Talking Points:

- Risk trends flagged materially this past session with a third consecutive gap higher for SPX earning less progress and range

- The ECB rate decision - top event risk Thursday - confirmed the expected end to QE without fulfilling fears of later first hike

- Crude oil finally posted a meaningful rally and even earned a technical break, but consider liqudity for intent

What makes for a 'great' trader? Strategy is important but there are many ways we can analyze to good trades. The most important limitations and advances are found in our own psychology. Download the DailyFX Building Confidence in Trading and Traits of Successful Traders guides to learn how to set your course from the beginning.

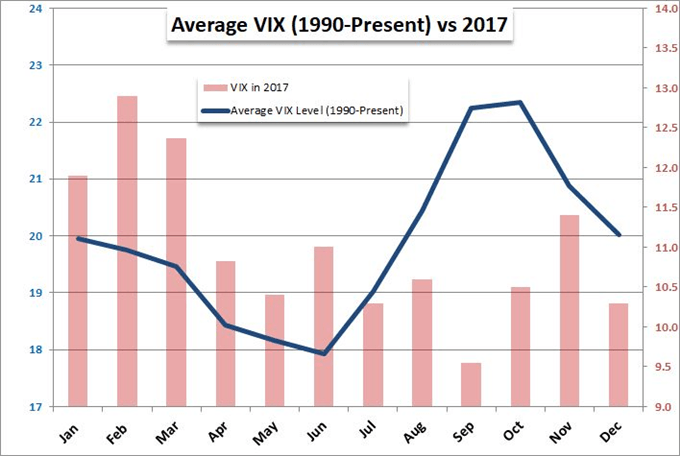

Is Market Volatility Finally Slipping Into the Seasonal Tide?

There remains a conflict between what we have come to expect from the markets after months of speculative escalation and the warm embrace of a seasonality-based deflation born of an undisputable drop in liquidity. Thus far, we have seen the glare of volatility remain despite the usual slide in activity as key event risk thins out such that systemic themes grow further and further out of reach of the newswires. However, with the European Central Bank (ECB) rate decision playing out yesterday without the dramatic fanfare that could have been, the road to 2019 has notably cleared up. There are still a select few high-profile events on tap through year's end and a host of unresolved fundamental themes lurking in the system, but the likelihood that circumstances for these events will hit the proper pitch to resonate with the thinned speculative rank is increasingly small. It seems this self-awareness is starting to sink in with the market if implied volatility readings are to be believed. While the equity-based VIX and short-term VXX indices remain remarkably buoyant; there has been a slide in activity readings for yields, commodities and FX markets. If this represents a reliable reversion to seasonal norms, the picture of the S&P 500 holding at its 2018 support despite large wicks and high ATR (average true range) readings looks more like the reliable signal that we have seen in previous years.

Historical Averages of VIX Volatility Index by Month

The ECB Calls to an End its Massive Stimulus Program

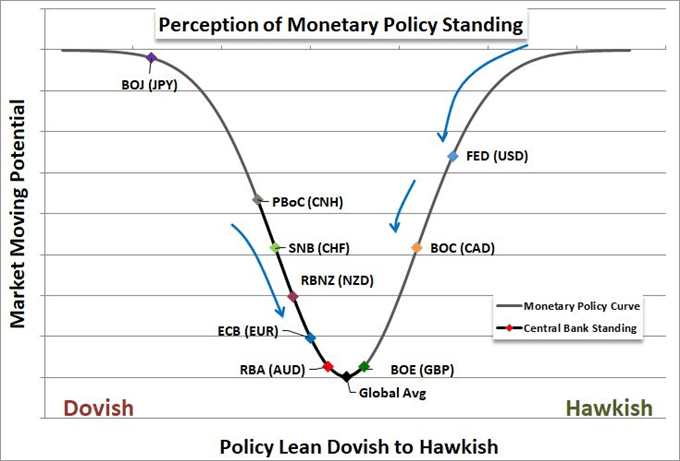

Through the past session, we cleared the last great fundamental hurdle for the week. The ECB rate decision managed signal an important change in its course of policy without sending shockwaves through the system. While they didn't touch their exaggerated benchmark rates (including the negative deposit rate), President Draghi announced the end of the extraordinary stimulus program. After more than three-and-a-half years of Quantitative Easing (QE), the bank pumped over 2.6 trillion euros worth of liquidity into the system. It is difficult to argue that this bolstered growth, employment or inflation; but it certainly did deflate the Euro and perhaps local capital market benchmarks. This move pulls the world’s second largest central bank from the explicitly 'bearish' end of the monetary spectrum but it is not an automatic swing to the opposite end of the spectrum. Like the Fed between 2014 and 2017, the ECB will continue to reinvest proceeds from the program to keep their balance sheet unchanged and of course rates will stay at their record low level. What traders were really looking for to signal the Euro one way or the other was any language to suggest that the first hike would happen in late 2019 or into 2020. There was nothing said or projected that seemed to clarify that for the speculative rank, and thereby the Euro was left without the ignition EURUSD was looking for. It is still possible that this benchmark pair triggers the inverse head-and-shoulders pattern or charges to revive the medium-term bear trend, but it would be exceptionally difficult to spin into a lasting move everything considered.

Monetary Policy Spectrum of Major Central Banks

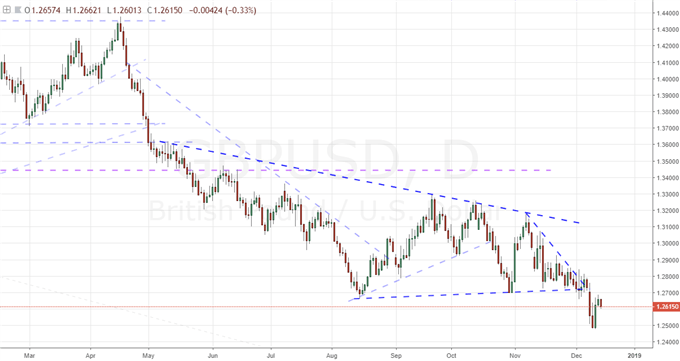

More Anticipation than Motivation for Pound and Dollar

Where the Euro is somewhat disappointing for its lack of fundamental enthusiasm from a key event, two of its most liquid counterparts retain much the same appetite without the convenience of high profile catalysts. The Pound is still directly tuned into the Brexit proceedings and there is still a wide range of outcomes from this dispute between the UK and EU with a large clock in the background. Prime Minister Theresa Mays' no-confidence vote dodge earlier this week has already lost its inherent lift through the standard relief rally. There simply wasn't enough of a discount on the alternative outcome and the market is not sure that her remaining at the helm changes the range of outcomes that the country faces. May suggested through her spokesperson that no vote on Brexit is likely in Parliament before Christmas, so volatility in Sterling before then would be more self-indulgent. As for the US Dollar, there is plenty of systemic anticipation in place between trade wars, growth, credit quality and more. However, attention seems to be heading into a familiar vortex in the form of next week's FOMC rate decision. Though it comes the week before an absolute liquidity crunch, it will be a critical update for US policy owing to an anticipated plateau in the tightening cycle being plotted out in the forward guidance. This has implications for risk trends as well as the Greenback, but we won't know how far that can stretch until the details are announced on Wednesday.

Chart of GBPUSD (Daily)

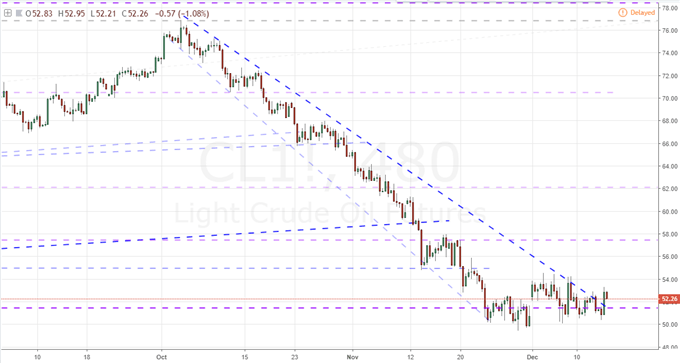

Crude Oil Attempts to Draw Out Speculators with a Break

While key trends and technical levels seem to be losing their luster across a range of benchmark asset leaders, there are still some interesting technical pictures. If indeed the market is going to slip into its tradition of reversion to the mean - a jargon term for ranges that perhaps are less precise at technical borders - there are certain areas this may be exploited. For the Swiss Franc, the Swiss National Bank (SNB) rate decision reminds us that this group is stuck for the long haul which can set the CHF course a little more reliably. If so many other major central banks were backing off their hawkish lean (Fed, BOE, BOC), then this could position the currency in a clearly bearish position. Yet, that isn't the context we have. The Kiwi is another currency that is interesting for reversion after its strong, one-way rally in defiance of unfavorable fundamentals; seeing speculative pullback could send this currency to correction. With this market backdrop in mind, however, there are perhaps no more remarkable a speculative interest in the trading rank than with US crude oil. The commodity tumbled over 30 percent in the span of little more than 6 weeks to put itself into at least a short-term speculative, oversold position. After a few weeks of consolidation, we registered a strong rally this past session to produce what could be considered a noteworthy break. What kind of intent does this development have? I would not set my expectations high - and we only need to look to natural gas to see why. We discuss all of this and more in today's Trading Video.

Chart of Crude Oil (8 Hour)

If you want to download my Manic-Crisis calendar, you can find the updated file here.