US DOLLAR FORECAST, US-CHINA TRADE WAR – TALKING POINTS:

- US-China trade war tensions are continuously climbing. Where might this escalation lead?

- Beijing prepared to use rare earth minerals, bureaucratic tools as leverage in trade talks

- Will China push the proverbial “nuclear button”, dumping its US Treasuries portfolio?

See our free guide to learn how to use economic news in your trading strategy !

WHERE IS THE US-CHINA TRADE WAR HEADED?

The US-China trade war is a fundamental headwind that is continuing to blow the sails of the global economy increasingly closer to a rocky coastline. The IMF, WTO and other notable institutions have cited the conflict as the primary culprit behind deteriorating global growth prospects. Analysts have also highlighted the risk that weakening economic conditions could expose hidden weaknesses in the financial system.

At the time of writing, officials in Beijing and Washington have dug their heels into the ground and threatened to escalate the situation. The most recent incident came when US President Donald Trump imposed an additional 15 percent tariff on $200 billion worth of Chinese goods in response to China’s alleged back-pedaling on key issues in the prospective trade agreement.

This was followed by a threat to impose an additional 25 percent tariff on $300 billion worth of Chinese goods unless Beijing was brought to heel. Some of these demands curbing its development of state-owned enterprises (SOEs), which Washington accused of giving local companies an unfair advantage. China responded that it sees such a demand as an “invasion” of its sovereignty.

Want to learn more about the history of trade wars? See our interactive infographic here!

PRC officials have reiterated that they will not swallow any “bitter fruit” and compromise on what they believe could undermine core interests. Starting in June – in response to US tariffs – Beijing imposed a levy of $60 billion against US-imported goods. As both sides double down, China has begun to explore alternative ways of retribution, with one measure being so extreme it has been dubbed the “nuclear option”.

This would be to sell its $1.1 trillion holding of US Treasuries. More on that later. How else, then, may China use any of the non-military weapons in its arsenal to gain an advantage in trade negotiations with Washington?

CHINA MAY RESTRICT ACCESS TO RARE EARTH MINERALS

There are many steps before Beijing would even consider a radical move like selling most or all of its Treasuries portfolio, including banning or at least strongly restricting the supply of rare earth mineral exports to the US. Speculation about such a policy began when Chinese President Xi Jinping demonstratively visited a local rare earth processing facility.

Despite the name, China might use these “rare” earth minerals as leverage not because of their scarcity, but rather because it dominates their processing. Here the world’s number-two economy wields an unparalleled advantage. The facilities doing this work operate at a high financial and environmental cost, which has been decisive in keeping competitors at bay.

In the US, especially given the political atmosphere of reducing pollution and being more environmentally conscious, attempting to ramp up production would be a long and costly process.

HOW WOULD RESTRICTED SUPPLY OF RARE EARTH MINERALS IMPACT FINANCIAL MARKETS?

China accounts for 80 percent of US rare earth mineral imports, 17 of which are heavily used in high-tech consumer electronics and military hardware. Some other applications include batteries, catalysts in cars and wind turbines. It has an advantage because most of the technology that the US already uses has these rare earth minerals embedded in it, most notably in computers and cellphones.

Apple Inc uses many of these materials to enable the use of key features in its cellphone products, which if restricted could dramatically disrupt production and hurt earnings. As one of the largest companies in the world with a market cap of almost 800 billion, significant price moves in Apple stock could reverberate across global financial markets and sour sentiment.

Cycle-sensitive assets such as equities as well as the New Zealand and Australian Dollars would likely sink while the ant-risk Japanese Yen and US Dollar along with Treasury bonds would likely catch a haven bid. The S&P 500 in particular might suffer because of Apple’s significant weight in the index, making the company a frequently-cited bellwether for market sentiment.

WRAPPED IN RED: HOW CHINA MAY USE BUREAUCRACY AS LEVERAGE IN TRADE TALKS

In addition to using mother nature, China can also harness the vast power of the bureaucratic state to wrap US businesses in red tape. In a recent US-China Business Council survey, 25 percent of firms reported increased scrutiny by regulators and greater barriers to entering the Chinese market. These include increased frequency of unannounced inspections and slower clearance for customs among many other obstacles.

While the Chinese government has not explicitly stated that they directly ordered the implementation of these bureaucratic hurdles, the timing is considered suspicious among analysts and market participants. Businesses have found themselves encountering more bureaucratic roadblocks almost exactly as US-China trade relations began to severely sour in May.

A breakthrough in trade negotiations may miraculously result in customs and various checks disappearing and could speed up the process of regulatory clearance. However, until this occurs, it is not likely that firms will find it any easier to enter and participate in the Chinese market, leading to greater speculation that US economic performance will take a hit.

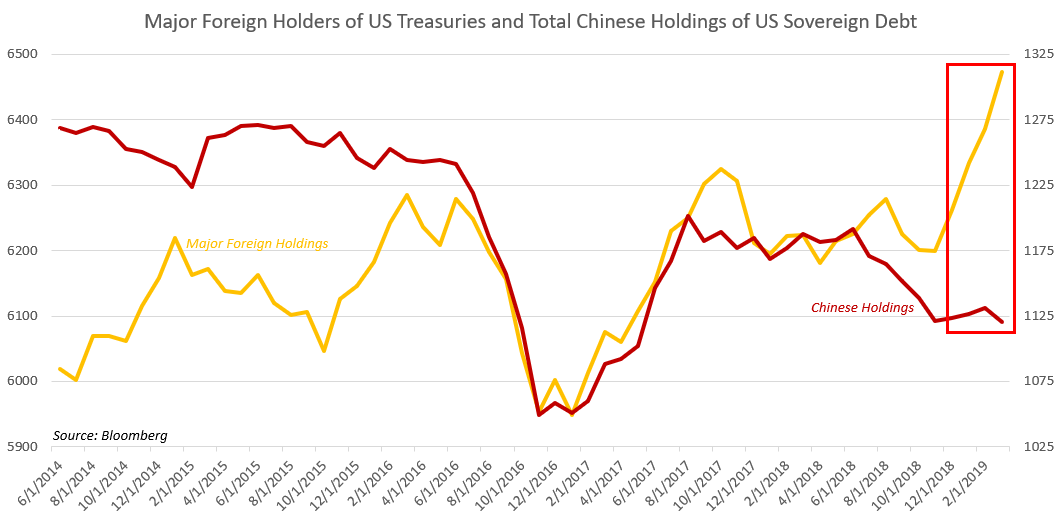

THE NUCLEAR OPTION: WILL CHINA DUMP ITS TREASURY HOLDINGS?

The short answer is “probably no”. However, to discount the unthinkable in inconceivable times would be as unthinkable as it is unconceivable. China is the largest foreign holder of US debt, owning approximately $1.1 trillion in Treasuries. Since Beijing has accrued such a large stockpile of US government bonds, market participants have worried about what might happen if China were to rapidly divest its portfolio.

Chinese officials have not exercised this option because the global impact would almost inevitably reverberate back to Asia and undermine China’s own growth prospects and financial stability. However, if the US continues its aggressive approach to trade talks, it may back Beijing into a corner, leading to a greater probability that it will flex this muscle as a warning sign. To a certain degree, it already has.

In March, China sold $20 billion worth of US Treasuries, the largest selloff in close to two years. Global financial markets were spooked on just the prospect that China would consider even using such a controversial weapon as a scare tactic. What would be the short, medium and long-term consequences if China dumped all its US Treasury holdings?

The short-term reaction would almost certainly be market panic. The US Dollar along with sentiment-linked currencies like the Australian and New Zealand Dollars would likely drop alongside equities and growth-geared commodities. The sudden influx of US Treasuries would depress bond prices and cause a dramatic spike in yields (since the two typically move inversely to each other), leading to a surge in borrowing costs for the US government.

Yields on Treasuries are where almost all other borrowing costs are benchmarked. These include business and consumer credit, corporate bonds, mortgages etc. The higher yield on US bonds would thus lift rates on a slew of interest-bearing debts, making them more expensive to service and reducing the overall rate of borrowing. A slowdown in investment and economic growth would follow, leaving the central bank to clean up the mess.

However, it is not as if China would emerge unscathed in this scenario. Approximately 20 percent of Chinese exports head to the US, making it the country’s largest customer. If demand there plummets, China’s growth would be hurt as well. Furthermore, the destabilizing effect would impair risk sentiment by way of the shockwave it would send throughout developed and emerging market economies.

The cost of commodities – which are primarily priced in US Dollars – would soar due to a weaker Greenback. As a major importer of raw materials, China would see its cost structure skyrocket. This would undermine China’s own economic prospects and may cause diplomatic relations with key allies to suffer.

A weaker US Dollar might alleviate sovereign borrowers that have their debt denominated in USD. However, the benefits to be had from this relative to the costs incurred by global markets would be almost inconsequential. In the US, purchasing power would be radically reduced, limiting domestic consumption – the driver of growth – in the largest economy in the world.

HOW MIGHT THE FED BE ABLE TO ALLEVIATE THE CRISIS?

The Fed could cut rates, though by this point they may be limited in their ability to do so. This might weigh on the Dollar to some extent, though by this stage in the trade war it is likely to be under severe strain already. The result could then be a form of stagnation where inflation and unemployment both remain high – much like the oil shock crisis in 1979. In this environment, the central bank will probably struggle to craft effective policy that doesn’t undermine its own objectives at least to some extent.

The longer-term consequence of large-scale Chinese divestment from Treasuries is that it would undermine confidence in the US Dollar and provide policymakers with the impetus to find an alternative reserve currency. The probability that Beijing will pull such a maneuver seems low because it would essentially be pulling the rug from under itself by destabilizing the largest economy in the world and a key trading partner, undermining its own performance.

In this regard, the decision by China to dump all its holdings of US Treasuries would be both its honey and hemlock. The sweet taste of exerting such power would be swiftly replaced by the poison of the blowback. To that end, it seems Chinese officials might do well to take a page from Confucius: “Before you embark on a journey of revenge, dig two graves”.

FX TRADING RESOURCES

- Join a free webinar and have your trading questions answered

- Just getting started? See our beginners’ guide for FX traders

- Having trouble with your strategy? Here’s the #1 mistake that traders make

--- Written by Dimitri Zabelin, Jr Currency Analyst for DailyFX.com

To contact Dimitri, use the comments section below or @ZabelinDimitri on Twitter