This daily digest focuses on market sentiment, new developments in China’s foreign exchange policy, changes in financial market regulations and Chinese-language economic coverage in order to keep DailyFX readers up-to-date on news typically covered only in Chinese-language sources.

- The PBOC’s guidance is still the top driver for Yuan moves; impact from imports and exports is limited.

- Chinese securities firms warn investors on the spreading default risk in Northeast China regions.

- Manufacturing firms are facing internal and external challenges to meet the required production cuts in 2016.

To receive reports from this analyst, sign up for Renee Mu’ distribution list.

Sina News: China’s most important online media source, similar to CNN in the US. They also own a Chinese version of Twitter, called Weibo, with around 200 million active usersmonthly.

- The major driver to the onshore Yuan’s moves was the PBOC’s guidance on Monday. The Central Bank set the daily fix for the Yuan by -209 pips or -0.31% weaker against the US Dollar, responding to the Dollar strength led by a better-than-expected Non-Farm Payrolls print last Friday. Within the first 45 minutes following the PBOC’s release, the onshore Yuan (USD/CNY) lost -0.18% to 6.6633 while the offshore Yuan (USD/CNH) dropped -0.06% to 6.6723.

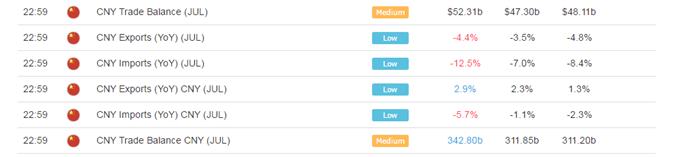

- China issued disappointing July import and export figures on Sunday while Yuan rates strengthened following the release. As is shown on the DailyFx Economic Calendar, China’s trade balance has greater importance than just the amount of exports and imports, and therefore, an improved trade balance coupled with weakened imports and exports could bring a net positive impact to Yuan rates. The Yuan’s moves on Sunday followed this thesis: The offshore Yuan (USD/CNH) gained +0.04% in the first 10 minutes after the release.

China Finance Information: a finance online media administrated by Xinhua Agency.

- Increasing defaults in state-owned enterprises (SOEs) in Northeast China could trigger a domino-effect in the region. Northeast China is comprised of three provinces is a major traditional industrial base for the country and was once famous for its heavy industries. However, after seven defaults made by Dongbei Special Steel within four months, investors not only raised concerns on the SOE itself, but also on its sponsor - the Liaoning provincial government as well as other SOEs in the region. According to Xinhua News, a company with an above 70% debt-to-asset ratio is common to see in the region, which is beyond the more-normal levels of 40% to 60%. Due to increasing default risks in the region, local SOEs are finding it harder and hard to finance on-going operations: This year at least 12 corporate bonds have been canceled at issuance. An incredible high debt ratio of 157.7% in Liaoning province makes the local government incapable of supporting SOEs even if they wanted to. Therefore, multiple Chinese securities firms have warned investors of a potential broader crisis in Northeast China regions.

- China is facing increasing challenges in production cuts that are set to be completed over the rest of 2016, with obstacles from both inside and outside the country. In the first seven months, only 38% of reductions in coal production and 47% of reductions in steel production have been achieved. As local governments worry about negative impacts of production cuts to the regional economy, they have slowed down the pace of production cuts. More than ten provinces in China (equivalent to states in the U.S.) have not yet started the substantial work of resolving overcapacity in coal firms. Most of the provinces assigned over 50% of required steel production cuts in the region to the last quarter of 2016. This has raised the Central Government’s concerns on whether they are able to achieve the target by the end of this year.

What makes the condition even more challenging is that imported coal in the first half of 2016 increased +8.2% from a year ago while total consumption dropped -4.6% over the same span of time. Growth in imported coal was especially high in May and June; the annualized increase was 33.6% and 31.0% respectively. This means that while China’s domestic manufacturing companies are working hard to cut production and struggling to survive, the imported products have eased a portion of their efforts. According to China’s General Administration of Customs, the increased imports in energy products were driven by more favorable import prices: The import prices of iron ore, crude oil, coal and steel in the first seven months dropped -13.3%, -29.6%, -18.8% and -9.4% respectively. The continued rising imports in these products could hurt China’s manufacturing companies’ incentive on further capacity cuts.

To receive reports from this analyst, sign up for Renee Mu’ distribution list.