the wires this past session would have likely sent the market reeling. The most incredible remarks this past session would come once again from the US President, Donald Trump. In a wide-ranging talk, the leader of the world's largest economy stated clearly that a US recession may be necessary in order to ensure the trade war with China finds its mark and inspires permanent change in what it believes are unfair trade practices. That is as clear an indication of priorities for the Adminstration as we have seen. In short, White House would not back off the fight should the world's largest economy tip into recession.

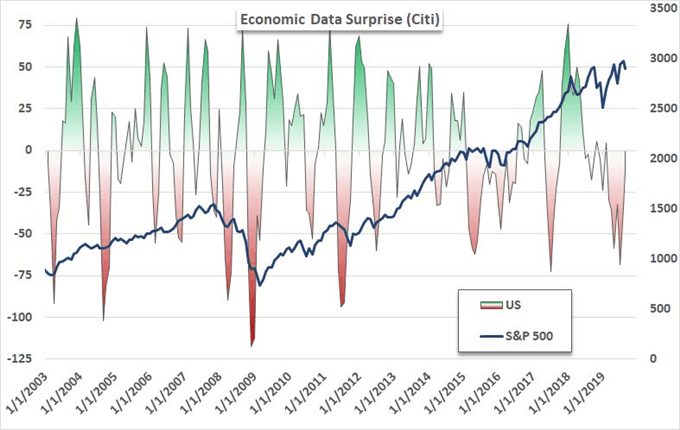

Chart of S&P 500 and Citi’s US Economic Surprise Index (Monthly)

This statement is even more concerning than its direct implications for the balance of priorities of the government. In the 'brief' recession scenario Trump evaluated, he suggested that a domestic two-month recession may be necessary to ensure the full exertion of pressure on China to change the behavior of the world's second largest economy. The technical definition of a recession according to the NBER is two consecutive *quarters* of economic contraction. If Trump meant two months, he is unlikely to appreciate what is at risk. If he meant two quarters, he is assuming an unrealistic amount of control over the economy. The march from growth to contraction in such a large economy - much less to the global performance - takes a very long time and incredible pressure to affect. Allowing the economy to stall is no small decision, but it is certainly being treated as such.

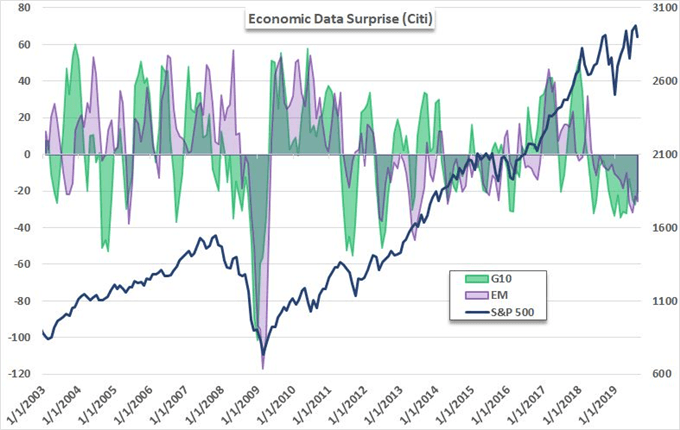

Chart of S&P 500 and Citi’s G10 and Emerging Market Economic Surprise Index (Monthly)

Anticipation Remains the Dominant Feature of the Market Landscape

As far as revelations of policy go, this past session's Trump remarks are even more pressing than the previous suggestion that 'trade wars are good and easy to win' - which signaled that the President absolutely intended to push ahead with his American-First agenda. And yet, despite the serious economic and financial implications, the market simply coasted. Sure, the S&P 500 and other risk-leaning assets eased off their Monday rally. Yet, the retracement was far from the chastening move we would expect with this stated position. Fundamentally-speaking there are few more ominous signals than what this represents. Yet, there is always the possibility that all these overwhelming circumstances can change course in the near future if the leaders of the world's largest central banks or its largest economies commit to an extreme preemptive action. It is very unlikely, but hope is a powerful drug - otherwise US equities would not be where they are today.

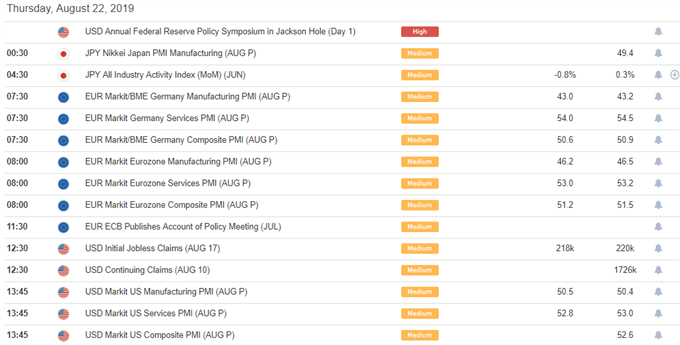

DailyFX Economic Calendar Key Thursday Events

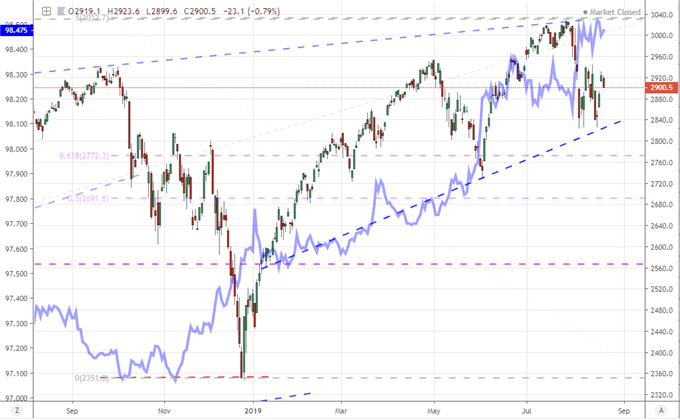

Trade Wars, Fed and Recession Fears Rotate to Cap S&P 500 and Dollar

There is an important cycle at work between fundamentals and speculation that will act to cap one of the world's favorite safe havens and its chief risk benchmarks. Trade wars represents the frontline of economic pressure on the global economy - one in which the United States and other countries seem intent to press as far as they deem their personal advantage continues to outweigh the global detriment. As the weight builds, the outlook for growth flags and markets begin to faulter. The threat of an economic contraction and collapse in equities forces the US and other governments to offer some measure of relief. For the Trump administration, the announcement that some small portion of the $300 billion in additional Chinese goods due to face 10 percent tariff on September 1st would be removed from the list while a more significant contingent would see the tax delayed to mid-December was very likely a move to resuscitate flagging markets. Yet, market participants perhaps realize that if the S&P 500 and its close counterparts were to return to record highs, the promise of support would evaporate.

The same automatic rebalancing is true for the influence of the Federal Reserve. While effectively holding back the tide from the President who is attempting to push the central bank to fast-track easing in order to support the transmission of the tariffs, the central bank cannot afford to ignore the panic and demands of the market. As such, if Trump pushes the trade wars and markets start to collapse under the fear of recession, the Fed will be prompted to respond with extreme measures (alongside an expected government response) that could in turn right the ship. Consequently, the central bank can put out a fire and preclude an extreme, dovish move. It is a potential balance between the compounding burden of trade wars and the unrealistic dependency put upon the world's largest central bank...until fear runs deeper than either group can hope to correct.

Chart of S&P 500 and Fed Fund Futures Contract for December 2019 (Daily)

Chart Created Using TradingView Platform

Dollar Has the FOMC, Euro Italian Politics and Pound the Ever-Present Brexit

With the responsive status of the Federal Reserve, the US Dollar will find an 'unnatural' cap to its ability to establish a clear trend - bullish or bearish. That doesn't mean we should tune out the top US event risk for the forthcoming session. The minutes from the July FOMC meeting are not a write off just because of the symposium later in the week. If you recall, the central bank cut rates for the first time in a decade last month and Chairman Powell's outlook was less than clear. There is certainly room in these transcript to charge speculation and potentially a short-term volatility response from the Greenback.

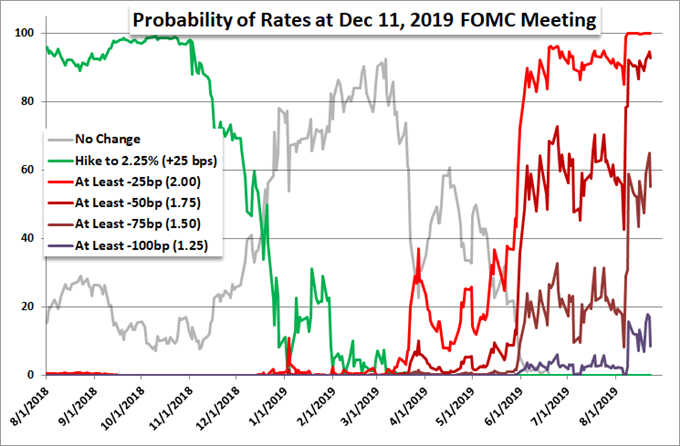

Probability of Fed Easing Through Year’s End

The Euro is facing a fundamental spark of its own. This past session, the League party led a no-confidence vote against Prime Minister Conte who in turn tendered his resignation. Despite the walk back by Santini and his party, the leader seems to be on his way out. That puts the status of Europe's third largest economy in serious uncertainty, especially with the budget - a source of serious contention with the EU - in doubt. Despite the inherent risk from this development, Italian yields barely budged. Regional risk assets were still performing well, perhaps because it translates into a higher probability that the ECB removes all the stops with stimulus. Yet, if that is the case, this would still be a collective burden to the Euro which bounced Tuesday.

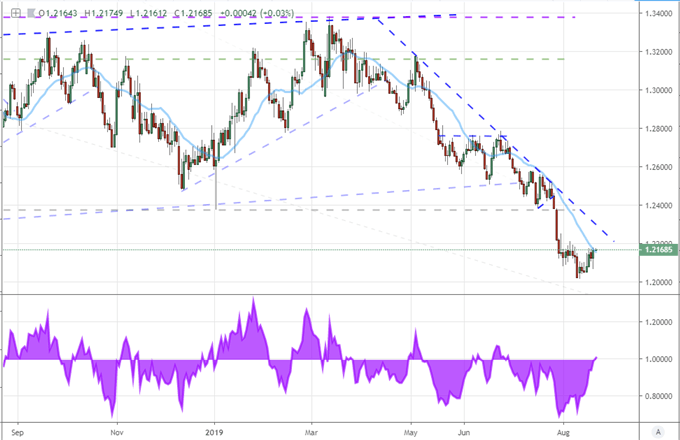

And, rounding out the top three fundamentally and technically-laden currencies, the Sterling is still absorbing the radiation from a no-deal Brexit anticipation. Prime Minister Johnson is still loudly pushing a clean break without agreement if the EU doesn't budge on the backstop. Yet, the EU has made clear it has no intention on reversing on a hard border in Ireland. This would seem an impasse that will create no small amount of chaos on October 31st but there are naturally rumors of back-channel negotiations that are drawing out the hopeful. GBPUSD, EURGBP and GBPJPY all look technically appealing, but all that potential is for not if the markets will not allow a run. We discuss all of this and more in today's Trading Video.

Chart of GBPUSD with 20-Day Moving Average and Differential (Daily)

Chart Created Using TradingView Platform

If you want to download my Manic-Crisis calendar, you can find the updated file here.

What fundamental themes should you follow next week? How will they impact the markets at large? Sign up for our webinars to better evaluate how market developments are shaping markets. Sign up on the Webinar Calendar.