Short EUR/GBP: A Hawkish BoE and Price Action Support Further Downside.

The Great British Pound has been on a tear of late, even before the 50bps surprise delivered on the June 22. The Euro itself enjoyed a bit of a renaissance of late with EURGBP bouncing as a result with the pair trading around the 0.8593 at the time of writing.

The Bank of England (BoE) has seen an increase in rate hike probabilities following a blockbuster inflation reading in May. The European Central Bank (ECB) on the other hand has stuck by its hawkish rhetoric yet seems to be running slightly out of steam as economic conditions remain a concern. Given that the UK economy is exceeding expectations as mentioned by both Chancellor Hunt and PM Sunak following the June BoE meeting, I do expect the UK and its rate hike path to be a more realistic one than that of the ECB.

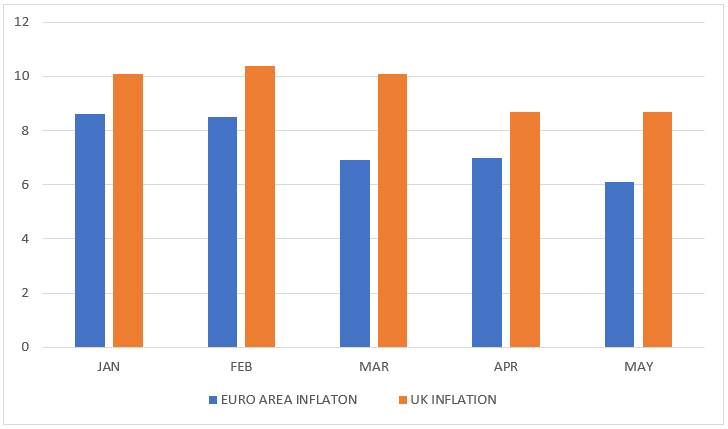

Inflation as well remains more elevated in the UK compared to the Euro Area providing another form of confirmation that the BoE may need to be more aggressive than the ECB moving forward into Q3.

UK VS EURO AREA HEADLINE INFLATION IN 2023

Source: MS Word, Excel. Created by Zain Vawda

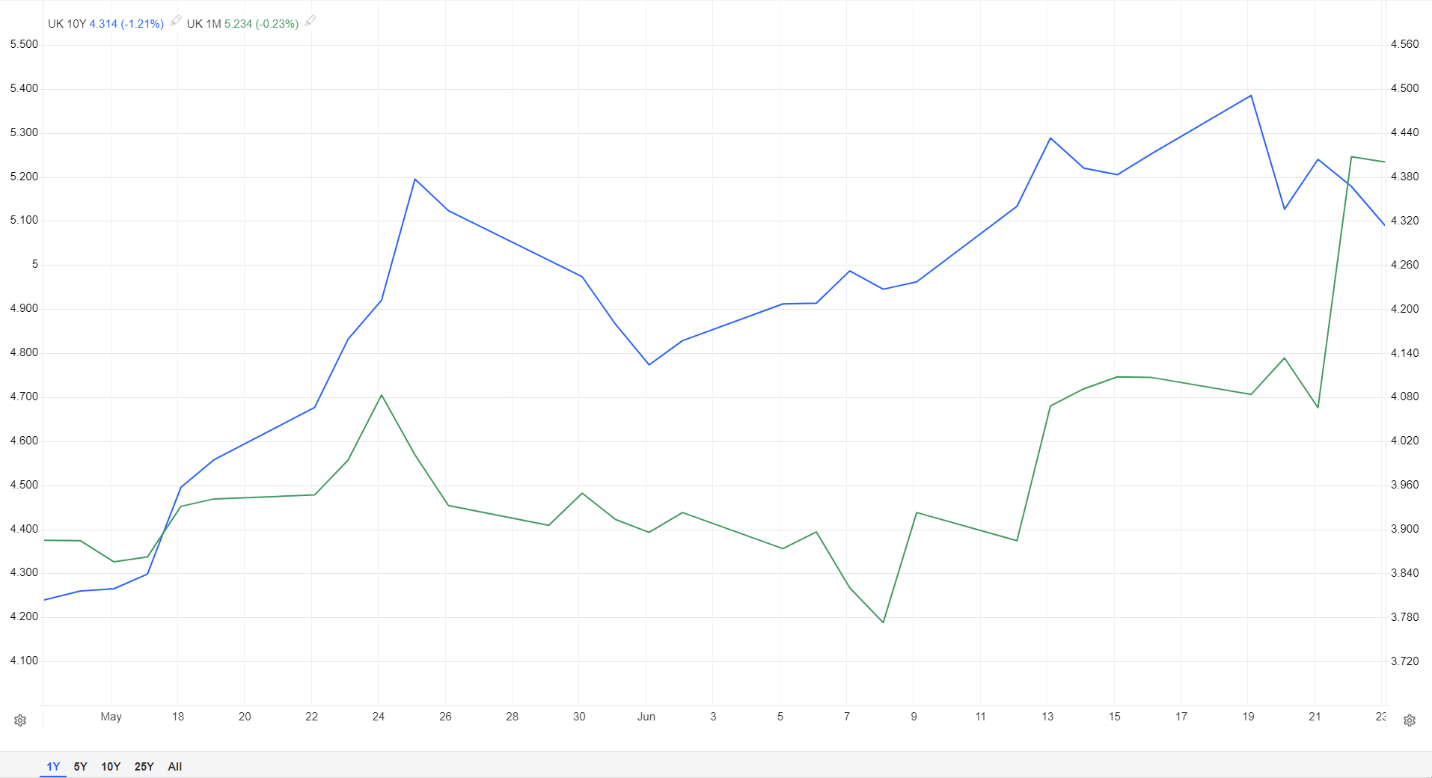

This might be the first time you are hearing this but for once an inverted yield curve may be a positive at least where the GBP is concerned. An inverted yield curve could in theory work to the advantage of a reserve currency like the GBP with a similar story appearing to take place in regard to the US dollar. Just another reason why I believe the GBP will remain supported in Q3 and gain against many of its G10 peers.

UK Yields 10Y Vs 1M

Source: TradingEconomics, Created by Zain Vawda

TECHNICAL ANALYSIS

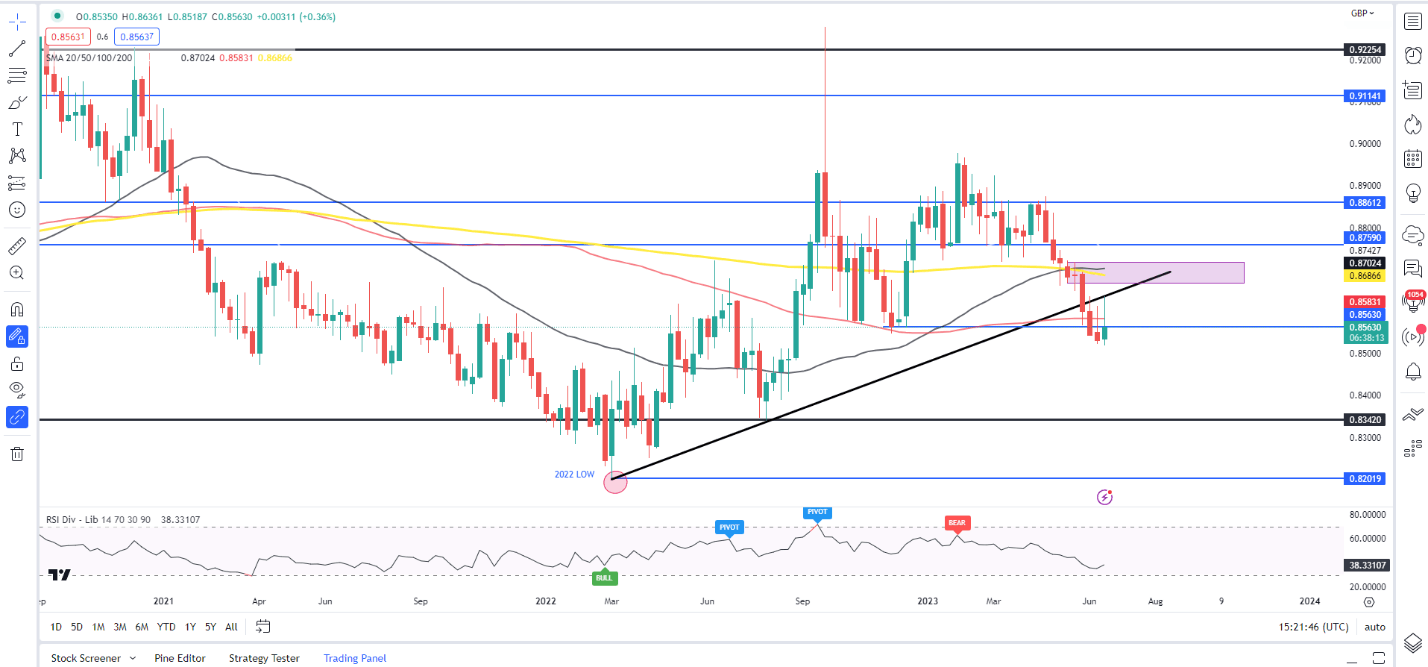

From a technical perspective, looking at the market structure on a weekly timeframe and we have just broken the overall bullish trend which has been in play since the March 2022 lows. A break and weekly candle close below 0.8560 confirming a change in structure to bearish while at the same time breaking below the ascending trendline.

The current weekly candle has retested the trendline this week before rejecting with the 100-day MA providing resistance as well. The weekly candle is on course to close as an inverted hammer candlestick hinting at further upside in the week ahead preferably toward the 0.8700-0.8800 mark. The overall bearish trend will remain intact without a weekly candle close above the 0.8862 handle.

EUR/GBP WEEKLY CHART

Chart prepared by Zain Vawda, TradingView

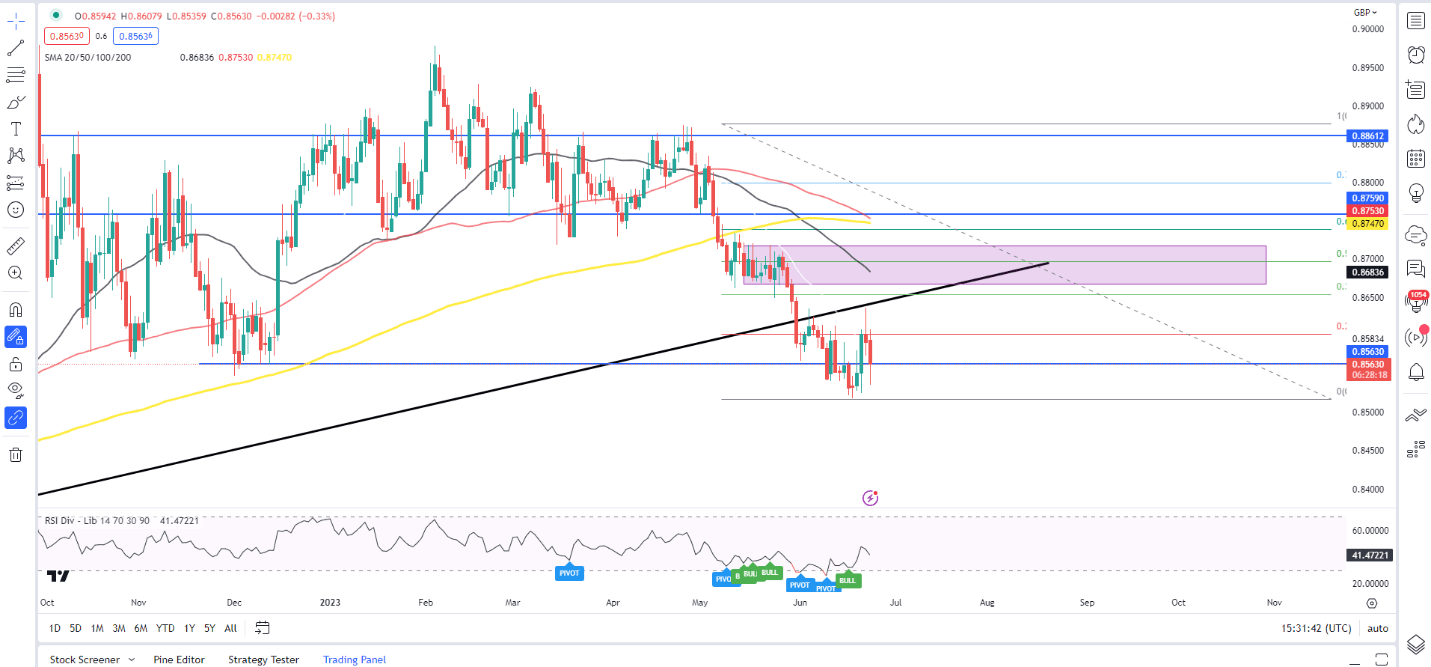

Now given what price action is telling us on the weekly timeframe a deeper retracement cannot be ruled out at this stage with the 0.8700 level looking particularly inviting with a host of confluences resting there.

On the daily chart we also have a death cross pattern forming as the 100-day MA is about to cross below the 200-day MA, a further sign of the bearish momentum in play. If we look at the daily chart below, I will prefer a pullback toward the 0.8700 mark as that would provide an even better risk-to-reward opportunity for potential shorts. Downside targets will be resting around the 0.8342 mark and below that at the 2022 low around the 0.8200 handle.

EUR/GBP DAILY CHART

Chart prepared by Zain Vawda, TradingView

Contact and follow Zain on Twitter @zvawda