S&P 500, VIX, FOMC, Dollar and EURUSD Talking Points:

- The Market Perspective: USDJPY Bearish Below 137; GBPUSD Bullish Above 1.2300; S&P 500 Bearish Below 4,030

- Despite the presence of the FOMC rate decision Wednesday, the markets reacted to the sharper-than-expected slowdown in US CPI

- Volatility and trend are two separate matters when it comes to the clash between the Fed decision and liquidity expectations ahead…and don’t forget it isn’t just US event risk on tap

There was an extreme bout of volatility from the broader markets Tuesday. Though it would register through global indices, emerging markets, junk bonds and beyond in broader risk spectrum; the core of the fundamental impact this past week proved the US equity market and the Dollar. Naturally, a closely-watched inflation update for the United States would do more to charge local assets; but it is also important to recognize the global reach of these benchmarks. Indices like the S&P 500 and Dow are signposts for global sentiment while the Dollar is the most heavily used fiat for transaction and wealth storage by a wide margin. We witnessed an incredible test of that influence this past session with the US CPI. With the headline reading slowing more quickly than expected (7.1 vs 7.3 percent) along with the core (6.0 vs 6.1 percent), there was clear fodder and an easy historical lesson from November 10th to elicit the market’s response. Yet, the incredible gap higher on the open (second largest in 25 months) and temporary clearance above the 2022 bear-defining trendline around 4,060 proved very short lived. After a run as high as 2.8 percent higher on the day (4.0 percent for futures which found its peak well before the exchange open), the market ultimately retraced much of its gains and closed back within its past month’s range.

Chart of the S&P 500 with Volume, 20 and 200-Day SMAs (Daily)

Chart Created on Tradingview Platform

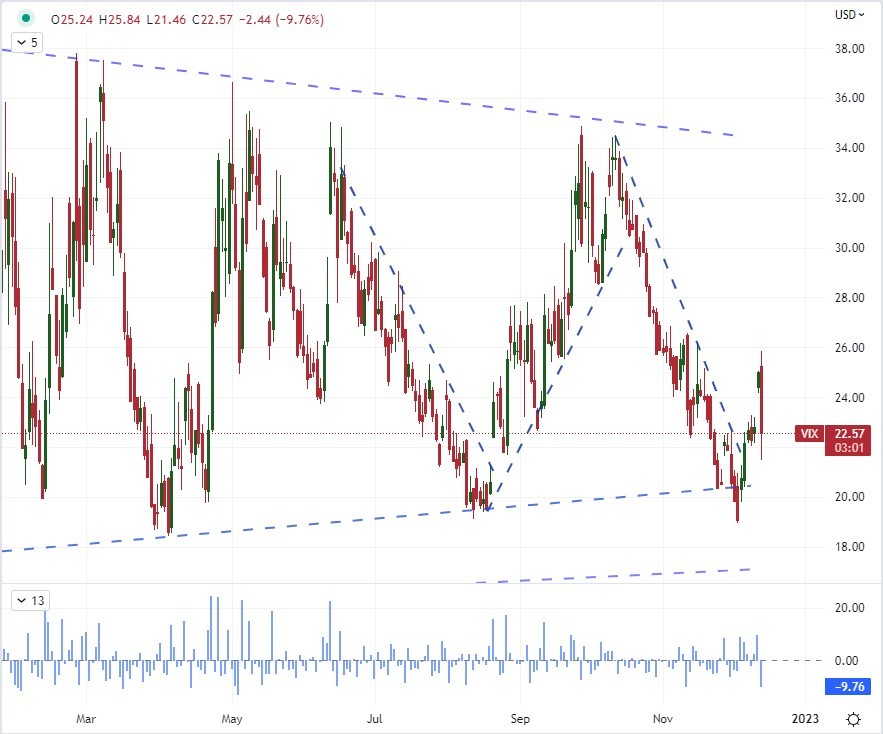

Fundamentally, the US inflation data is readily superseded by the FOMC rate decision. Price pressures draw much of their macroeconomic sway from interpretations as to how the data will influence the central bank’s policy moving forward. That is likely why the initial reaction from the market was significantly reversed – and perhaps why the Dollar’s move was more measured by sticky. Yet, if the priority has always been the Fed’s upcoming policy decisions, why did the markets move so dramatically on CPI? Volatility. Anticipation is very high for this upcoming session’s top listing. That exacerbates the curb in participation beyond the typical year-end restrictions and it further amplifies the impact of repricing forward rates. This is the kind of backdrop that can generate severe activity while ultimately struggling for trend development. Far more remarkable to me this past session was the sharp decline in the VIX after Tuesday’s inflation release. The gap higher on Monday seemed to defy the month-long projection of the ‘fear index’ but it was fitting given this week’s event risk. Seeing the risk premium drain from the market before the Fed decision is perhaps even more remarkable. These are unusual conditions indeed.

Chart of the VIX Volatility Index and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

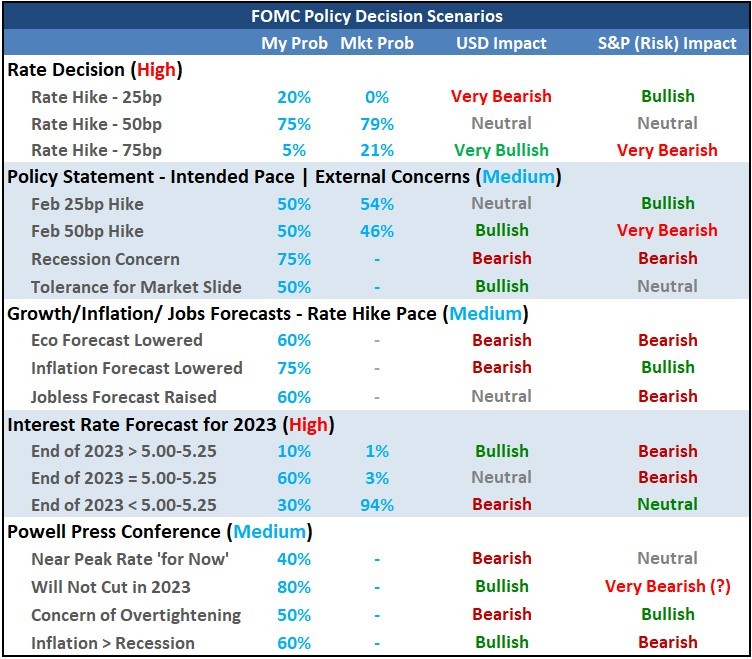

We will see just how topsy turvy the financial backdrop is with the release of the FOMC rate decision ahead. There are different stages to this event for which fundamental traders will need to prioritize their focus. The monetary policy statement and Chairman Powell press conference half an hour after the initial release will focus on nuance which will be easily drowned out by more binary developments. The rate decision itself is of great interest, but the probability of a 50 basis point hike seems to be highly probably. If it is anything other than a 50bp increase, it will be the principal factor on the day. More likely, if that still-hefty half-percentage point hike is confirmed, it will likely reflect as a neutral outcome by market participants regardless of those arguing it is a slow down of the 75bp clip of the past four meetings or the hawks that would say it defies the CPI data. In that case, attention will immediately snap to the Summary of Economic Projections (SEP). While the outlook for growth, employment and inflation matters; the rate forecast for 2023 will give more traction to what is ahead. Further, given the Fed has reiterated that it is confident it won’t lower rates in 2023, the forecast though year’s end will stand as the ‘terminal rate’.

FOMC Scenario Table with Events, Probabilities and Dollar/S&P 500 Impact

Table Created by John Kicklighter

I believe the biggest volatility response from ‘risk assets’ in the upcoming FOMC decision is around their expectations for the terminal rate and the degree of effort made to convince the market that the central bank will not be cutting its benchmark over the coming year. That has been where most of the day-to-day market action has been around this fundamental theme, and they will endeavor to provide as clear a signal as possible. This is likely to lead to considerable volatility but will be less likely to generate follow through. On the Dollar side of the equation, the Greenback could experience the inverse: less of the extreme volatility but could generate more trend. Certain pairs will experience more of the impact than others. One pair that will be particularly interesting is EURUSD. The cross has critical technical levels overhead heading into the event. A long-term trendline, big Fibonacci level and previous swing low are around the 1.0700 level. That said, we have the ECB rate decision ahead which could offset or amplify what this pair does.

Chart of the EURUSD with 20 and 200-Day SMAs (Daily)

Chart Created on Tradingview Platform

Speaking of the ECB decision, it is worth lifting our head up from the US docket focus to appreciate the broad event risk through the next 48 hours. There are also rate decisions from the Bank of England, Swiss National Bank and Mexican central bank. There are inflation indicators from the UK, capital spending figures from Japan, New Zealand GDP, Chinese November statistics and Australian employment. There is capacity for a broad base of volatility.

Top Macro Economic Event Risk for the Next 48 Hours

Calendar Created by John Kicklighter