Talking Point:

- Today marks the one-year anniversary of our Market Talk article/newsletters, and to mark the occasion we’re revisiting the theme that kicked it all off with China and the Yuan. To sign up for my distribution list, please click here to sign up. .

- While weakness in the Yuan carried large macro-implications in August and January, eliciting major global market sell-offs, more recently the Yuan has weakened with little corresponding response. But this doesn’t mean that this risk is ‘over’ yet, as the Chinese economy continues to face slowdown.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

In what’s appearing to be a quiet day across markets in the midst of a light week of data, price action has remained relatively subdued across much of the FX-space after the outsized moves of last week. As we wrote yesterday, the predominant trends being seen in the US Dollar, Japanese Yen and Gold could be due for some element of consolidation after the big moves in the week earlier. And if we combine a light economic calendar in the latter portion of the summer with the start of the Summer Olympics, we have a recipe for light volume-markets until we get to the Jackson Hole Summit at the end of the month (August 25-27).

But traders would be well-served to not get caught flat-footed here, as there is still the potential for considerable risk in the global economy. And given that lighter volume is being seen at the present, any potential flares of risk could become magnified as lower levels of liquidity in a market could amount to higher levels of volatility.

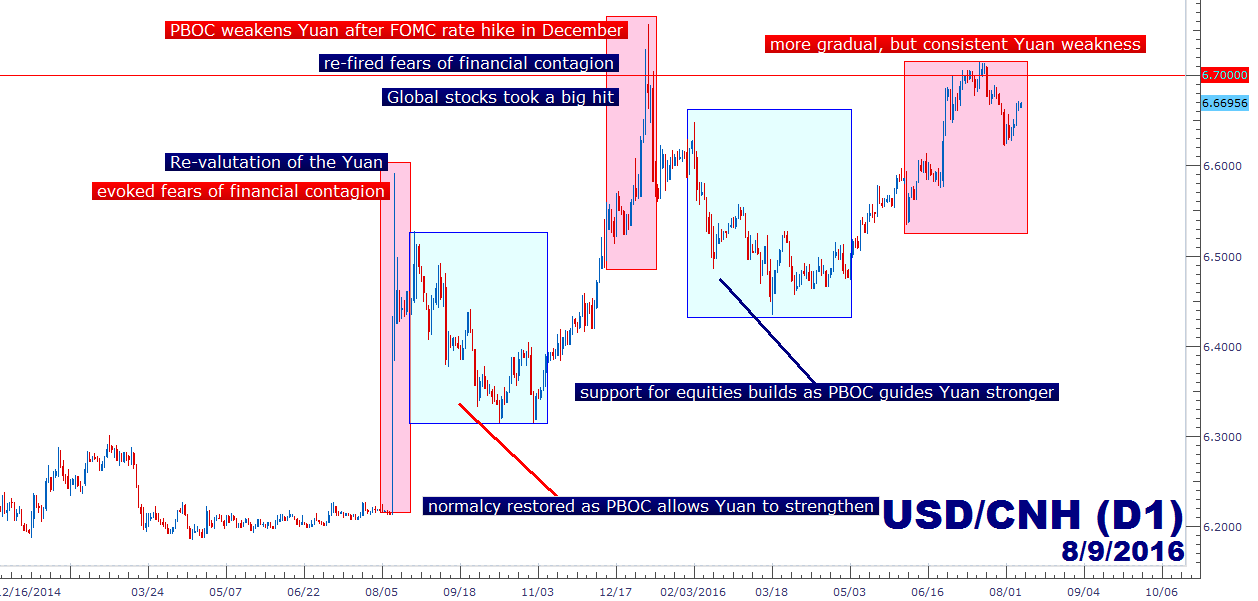

One of those potential risk factors is a risk that’s been somewhat under-the-surface of recent as U.S. rate hike expectations and Brexit have stolen the headlines throughout the summer, and that’s the continued struggle of the Chinese economy . It was almost one year ago that China re-valuated the Yuan to a basket of currencies as opposed to the former direct-peg with the U.S. Dollar. This created a rush of Yuan-weakness against the Greenback, and this fired fears of a Chinese slowdown permeating through the global economy as fresh capital could flow out of China on the back of this newfound-weakness. If capital is flowing out of China, it needs a home, and this meant the prospect of unwanted. Within a couple of weeks, those fears had hit global equity markets on the back of China’s ‘Black Monday.’

But those fears abated as the Chinese Yuan strengthened in the weeks following, only to flare up again at the start of 2016 as the Yuan put in another spike of weakness, re-firing fears of a ‘contagion’ effect hitting the global economy on the back of a slowdown in China, led by Yuan-weakness.

Created with Marketscope/Trading Station II; prepared by James Stanley

So, as the Yuan had spiked-weaker in the past, global stocks took an outsized hit as fears of ‘contagion’ spread throughout the global economy. But more recently, the PBOC has been gradually guiding the Yuan weaker to levels that have previously evoked crisis-like responses at the psychological 6.7000 level. The fact that there hasn’t yet been a corresponding move in equities is the part may be a bit disconcerting.

How Does Yuan Weakness Hit the Rest of the World?

Trade and capital flows. If the Yuan is weakening, we’re likely seeing Chinese investors attempting to sell out of their Yuan in favor of currencies that might not weaken as much. For capital to leave the Yuan, it needs a place to go; such as US Dollars or Japanese Yen. This brings strength into those currencies at a time when few economies can afford it. Sure, the benefits of investment capital have generally been positive in the past, but in a low-rate/ZIRP-like environment, there is no lack of investment capital, and more of a lack of investment opportunities. So capital flows coming out of China on the back of a weak-Yuan could be an extremely threatening thing, especially for the chief Chinese trade partners of the U.S. and Japan. This is one of the reasons we called the Yen the ‘safe haven vehicle of choice’ back in September of last year, because despite the Central Bank policies that have been engineered to evoke currency weakness, an onslaught of Chinese capital seeking safer harbors could more than erase all of that ‘work.’ This exacerbates Central Bankers’ problems, and it erases one of the few tools that they have left in their ‘arsenal.’

Why is Yuan Weakness So Widely Expected?

Because of debt, and like much of the rest of the world China is carrying far too much. The issue gets a bit more complex from here given the importance of Chinese SOE’s or, State-Owned Enterprises, which are quasi-public/private companies competing directly with the private sector. These are companies that have traditionally been supported by the Central Government, getting fresh capital when needed even if the firm remains inefficient in their sector or space; and when capital is flowing into the economy this isn’t necessarily a ‘big’ risk because the government can simply funnel money into the SOE. But as problems arise and as the government gets a bit more ‘strapped,’ that support can begin to dry up, as we’ve begun to see in China.

So the Chinese government has a really difficult task on their hands. A tighter liquidity environment makes it more difficult for these fledgling companies to survive, and this could lead to major increases in unemployment. On the other hand, too loose of a liquidity environment spurns capital flows out of China, which further exhaust a declining reserves account while also transferring pressure to the rest of the world. There isn’t an easy way out here.

The Chinese government thus far has countered the problem with a series of short-term loans, but this has done little to address the rising defaults being seen in the country. Of recent, Chinese securities firms have begun to warn of rising default risk in Northeastern China, as discussed by our own Renee Mu in her article yesterday, Default Risk Spreads in Northeast China.

Rising default risks to a heavily-indebted economy could be a very dangerous thing, as this increases the probabilities of a ‘cascade-effect’ as debtors become more insolvent. We discussed this theme in-depth in January in the article, China: It’s Just a Matter of Time, and it May Have Already Begun.

As these risks increase, so does the probability that the Chinese government does something inventive in order to off-set those risks, because at this point it seems that they are well-aware that splashes of Yuan-weakness can carry a butterfly-effect through global markets; which can, in-turn, become a political issue, particularly in the midst of a U.S. election that has seen the topic of ‘trade’ become a hot-button issue.

Chinese Regulators Need to Keep Yuan at a ‘Goldilocks’ Level

For Chinese regulators at the moment, it would seem the primary goal to be one of stability; in keeping the Yuan weak enough for the near-certain slowdown that is continuing to permeate the Chinese economy to be mitigated enough so as not to hit the rest of the world. But too much weakness could be a very bad thing for China and the rest of the world, as large amounts of capital flowing out of the world’s second largest economy can create waves of monstrous proportions.

So, even though stock prices are at highs in the U.S., don’t be caught flat-footed. The primary driver here has been one of hope on the back of Central Bank policy, and hope can be erased very quickly in the face of direct-fear.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX