S&P 500, VIX Index, Financial Conditions, ISM, Employment and AUDNZD Talking Points:

- The Market Perspective: USDJPY Bearish Below 141.50; Gold Bearish Below 1,680

- The S&P 500 put in for its biggest single-day rally – a 2.6 percent surge- from 22-month lows, but it looks to have more to do with temporary seasonality than conviction

- Historically, the VIX and market volume are expected to peak in October which is a troubling proposition against a backdrop of fear of recession and financial instability

S&P 500 and VIX: Seasonal and Structural Sentiment

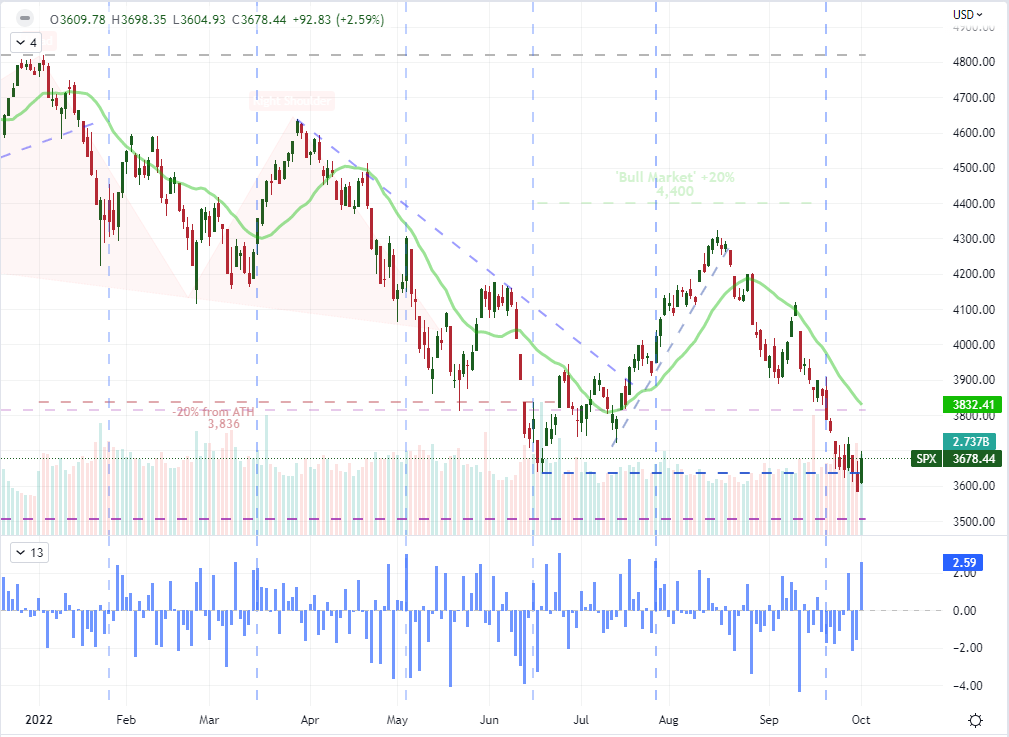

With Monday’s session, we have opened more than just a new trading week. It is also the start for October and the fourth quarter. There is a lot of seasonal capital flow associated to this transition, and those tides may have had more to do with the charge in risk appetite this past session that more traditional means of fundamentals or technical progress. That matters because a seasonal influence is inherently limited in duration. That is not to mean that we cannot transition into a more robust motivation for the masses to build on a view; but without some additional means of transportation, the run could end quickly. As for the ‘risk’ performance specifically Monday, the 2.6 percent rally from the S&P 500 seemed to lead the way. It was the biggest single day rally in over two months – specifically July 27th, the day the Fed hikes benchmark rates 50 basis points – but it marks relatively limited progress from 22-month lows and a multi-week slide of -17 percent.

Chart of S&P 500 with Volume, 20-Day SMA and 1-Day ROC (Daily)

Chart Created on Tradingview Platform

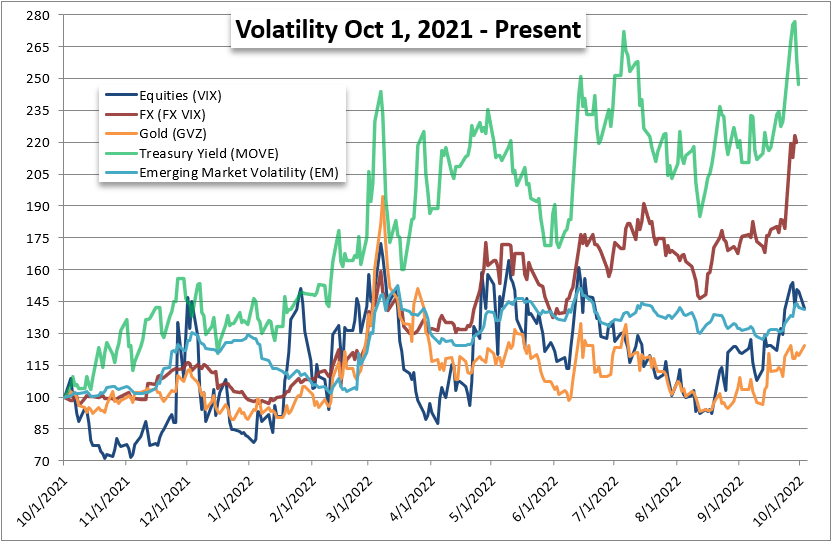

My skepticism around mounting a lasting bullish reversal certainly draws on the technical and fundamental backdrop. In addition to the larger bear trend of 2022, the thematic outlook sees a serious concern around the probability of a global recession along with a not-insignificant-concern that financial conditions can be destabilized in the fight against rampant inflation. Given that that the world’s major central banks have built up an enormous pool of stimulus over the past decade upon which speculators have shifted their personal sense of risk exposure, there is both excessive leverage in both the notional and thematic sense. Expected (implied) volatility is high across the financial system – and particularly in yields and FX – which puts the financial markets unease. It was Franklin D Roosevelt who said in a speech in 1933 that there was ‘nothing to fear but fear itself’. That may have been reassuring in that context; but for markets that are driven by herd mentality, it can be devastating nonetheless. And given the historical norms of volatility peaking in October, it is a reason to worry.

Chart of Relative Equity, FX, Gold, Treasury and Emerging Market Volatility (Daily)

Chart Created by John Kicklighter

Recession Worries in ISM Data and Focus in the Jobs Figures Before NFPs

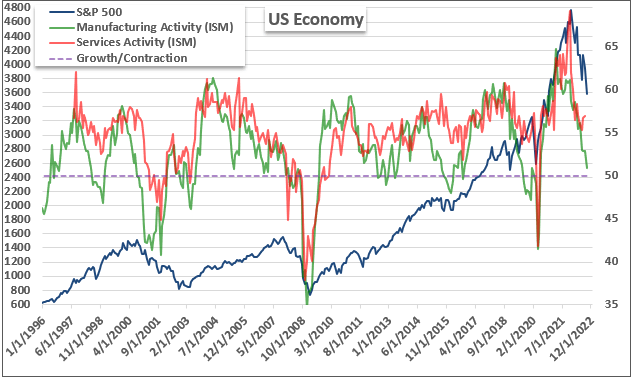

Seasonality and sentiment are abstract but critical threats to monitor moving forward. It is difficult to project how the crowd’s views will change over time, but it can be informed by more prosaic fundamental themes. One area of concern that I have been tracking these past months is the view that recessions are probable, if not inevitable. The perception of a ‘soft landing’ has clawed its way back into the popular view for the US and globally these past weeks, but that optimism was knocked down a peg this past session with the release of the ISM manufacturing report for September. While it was expected to have slowed this past month, the 50.9 reading was far more constrained than was anticipated. Furthermore, with the employment (48.7) and new orders (47.1) component both dropping sharply from the past month and in ‘contractionary’ territory, the forecast is serious. At the very least, the attention on the service sector report later this week will be markedly more intense.

Chart of S&P 500 Overlaid with Manufacturing and Services ISM Surveys (Monthly)

Chart Created by John Kicklighter with Data from ISM

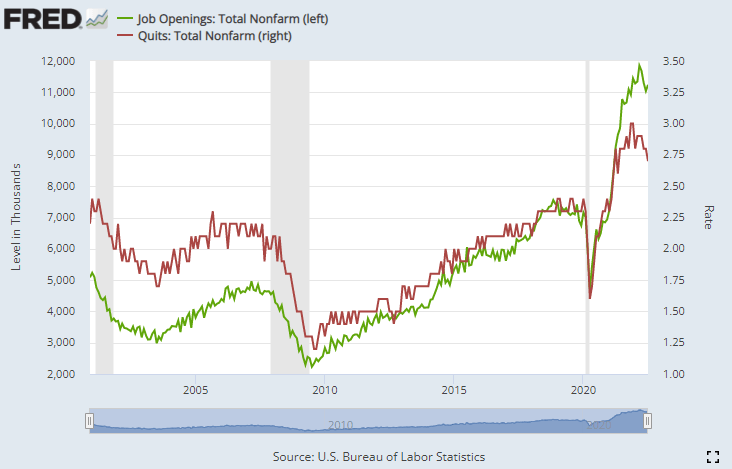

If we are indeed paying closer attention to the health of the world’s largest economy, then the run of employment data we are heading into can gain some serious market-based traction. With the ISM factory employment reading dropping in yesterday’s report, there is likely to be a marked escalation in the interest (perhaps fear) around the September nonfarm payrolls due for release on Friday. In the meantime, we are traversing a range of meaningful employment data that will feed into that eventual release. In Tuesday’s session, the JOLTs job openings and quits figures will be particularly informative. We have witnessed an extraordinary labor markets post-pandemic with Americans seemingly in control of their employment destiny, but those heydays may have passed.

Chart of US Job Openings and Total Quits from JOLTs (Monthly)

Chart Created on St Louis Federal Reserve Economic Database with Data from US BLS

Key Events and Interest Rate Speculation

When it comes to market potential, I believe that market conditions such as liquidity then the potential for recession threat analysis are the top concerns. That said, these are not particularly reliable in offering progress at a regular cadence. With an allowance for threats from the headlines and ‘out of the blue’, there is also plenty of event risk scheduled on the docket. And, looking over the macro calendar, I would say that much of the event risk is centered on monetary policy speculation. This past session, there were a number of Fed officials speaking on various topics, but John Williams and Tom Barkin stood out for me. The former suggested that inflation would fall quickly in 2023 as a dovish mea culpa to the market, but the latter touched on a possible increased volatility norm in monetary policy and acknowledge a possible Dollar contagion risk. I will be watching to see what Lorie Logan, Loretta Mester, Philip Jefferson and Mary Daly have to say in the upcoming session. Add to that watch list ECB President Christine Lagarde.

Critical Macro Event Risk on Global Economic Calendar for the Next 24 Hours

Calendar Created by John Kicklighter

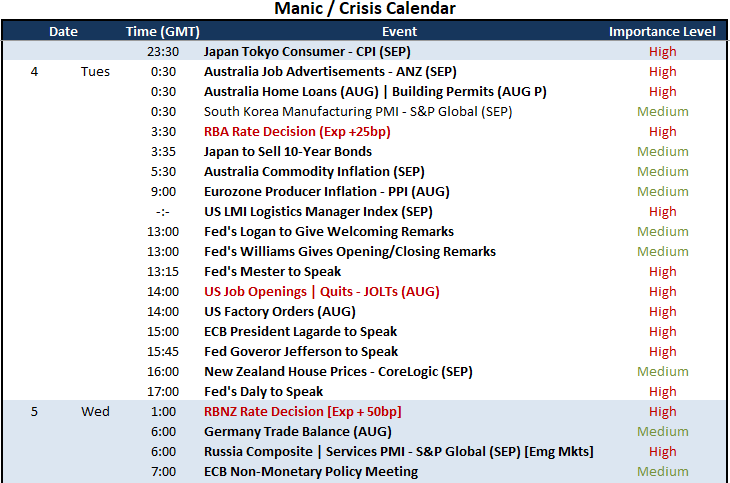

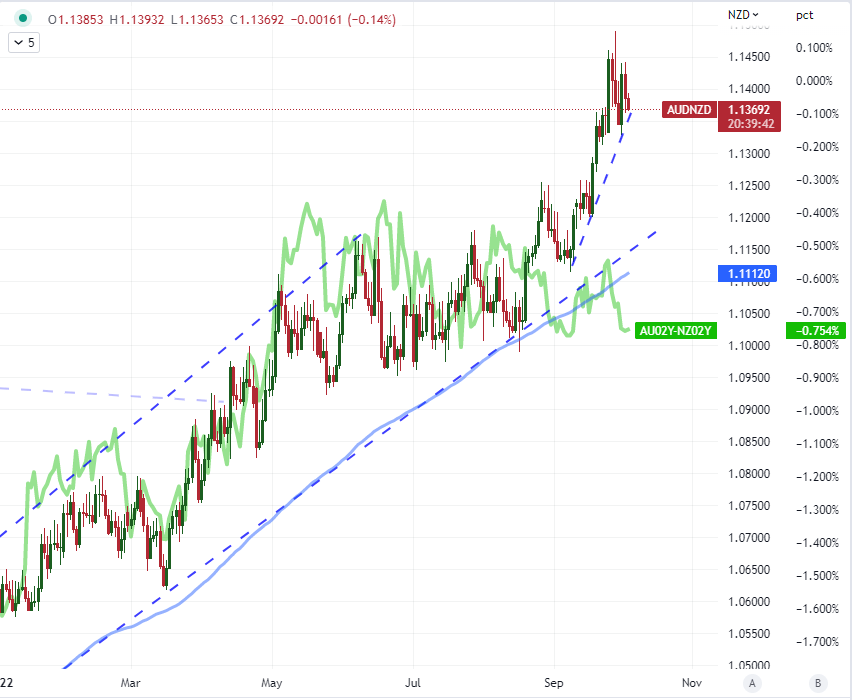

If you are watching monetary policy, then it should be said that we will get closer than just aggregating central bank members’ views on their collective course. On tap for Tuesday morning is the Reserve Bank of Australia (RBA) rate decision and then Wednesday morning will offer up the Reserve Bank of New Zealand (RBNZ). Both are expected to hike their respective benchmark rates by 50 basis points. That said, both of these historical carry currencies have given up significant ground to the likes of the US Dollar as they have flagged the pace of tightening of the world’s largest currency and policy group. That makes fundamental pictures for AUDUSD and NZDUSD harder to focus, but the comparison of AUDNZD is more interesting to me. Notably, the correlation between the exchange rate and the Australian-New Zealand 2-year yield spread has broken materially these past two months.

Chart of AUDNZD with 100-Day SMA Overlaid with AU-NZ 2-Year Yield Differential (Daily)

Chart Created on Tradingview Platform

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team