Talking Points:

- USD/CNH has seen aggressive price action around the adjustment to Offshore Yuan Overnight rates shooting up to a high of 66.82%.

- This essentially nullifies the prospect of staying long USD/CNH, as aggressive carrying costs combined with PBOC action make the up-trend in the pair very risky to stay long of.

- As we’ve been saying, for those that want to trade an Asian Slowdown, look to Japan. Last night’s rate adjustment is just another reminder that trading this theme in China brings on unknown and extraneous risks. Learn to manage your risk with Traits of Successful Traders.

So, I guess there is at least one area where rates are moving up, although this isn’t really the type of ‘rate rises’ that markets are looking for: Overnight rates on the offshore Yuan shot up to a high of 66.82%. That’s right – that is not a misprint. That is 6 thousand, six hundred and eighty two basis points. So before we go any further – I want to warn you about trading in USD/CNH. If you look at the chart, it would appear that a nice trend has formed. And to the trader, this can be a very good thing. But lurking under the surface is the non-predictability of a Central Bank that’s been backed into a corner. So be very careful if speculating here, especially in the direction of the trend because these overnight rates can be very, very, very costly.

But why would they do this?

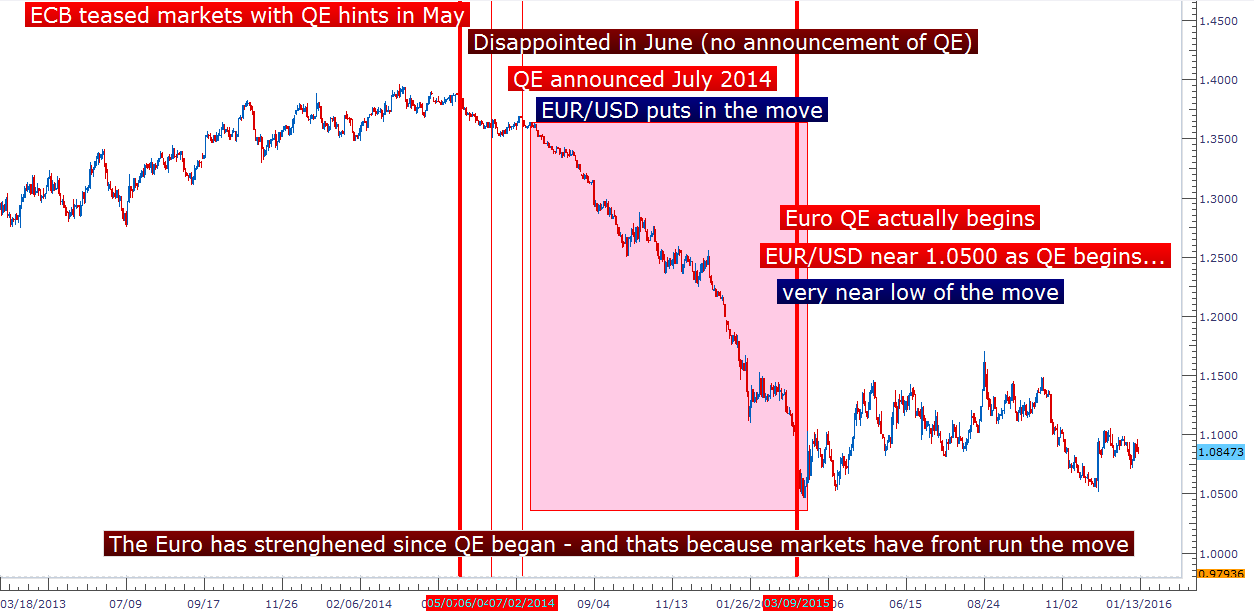

Well, there are a few reasons. Key of which is something that American and European Central Bankers didn’t address during their QE-reigns, and that’s the impact of market forces. As in, the ECB announced their QE policy in July of 2014. By the time QE actually began to take place, the EUR/USD had already put in much of the move lower, and was actually weaker than where we are at now (almost a full year into Euro-QE), and this is because investors and traders had front-run the move. Central banks were ‘ok’ with this because it helped them accomplish their goal; they wanted a weaker currency so speculators selling it on the expectation of something that was going to happen was allowing them to move towards that. The chart below illustrates the timeline of European QE, and how the QE program beginning in March of 2015 actually called the near-low of the move, amazingly enough.

Created with Marketscope/Trading Station II; prepared by James Stanley

So, from here – it appears that QE has helped hedge funds and portfolio managers far more than the average working person inside of these economies, and this is what China is looking to offset. For macro economists, this can be a good thing – but for traders looking to trade the Yuan, this can be a very, very bad thing as you’ll have to fight one of the world’s largest Central Banks.

But as we’ve seen of recent, these front-run QE moves haven’t really provided any lasting impacts to the economies that they were designed to help. Six years of QE in the United States have led to a fragile recovery that would probably be more brisk had we done no QE at all (six years is a long time for an economy to turn itself around), and Europe is still grappling with deflationary pressures across the continent despite a Trillion Euro’s being spent on bond purchases. So China isn’t allowing investors any free rides on this expectation for further Yuan weakness in response to bigger-picture pressures within the Chinese economy.

This also affords the world the luxury of not seeing a currency-sparked panic take place solely because of fear – and this is a good thing.

China is slowing down. This is not a secret, and there aren’t many people that refute this any longer. The big question is how aggressively this is taking place, and how much peripheral damage might occur. Chinese regulators have been fighting for the better part of five months now after matters got really brutal in August and September, and in some cases, it was this regulator action that really alarmed markets because it indicated that the slowdown in China may be taking place more aggressively than initially hoped or feared.

One of the biggest actions with the potential for long-lasting impact was on August 11th, and when it initially hit markets it freaked a lot of people out. This is when China modified the peg that they would use to fix the value of the Yuan each day. Previously, the Yuan was pegged to the value of the US Dollar, and regulators would set a mid-point on the Yuan based on USD and would allow their currency to fluctuate within a 2% band above or below their mid-point. The PBOC treated this very subjectively based upon their needs at the time.

The change was that the Yuan would be fixed based upon how it closes in the previous session, and it would be based upon the value of a basket of currencies rather than just the US Dollar. The obvious point of this when it was announced in August, a month ahead of the first expected Fed rate hike in nine years, was that it would allow China to keep the value of the Yuan weak as the US Dollar strengthened on higher rates and rate hike bets. Had the Yuan retained its peg to the US Dollar, the Yuan would strengthen right along with the greenback, and for an already fragile Chinese economy, this currency strength could spell real trouble for industrial production.

But perhaps more enticing to traders and investors, it signaled that Beijing wanted to guide the Yuan lower; and after six years of juicy trends driven by Central Banks, first with USD weakness and then with JPY weakness and then finally last year, Euro weakness; this was like music to the ears. A Central Bank was going to drive a trend that would allow the trader to just sit in the move and pick off the Yuan, selling rips and covering on dips. The drive for Yuan weakness is obvious – the economy is facing pressure and industrial production is still the engine that drives the ship. A weaker Yuan makes China even more competitive in manufacturing, and this is the quickest shot in the arm that the economy could get in terms of growth. This isn’t too different than those earlier mentioned themes of USD, JPY or EUR weakness, in which a weak currency offered a trade advantage that was essentially like welfare from one major economy to another. So, after China re-vamped their Yuan fix back in August, investors around the world began to speculate that the Yuan was going to continue to slide as Chinese regulators pulled out the big guns to combat deflationary forces. This created a huge spike in USD/CNH as the Yuan weakened massively on these bets.

Created with Marketscope/Trading Station II; prepared by James Stanley

But China isn’t having any of this, and this is why overnight rates have moved so brutally high. China is making it really difficult for speculators to stay short the Yuan by increasing overnight lending rates on the Yuan to such aggressive levels. So, just as I warned you at the beginning of this article – be careful of being long USD/CNH (or short Yuan), this is what regulators in China want. They want traders to NOT load the boat by selling Yuan in anticipation of a larger slowdown in Asia developing.

For traders that do want to play an Asian slowdown:

As we’ve been discussing, traders wanting to jump on this theme should cast their attention towards Japan, and this most recent bit of news is just another reason why. As a developing economy, China is still working through growing pains, and there aren’t really many precedents for how to manage a slowdown in such a large, globalized economy when there are so many external forces of pressure. New rules, or overnight announcements, or aggressive actions by the PBOC are likely; and will continue to be so for the foreseeable future, at least as long as China is grappling with these deflationary forces.

This is unknown risk. This is a trader’s worst enemy because it can’t completely be accounted for. So in many cases, it should just be avoided altogether.

Japan, however, is already large and developed; perhaps too much so. And further to this point, the Bank of Japan has far less flexibility than does the People’s Bank of China. Japan’s three years of QE have stretched the bank massively, and now, there are numerous questions as to whether they’d even be able to increase QE even if they did want to. But they may not want to – the Bank of Japan got a very rude reminder of the danger of market forces with those stock slides in August and September. The Government Pension and Investment Fund (GPIF) lost a whopping $64 Billion off of that volatility; a full -5.5%+ drawdown on an over Trillion Dollar portfolio. So, if they’re not too quick to take on additional risk that would be completely understandable.

So Japan is vulnerable on multiple fronts. Until QE came into Japan, the country was still mired in the midst of their ‘lost decades’ in which deflation was continuing to ravage the economy. Sociology isn’t on Japan’s side either, as a dwindling population will see a contraction of 1/3rd by the year 2060. So, just to keep GDP flat, we’d need to see GDP-per-capita increase by 150% over this period just to print the same GDP numbers that we have today. And even if Japan gets there unfettered, there are two people over the age of 75 for every one person under the age of 15. So entitlement benefits are going to bring rude consequences in the coming years.

China, on the other hand, is young and has a billion people. The one-child policy that was recently repealed in the country as created a sociological quagmire not-too-different than the one in Japan. The difference is that China has a billion people, so their margin of error is far less as those trends can change quickly. On top of that, China is full of arable land that isn’t currently occupied that can be populated with immigrants (which is a very good thing when speaking economics). We discussed this theme of sociology in relation to market forces in the article, China as Japan 2.0.

For now, the chart below shows the current setup in the USD/JPY, and this Yen strength can be extrapolated across currencies against the Sterling, Euro or Australian Dollars. Should risk aversion continue, we will likely see continued repatriation of the Yen from all of those retirees that have sent their weak currency out of the country in the constant search for yield.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX