.jpg)

Talking Points:

- This can be a challenging weekend for holding weekend risk given the ongoing and still developing scenario around Evergrande.

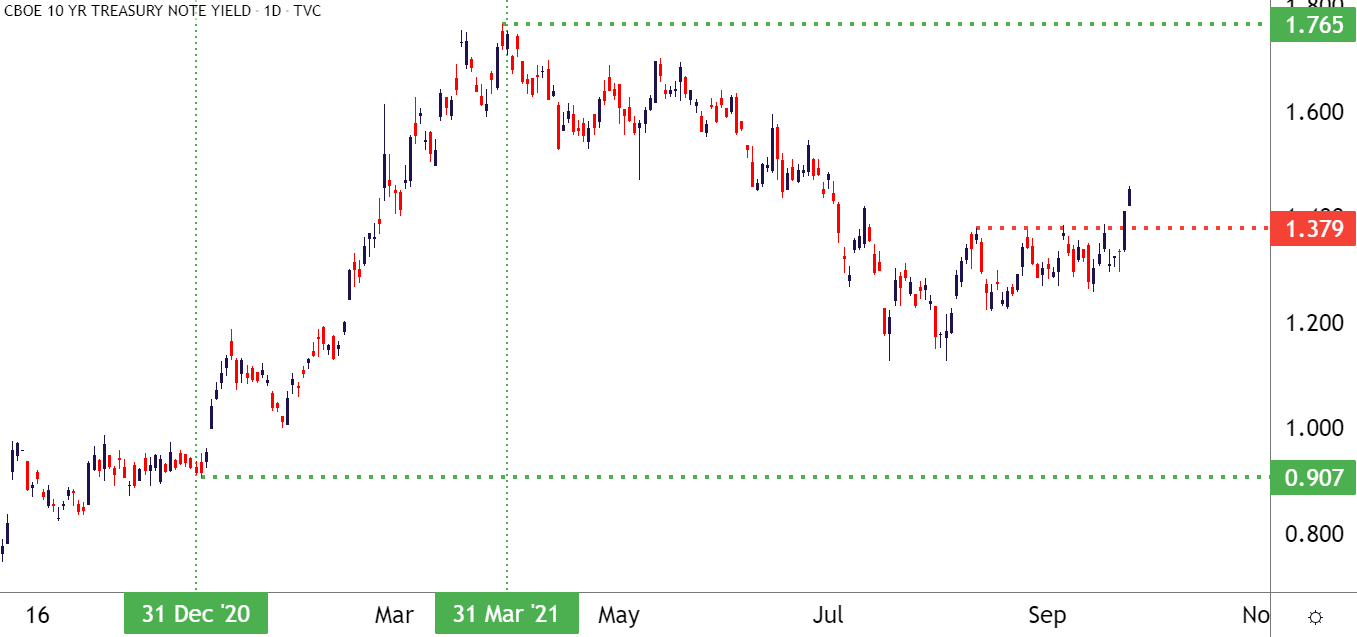

- The move in rates after this week’s FOMC has continued and the 10 year yield has pushed up to a fresh two-month-high.

- Next week marks the Q4 open on Friday, but notably there will be no NFP report on October 1st as that’s scheduled for a week later instead. The big driver on next week’s economic calendar our of the US is a batch of high-impact prints on Friday with PCE and PMI reports.

It was a big week in markets and, frankly, I think there has to be a lot of optimism with the way that price action has held up given all of the facts. While the week opened with pain as stocks gapped-down aggressively, a bit of hope punctuated the horizon as prices caught a bid around FOMC and continued to run higher on Thursday trade. So far on Friday we’re seeing a resistance hold but, deductively, this appears to be fairly positive.

The big driver this week was, of course, the Federal Reserve. The world was waiting for an announcement of taper that did not happen: Instead, the Central Bank warned that they were close to starting taper and it could happen in the next couple of months if labor market data didn’t disappoint. But, perhaps more surprising than a lack of a taper announcement is what showed up in the dot plot matrix, as the median forecast at the Fed now calls for a rate hike in 2022 whereas previously the expectation was for that first hike to take place in 2023.

In response rates markets have continued to run, yields on the 10 year Treasury are now trading at fresh two-month highs with a very strong thrust over the past couple of trading days.

A more hawkish central bank could provide some pressure to stock prices, at some point; and for specific rotation, this could add more pressure to the tech-heavy and rate sensitive Nasdaq 100 versus the blue chip S&P 500 as we move into Q4 next week.

US Treasury 10 Year Note Yield: Fresh Two Month Highs

Chart prepared by James Stanley; TNX on Tradingview

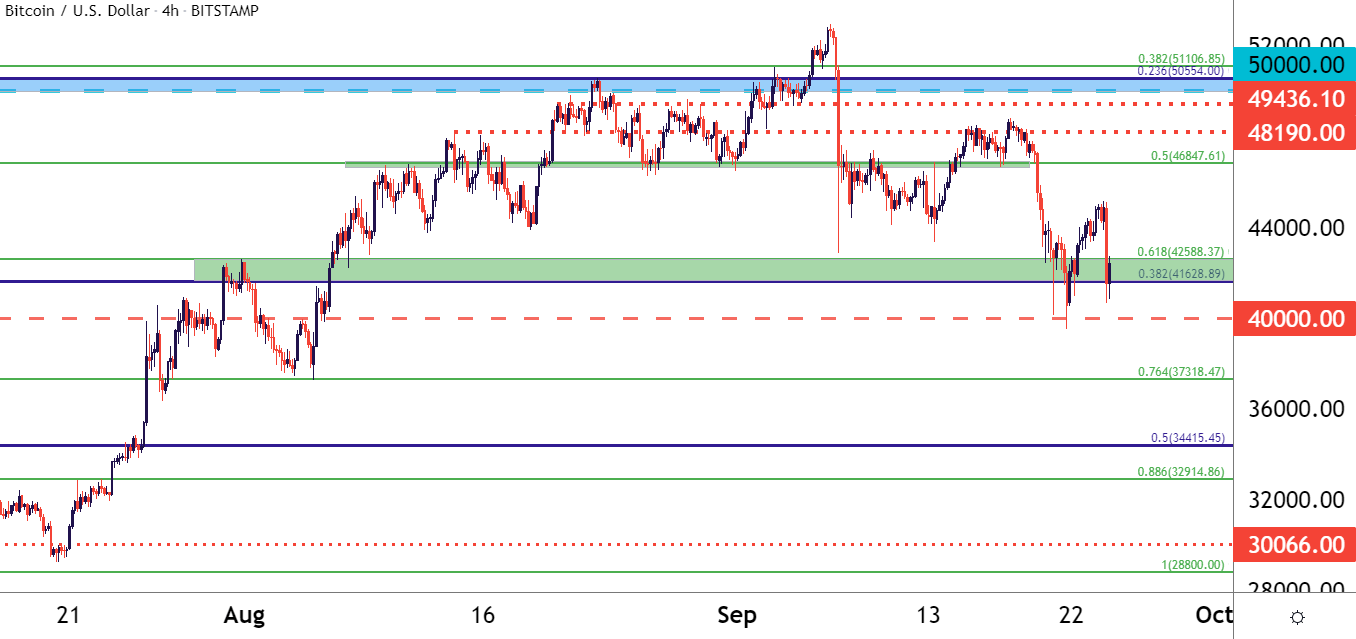

China Bans Crypto

You’ve probably already read that headline once or twice before. But China took their anti-crypto stance a step further today when they announced that all cryptocurrency transactions are now considered illegal.

While the headline is sweeping and attention grabbing, the price action has been far less so as this has merely amounted to a check-back to support at this point. Bitcoin is finding support in the same 41,628-42,588 zone looked at earlier this week, respecting the prior low that was set around the 40k psychological level.

To learn more about psychological levels or Fibonacci, check out DailyFX Education

Bitcoin Four-Hour Price Chart

Chart prepared by James Stanley; Bitcoin on Tradingview

Evergrande Weekend Risk

This could be a difficult weekend for holding open risk, as the past Monday’s open reminded, weekend events around the ongoing Evergrande saga could create a sharp re-pricing for when markets open on Monday.

While the risk appears less threatening at this point after a number of banks have come out to say that they’re minimally exposed to the risk, a 500 billion dollar bankruptcy could create massive ripple effects. There’s a number of counterparties to be considered and these relationships likely span the globe, it seems remiss to completely discount the risk of a larger Evergrande bankruptcy, if it happens.

In the news this week was an interest payment that was missed on Thursday. This doesn’t necessarily spell a default as Evergrande has 30 days to make the payment without it being considered a technical default.

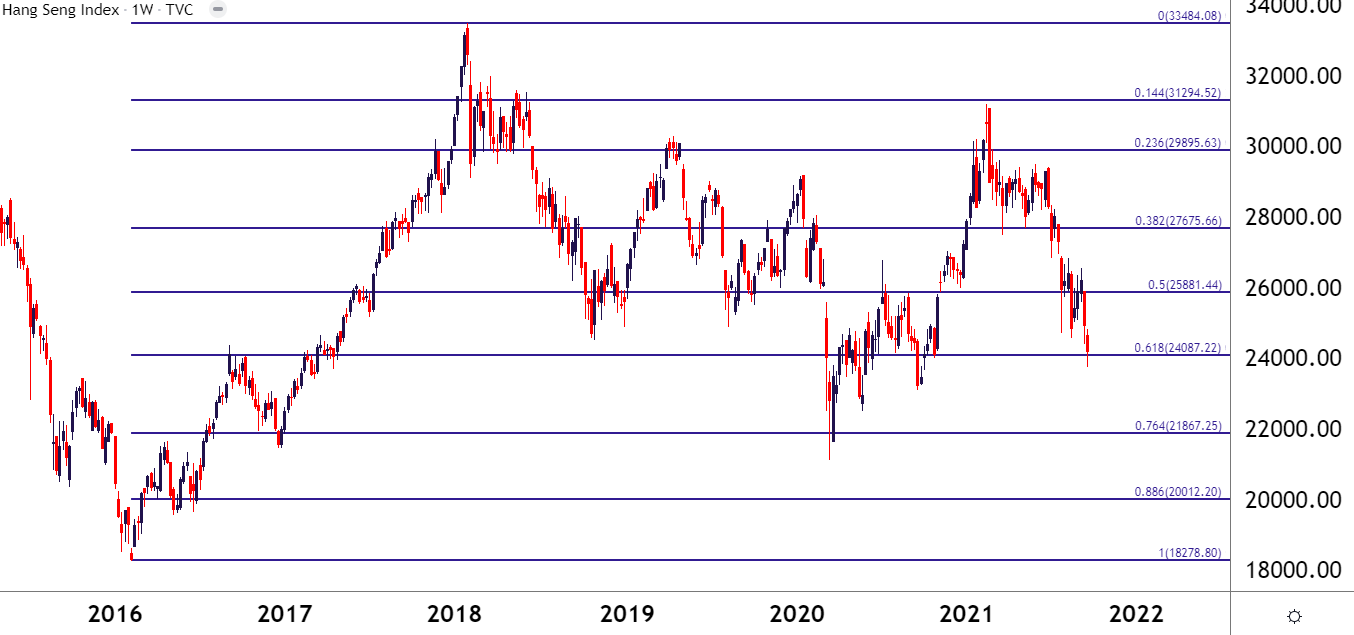

But, perhaps more importantly is the stance from China as we’ve already seen a number of changes in the way that country is handling the problem. It appears that a bail out isn’t a nearby option which furthers that question of ripple effects and what it might mean for markets outside of the mainland. For focal points, stocks in Hong Kong appear to be holding in a tough spot after setting a fresh 2021 low earlier this week. Price action is holding on the 61.8% retracement of the 2016-2018 major move.

Hang Seng Weekly Price Chart

Chart prepared by James Stanley; Hang Seng on Tradingview

--- Written by James Stanley, Senior Strategist for DailyFX.com

Contact and follow James on Twitter: @JStanleyFX