Turkish Lira Outlook:

- Aggressive intervention efforts last week saw the Turkish Lira gain +50% in a matter of days. However, the Lira still remains down over -40% year-to-date.

- Turkey has burned through its foreign assets to prop up the Lira, and the new policy to reimburse domestic savers may only weaken the government’s fiscal position.

- The Turkish Lira crisis is far from over, and may soon get worse once again.

Lira Remains in Crisis

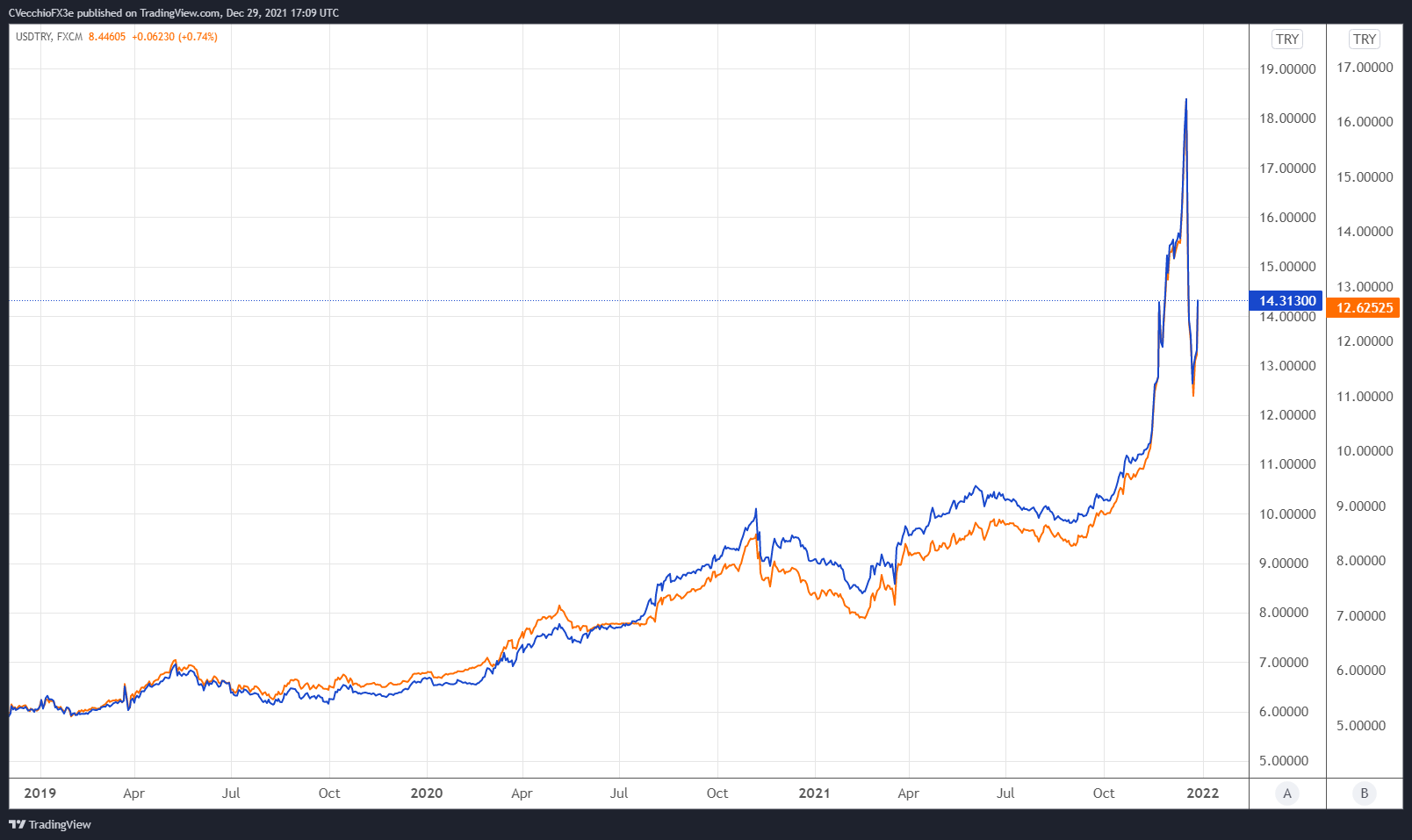

We’ve been periodically checking in on the Turkish Lira since the end of September, as the emerging market currency remains in the throes of a textbook currency crisis. In what appears to be a misguided attempt to prop up the Lira, the Turkish government intervened dramatically in currency markets, helping propel the Lira higher by over +50% last week.

The cost, however, was significant: Turkey burned through their remaining foreign assets in order to prop up the Lira. According to Bloomberg News, “net foreign assets dropped to minus $5.1 billion on Tuesday [December 22] compared with $817 million on Friday [December 17].”

For all that ammunition spent, the gains are relatively paltry: the Lira is still down by approximately -40% year-to-date versus the Euro and the US Dollar. While the intervention effort has seen the Turkish Lira return back to levels last witnessed in late-November, by no means is the currency crisis over.

The Turkish government’s new policy of reimbursing domestic savers on Lira declines is an attempt to stave off demand for foreign currencies like the Euro and the US Dollar. In order to compensate for losses, the Central Bank of the Republic of Turkey will have to print more currency – which can exacerbate the ongoing inflation issue, one that can’t be solved with Turkish President Recep Tayyip Erdoğan’s misguided obsession with low interest rates.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

EUR/TRY [BLUE] & USD/TRY [ORANGE] TECHNICAL ANALYSIS: DAILY PRICE CHART (December 2018 to December2021) (CHART 1)

It remains the case that the factors are in place for the currency crisis to worsen yet again, per the Emerging Markets Crisis Monitor: record inflation (and record low real yields), a negative current account, rising implied FX volatility, widening bond risk premiums, and a rising external debt burden are hallmarks of an emerging market currency in crisis.

--- Written by Christopher Vecchio, CFA, Senior Strategist