S&P 500, FOMC, Dollar, USDJPY, EURUSD, Yields and Recession Talking Points:

- The Market Perspective: USDJPY Bearish Below 141.50; Gold Bearish Below 1,680

- Beyond the FOMC’s decision to hike its benchmark rate range 75bps for a third consecutive meeting; it upgraded its rate forecasts and cut the GDP outlook

- A Dollar rally and S&P 500 slide after Wednesday’s event seems reasonable, but there are deeper implications and more provocative event risk ahead

A Break from the Typical FOMC Response

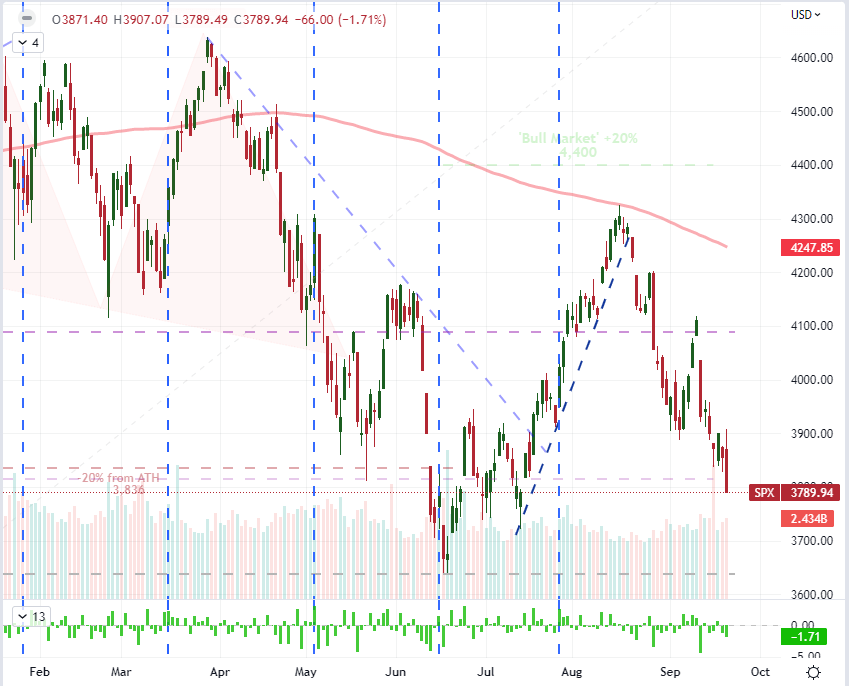

The Fed’s rate decision has likely altered the course of the broader financial markets moving forward. If you watched the FOMC event in real time this past session, you would have seen some healthy debate around how the market was interpreting the outcome. Risk assets in particular were remarkably volatile through the more than hour-long affair with sharp switchbacks. However, the ultimate course setting we have ended on seems bearish. That does not mean that the trend is set, but there will likely be a greater sensitivity to economically-compromising developments moving forward – a risky prospect with a run of major central banks due to announce their own policy mix and the high-level GDP-related data for September due on Friday. Breaking a trend of four consecutive FOMC decisions that ended with a positive performance from US equities, the S&P 500 closed Wednesday with a -1.7 percent dive to two-month lows. While the follow through of this benchmark is worthy of our attention, I am just as interested in tracking the course of liquidity. As a reminder, September historically sees an upturn in volume along with the start of a peak in volatility and the only month of averaged losses for the index of the calendar (averaging performance back to 1980).

Chart of S&P 500 with Volume, Fed Decisions, 200-Day SMA and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

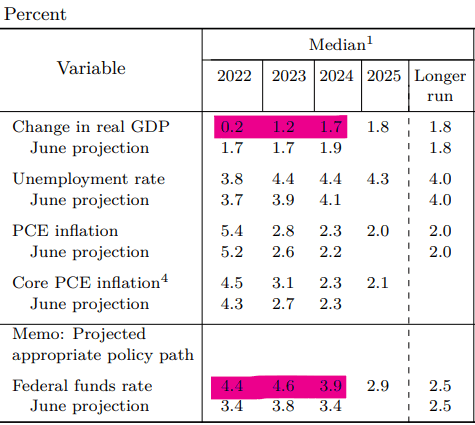

There was a lot to digest in the FOMC rate decision this past session, and that no doubt contributed the exceptional short-term volatility around the event itself. The initial announcement of the 75bp rate hike was exceptional as the third such move in a row but it was also essentially in-line with expectations. That immediately shifted the focus to the Summary of Economic Projections (SEP) released at the same time as the policy announcement. Most traders that track the Dollar and rate differentials honed in immediately onto the rate forecasts. The central bank’s year-end forecast for the benchmark rate range was set higher than what the market’s already-hawkish view allowed for: a 4.4 percent average rate that that was 100 basis points higher than June’s forecast and above the 4.2 percent forecast from the market. That would play to the risk downgrade and Dollar boost, but my principal concern was the sharp downgrade in growth forecasts. For 2022, the previous 1.7 percent projection was cut severely to 0.2 percent which would insinuate a significant probability of an official recession – which the NBER has tentatively delayed with a definition ‘clarification’ not long ago. As for Powell’s remarks, his reiteration that inflation is the principal concern was the clearest message I registered.

FOMC Summary of Economic Projections from June 15, 2022 Meeting

Table from Federal Reserve’s SEP

And Now that the Fed Inertia Has Passed…

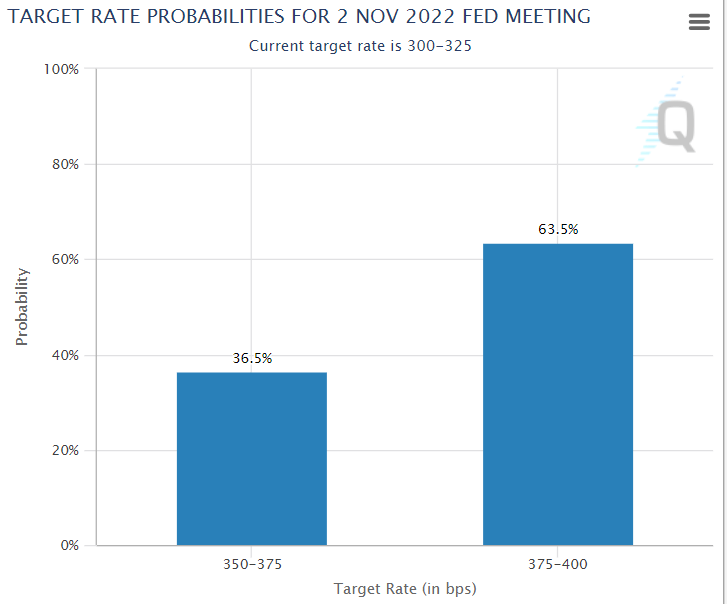

While many were looking to the Fed decision to dictate the market’s next significant move, I saw it more as an encumbrance to purposeful development. There was no doubt that the event carried extraordinary influence for speculative conviction, but this and other major central banks typically look to avoid triggering serious volatility that they need to then quell. There are certainly adjustments that will matter to the future but the change in the speculative compass is not particularly severe from where the market’s were reading the stars. From the Dollar’s perspective, the rate forecast moving forward seems to be exacting greater weight than I had expected. The Greenback rallied widely with pairs like EURUSD and USDCAD pushing even further in favor of the Dollar. EURUSD pushed fresh multi-decade lows below 0.9900 while USDCAD soared through 1.3400 to make clear its break through the midpoint of the post-Pandemic range. With a 64 percent probability of a fourth 75bp hike at the November 2nd meeting immediately after this big hike, the buoyancy is not so surprising.

FOMC Scenario Table with Potential Market Impact

Table Created by John Kicklighter

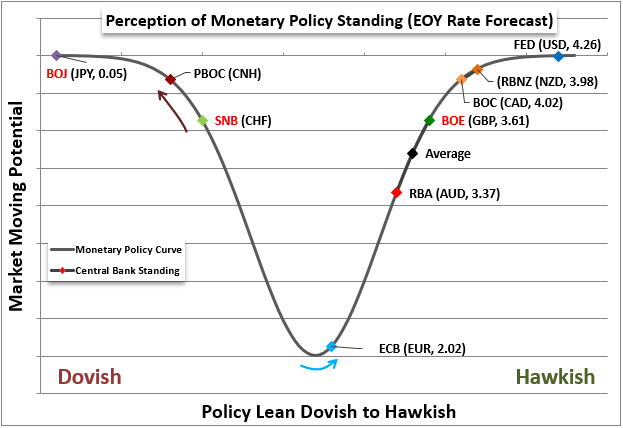

Heading into this week’s Fed decision, I did not expect the needle to move significantly on the relative yield perspective the Dollar. That is because the year-end forecast for the FOMC was already top-of-class amongst its peers. That would suggest that the hawkish advantage would already be significantly discounted. That said, having the FOMC push its forecast even higher than the market’s high water mark would certainly add additional charge. More than just the lagging Euro or the competitive Loonie, there were also notable breaks against the typical ‘carry currencies’ in the Australian and New Zealand Dollars. For GBPUSD, the extended slide comes with serious repercussions as a drop below 1.1300 has not been seen since 1985. This is a remarkable fundamental contrast, but I don’t think the uplift is a foundation for a sustained Dollar driver. With the outlook for growth deteriorating and the rest of the world likely to feel the fallout from the FOMC’s policies, there are complications that can complicate our course.

Chart of Relative Monetary Policy Standings Among Major Central Banks

Chart Created by John Kicklighter

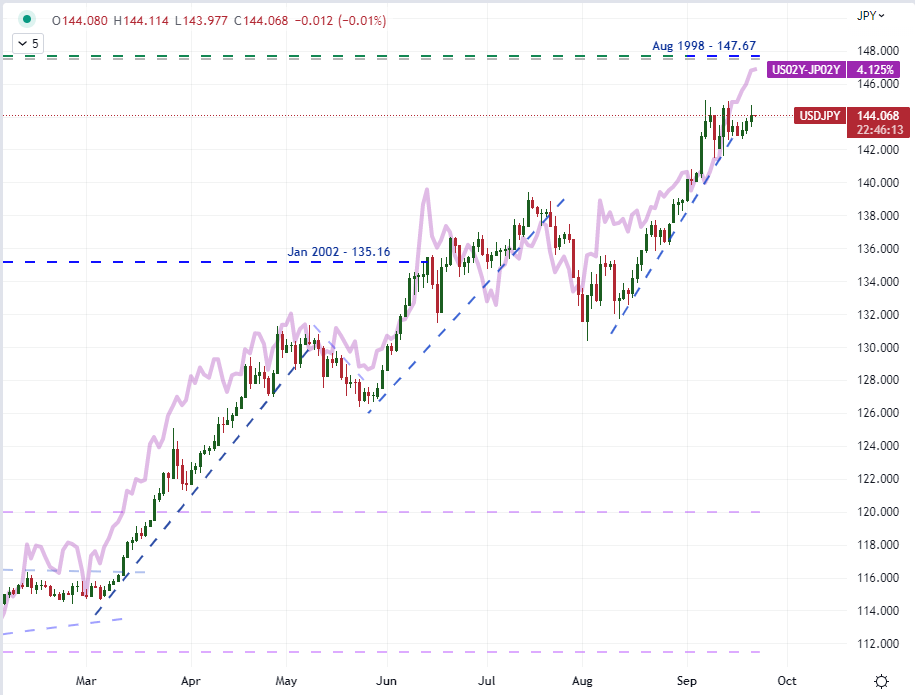

USDJPY and US Yields: Rates and Recession

While there seemed to be a clear response from the Greenback to an upgraded local rate forecast, it was principally the pairs that were considered ‘balanced’ that saw the brunt of the volatility. In contrast, the market’s leading example of divergent monetary policy, USDJPY, was noticeably anchored. It isn’t that rate differentials haven’t picked up here as well, rather the markets have already made a significant bid to discount significant imbalance for this cross. What’s more, there is the complication in that the Bank of Japan (BOJ) is due to weigh in on its own monetary policy mix this morning. Economists and markets expect the group to commit to its extremely accommodative policy and resort to corrections like the large bond buying efforts reported Wednesday morning. Just like the Fed decision was a curb through anticipation, we should watch to see the market’s intent after the Japanese authority has its say. The higher we go, though, I suspect the desperation from policy officials will build to an eventual public intervention effort.

Chart of USDJPY Overlaid with US-Japan 2-Year Yield Differential and Correlations (Daily)

Chart Created on Tradingview Platform

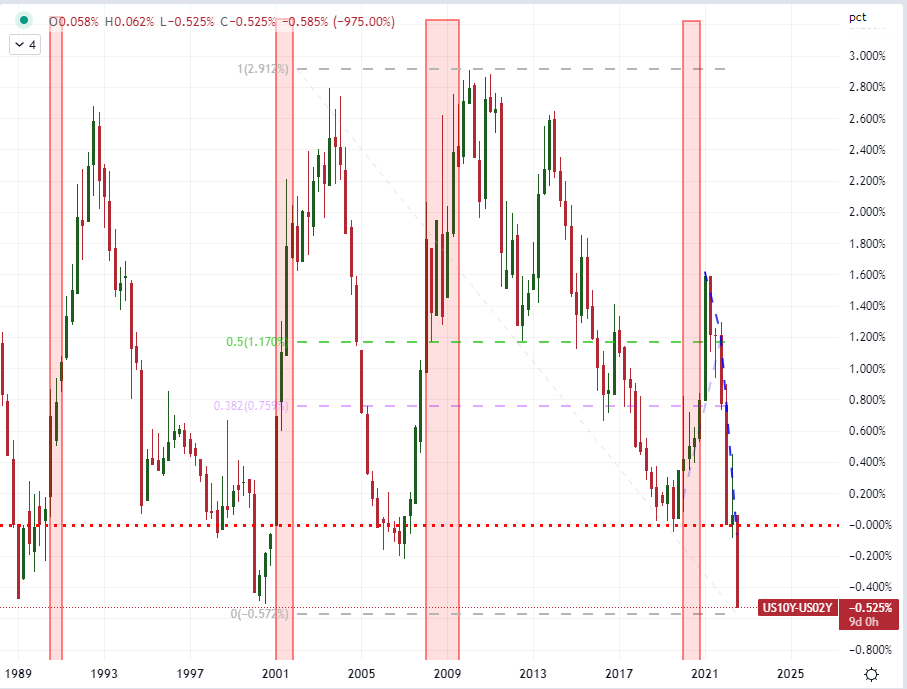

As we wade through a busy, final 48 hours of trade for the week; my attention will be on the undercurrent of recession concerns. Tactically chasing slightly higher rates of return matters little if the underlying financial and economic situation is essentially eroded. We are still seeing the aftermath of a market that has formed its core memories around the complacency inspired by stimulus from governments and monetary policy authorities. As conditions continue to erode while these same saviors reiterating their commitment to fight inflation first and foremost, the personal exposure to risk will set in. As a stark reminder of our current situation, the surge in 2 year Treasury yields (more aligned to rate speculation) and the slip in 10-year (more growth reflective) has pushed the ‘recession warning’ measure 2-10 spread to its deepest point of inversion since September 1981.

Chart of US 10-Year to 2-Year Yield Differential with Highlighted US Recessions (Monthly)

Chart Created on Tradingview Platform

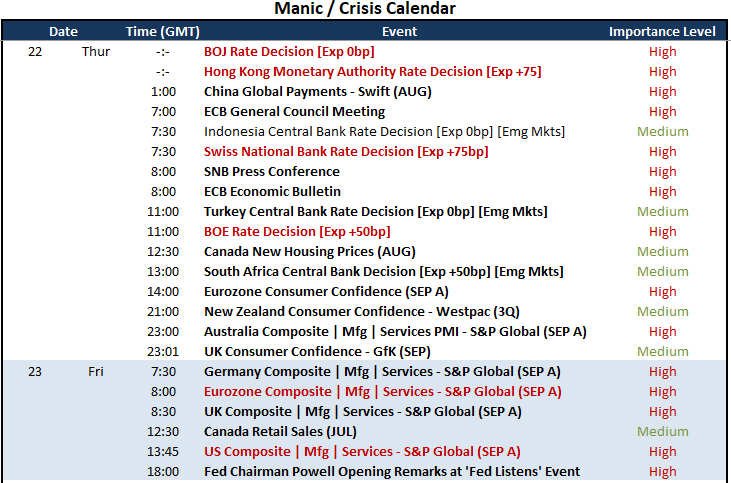

What’s next? The economic docket through Thursday’s session is a mine field of central banks that will test the waters that the Fed has made significantly more treacherous. The Bank of Japan and Swiss National Bank will offer up the scope of dovish contrast to the Fed’s hawkishness. If the BOJ holds its near-zero bearing, it will increasingly put it at odds to its global counterparts. Meanwhile, the SNB is seen following in the ECB’s footsteps, but that will likely further the EURCHF’s stretch to already-record lows. The Bank of England is another big picture counterpart, but here I’m more interested in the relative growth considerations between the US and UK. As for the Hong Kong Monetary Authority, an expected 75bp hike is reasonable to keep the USDHKD band in place, but it puts it further at odds to mainland China’s dovish hold. Further out to Friday, we will shift more wholly to the weigh recession risks in the September PMIs.

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team