Dollar Talking Points:

- Dollar posts an impressive rally despite earnings that decry Dollar strength, Powell warming to cuts and uneven data

- Pound and Euro register significant retreat despite fundamental references that have recently struggled to ump start price action

- US equities take a modest step lower from record highs while the rest of the risk-leaning assets remain placid

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Earnings Touch Upon Growth, Trade Wars and Monetary Policy Themes

We would touch upon all three major themes that we have kept regular watch over this past session through various headlines, officials' remarks and data points. However, I think it was particularly remarkable that trade wars, growth fears and monetary policy were all touched upon in US earnings. Starting with trade wars which had President Trump and Chinese media rhetoric to contend with, there was direct reference to the impact that this enormous source of uncertainty was bringing across a number of companies reporting. Perhaps more interesting was not the revenue guidance curtailed by poor relationships with the United States largest trade partners but rather more localized pressure. President Trump remarked this past session that he would advise his attorney general to look into Google's policies regarding China - a suggestion by one of his former technology council members, Peter Thiel, who also happens to have a stake in the industry. Putting the tension on US businesses is not unusual (Harley-Davidson, Amazon and GM among others).

The general health of the economy was readily reflected in earnings this past session as well. It is effectively the case that business sector earnings are a direct reflection of the overall health of an economy, but there were further particular performance figures that speak to the more overt fissures in expansion. Rail transportation firm CSX reported a miss on the quarter. When transportation of goods via rail, cargo shipping (like Maersk) or shipping solutions (such as Fedex) weaken; it can show fading expansion more tangibly then government data that is extrapolated by surveys with small sample size. Another interesting signal for the state of the economy through earnings was the Johnson & Johnson. While the consumer staple and medical devices maker beat top line, its sales weakened with a particular hit to foreign revenues for which it lamented the unfavorable exchange rate environment - something the US President may catch wind of.

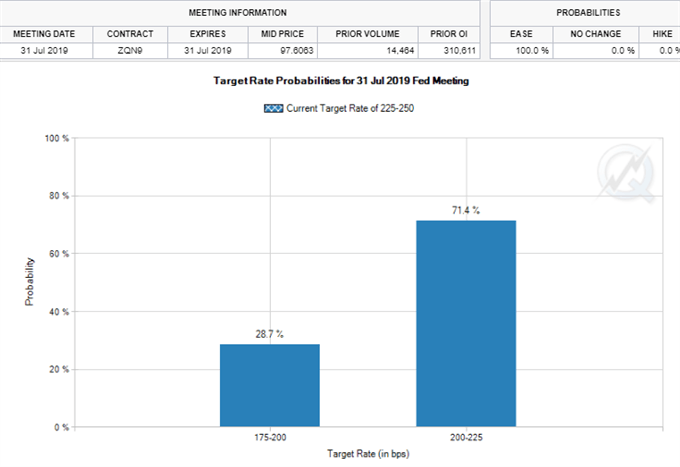

Perhaps the most comprehensive view of any of the systemic themes that we cover on a regular basis was the outlook for US monetary policy. There were three major banks that posted their previous quarter performance along with guidance for the future - JPMorgan, Wells Fargo and Goldman Sachs - and all three made either direct or related reference to an anticipated hit to profit from growing speculation of rate cuts by the Federal Reserve. JPM's CFO suggested that if there is one rate cut from the central bank this year, it could lead to income higher than $57.7 billion which would decline the deeper than cut through 2019. Not all companies benefit from an environment awash in liquidity.

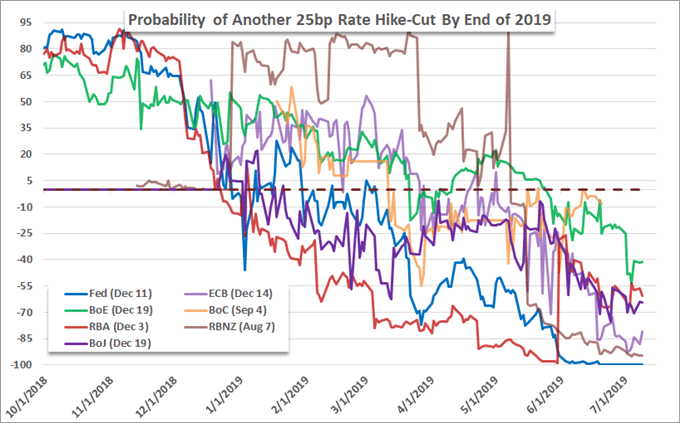

Probability of Fed Rate Cuts from CME Fed Fund Futures

An Abrupt Dollar Rally the Reflection of Themes, Event Risk or Just No Place Else to Go?

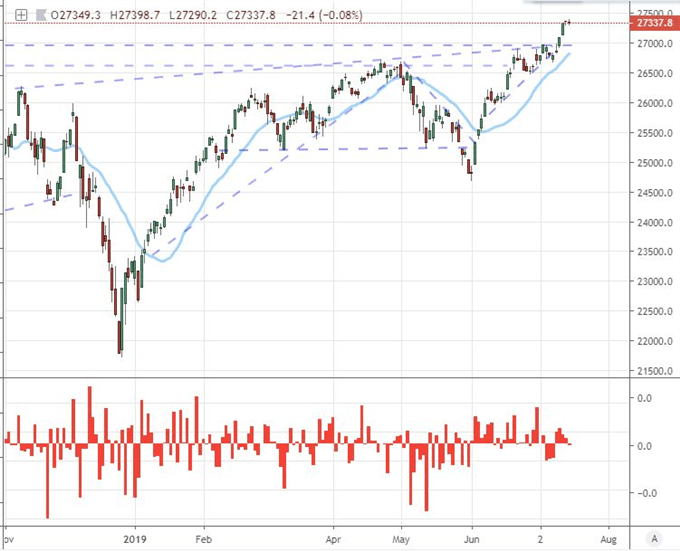

Looking for activity through the past session, there was a measured movement from the traditional risk-based assets. The Dow and S&P 500 look to once again be staging a more significant course reversal, but we have a ways to go before it reaches self-sustained collapse. So far, the Dow has posted its first gap lower in five trading days and offered some modest progress in a retreat after spinning its wheels through Monday. For most of the other risk-based assets, the buoyancy of the US indices are well out of reach.

Chart of the Dow Index and Opening Gaps (Daily)

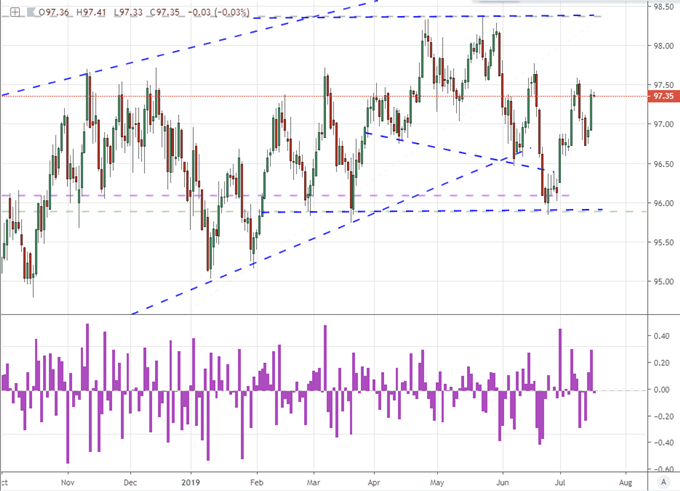

Far more impressive was the volatility from the top players in the FX ilk. The Dollar posted a hefty rally whether measured through trade-weighting (DXY) or on a more distributed basis. The Greenback's charge seemed to lack for consistency in its fundamental backing. Through Fed Chairman Powell's remarks, it was clear he was trying to commit forward guidance more explicitly to an impending rate cut while also suggesting the 'normal' of past cycles may not be reached again. In data, monthly retail sales rose 0.4 percent (versus 0.1 percent expected) while consumption excluding gasoline and autos offered a far more significant beat at 0.7 percent growth. That was on the favorable side of the scale. Alternative industrial production was unchanged, TIC flows expanded a scant $3.5 billion as China cut Treasury holdings a third month while export and import inflation dropped steadily. If the market is acting selectively, it could have still favored the bullish interpretation; but what we witnessed from the US currency may ultimately be the collective withdrawal from its major counterparts.

Chart of DXY Dollar Index and Rate of Change (Daily)

Unmistakable Weakness from the Euro and Pound

Looking for motivation for the Dollar, there are few stronger motivation than the simple equation of its most liquid counterparts succumbing to their own fundamental pressure. In addition to the Yen feeling a pinch through risk trends, the Euro dropped for a fourth consecutive session through Tuesday via an equally-weighted index. While the move lacks for unrestricted momentum, it is still a consistent drive. Behind its troubles, there is data in the form of investor sentiment which dropped the Eurozone as a whole (-20.3) and chief member Germany (-24.5 expectations and current measure flipping negative). In more systemic interests, Germany's Ursula von der Leyen was approved by the EU Parliament to head the Union, but there was a clearly divided backdrop.

Chart of Equally-Weighted Euro Index and Consecutive Candles (Daily)

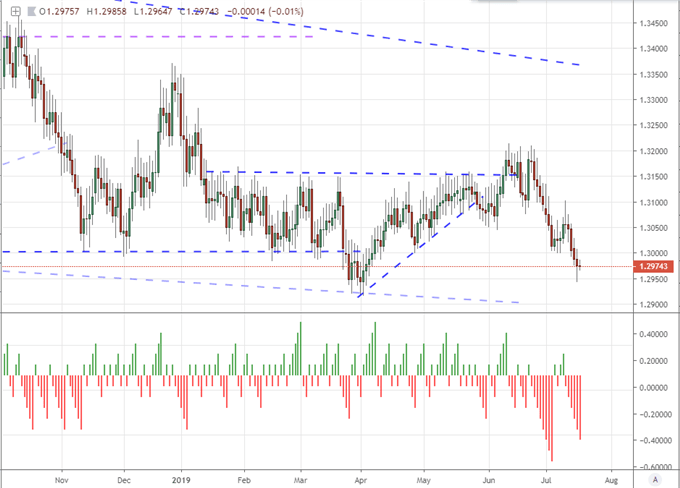

While significantly less liquid than the Euro - and thereby a less pressing lever for the Dollar - the British Pound's tumble was far more aggressive and incredibly productive. The Sterling dropped its lowest level since November 2016 while GBPUSD suffered its worst single-day performance since March 28th. UK jobless claims were a meaningful economic update with a notably poor benchmark update (38,000), but robust wage growth would seem to counter the pain. As important as this economic figure may be, it likely carries limited impact for the Sterling - and the same is true of the UK's inflation figures ahead. The unrelenting concern remains fears of a disorderly Brexit, but what insight is building this particular risk before a conservative party leader is decided and then we eventually return to a divorce fight with the European Union. At what point is a disorderly exit fully priced?

Chart of Equally-Weighted Pound Index

Kiwi Dollar Fails to Leverage a Data Move, Now It's the Canadian Dollar's Turn

For less reliable, systemic moves than the Dollar, Euro or Pound; we have to look to scheduled event risk with enough bite to hit upon a more headline-worthy theme. The New Zealand Dollar Tuesday morning had the chance to change its cards with rate speculation as 2Q CPI crossed the wires. While the clip of price pressures accelerated modestly (1.7 from 1.5 percent), it was in-line with forecasts and still well short of the RBNZ's tolerance band. It is no wonder the Kiwi wouldn't mount a substantial rally on the data release.

Chart of Rate Probabilities for the Major Central Banks

Perhaps the circumstances for the Canadian Dollar will be different moving forward. The currency has enjoyed an impressive climb these past weeks as the threat an ongoing US trade war and speculation of a BOC policy shift akin to that of the Fed have both faded into the backdrop. While dovish pressure is slowly building, the Canadian central bank is still lagging far behind for monetary policy action relative to the likes of the Fed, ECB and BOJ. That could change with the upcoming sessions Canadian CPI data. Headline inflation is setting the bar very low for generating a surprise response with a forecast of 1.8 percent that mirrors the previous month's clip. Technicals would better perform if the insight is dovish, but don't let expectations get too far ahead of practical market developments. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.