Euro Q1 Fundamental Forecast

The European Central Bank (ECB) ramped up expectations of additional interest rate hikes next year at its latest monetary policy meeting, and if they are true to their word, then the Euro may outperform a host of other currencies in the first three months of 2023.

The ECB set out its stall at its latest policy meeting, clearly telling the market that rate hikes are here to stay as price pressures remain too high and they are expected to stay elevated for longer than previously thought.

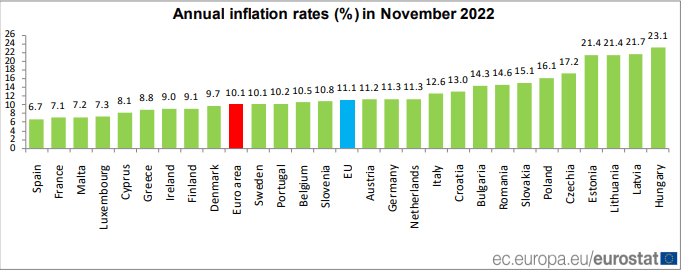

Annual Inflation Rate Comparisons

Source: Eurostats

‘The Governing Council decided to raise interest rates today, and expects to raise them significantly further, because inflation remains far too high and is projected to stay above the target for too long.’ The ‘significantly further’ comment suggests that the ECB will hike rates by 50 basis points at the next two meetings, at a minimum, with a third half-point hike already being priced into the market. In addition, President Christine Lagarde said that the central bank would start unwinding its bond portfolio - the asset purchase program (APP) – from the start of March at a rate of Euro15 billion a month until the end of Q2 when the subsequent pace will be reassessed.

While higher interest rates will help to quell annual inflation currently running at 10.1%, it will also increase borrowing costs across the Eurozone which will hamper growth prospects. The yield on the German 10-year Bund – the Eurozone’s de-facto benchmark – is now closing in on levels last seen over a decade ago. Whether the Eurozone economy is able to withstand ‘significantly’ higher borrowing costs is questionable.

Eurozone Borrowing Costs Moving Higher

Source: TradingView.com

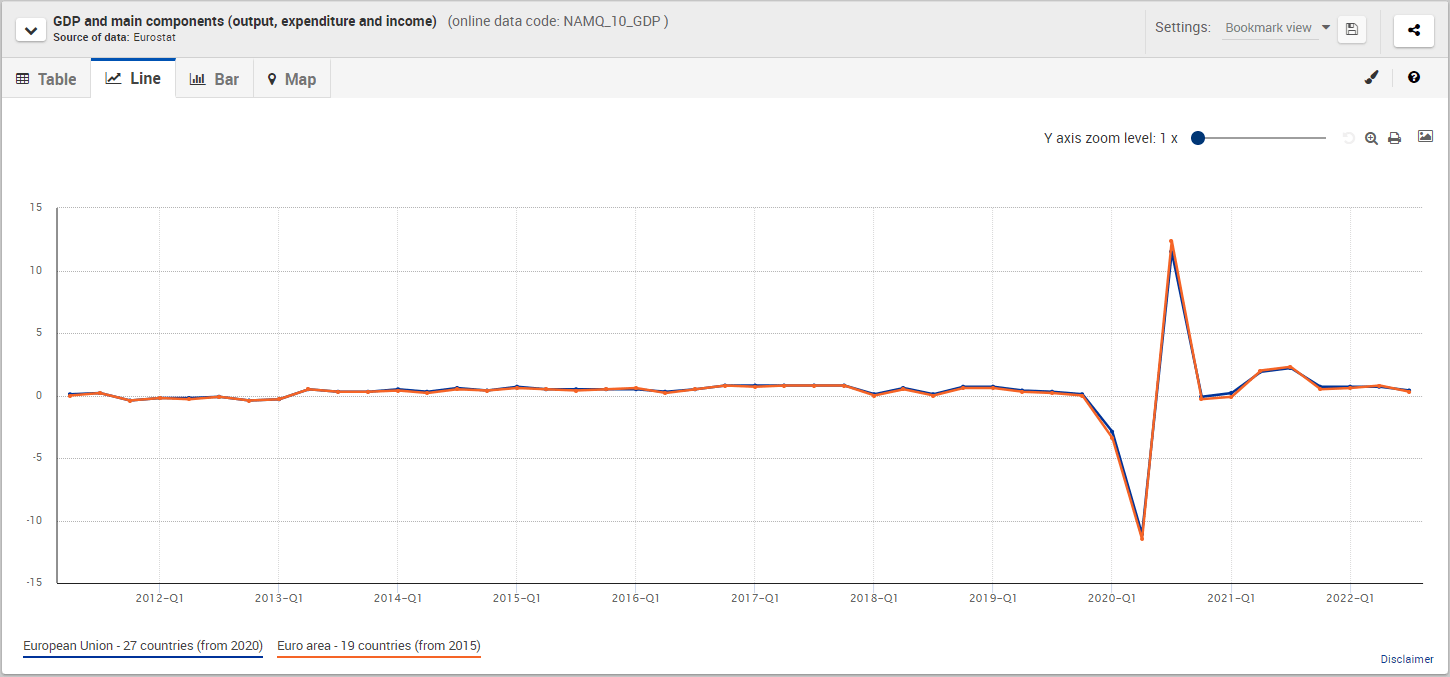

Eurozone growth has flatlined for much of the last decade, aside from the covid slump and pump, and higher borrowing costs are not going to help. The ECB’s new stance of doubling down on inflation will add fuel to the argument that the Eurozone is heading for a recession, and depending on who you listen to, this recession may not be shallow.

Eurozone GDP and Main Components

Source: Refinitiv

The ECB recently said that the Euro Area economy may contract in the current quarter and the next quarter although they expect a relatively ‘short-lived and shallow’ recession. The ECB sees the Eurozone economy growing by just 0.5% in 2023.

Whether the Eurozone economy can handle significantly higher rates next is debatable and may affect the Euro later next year if the ECB changes its path on policy. In the first quarter of 2023 however, higher rates and by default higher government bond yields will prop up the single currency. Indeed, the Euro may push further ahead, especially against a weak British Pound and against a US dollar that may be coming to the end of its own rate hike cycle. The days of EUR/USD trading below 1.000 looks to be over, for Q1 2023 at least.