USDJPY, BOJ Decision, S&P 500, Event Risk and EURUSD Talking Points:

- The Market Perspective: EURUSD Bearish Below 1.0550; GBPUSD Bearish Below 1.2100; S&P 500 Bullish Above 3,800

- The biggest fundamental event so far this week was the surprise tightening of monetary policy from the BOJ, but the news didn’t transmit throughout the ‘risk’ spectrum

- As we cross the halfway mark of the last full week of liquidity in 2022, the clock is ticking or the S&P 500 to extend its slide or for EURUSD to forge a break

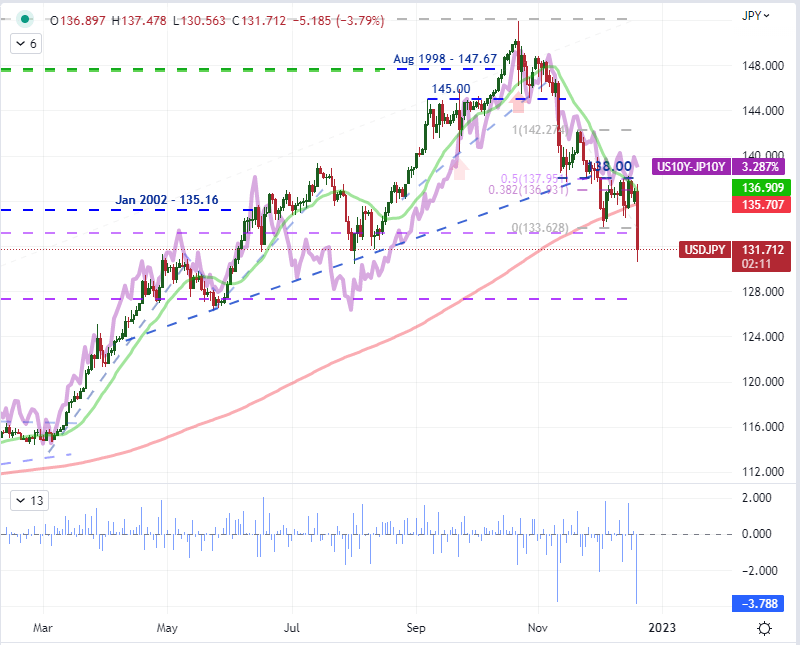

When it comes to generating volatility, there are two factors that tend to stage abrupt and dramatic market moves. The first is the scale of importance of the event or news that is released – or at least the suitability of the event to the asset in question. Second, consideration is how surprising the outcome in question. As far as that latter factor for the Bank of Japan’s unexpected policy tightening announcement this past session, it was clear there was little to no preparation for such an outcome from the market. The central bank announced a widening of its target band on the 10-year Japanese Government Bond (JGB) yield from +/- 0.25 percent out to +/- 0.50 percent.

The market wasn’t wholly unprepared because the possibility of even such a modest tightening move seemed impossible, it was simply a deeply held assumption after a relentless trajectory of easing. There was also very little messaging offered as to such a possibility which is highly unusual in this day and age. This was no rate hike or conventional policy move as far as western central banks have pursued in 2022, but it is normalization of an unorthodox and extremely dovish policy stance. The response from the Yen was incredible. USDJPY posted its biggest single-day loss (-3.8 percent) since October of 1998. Interestingly, the ‘surge’ in the Japanese 10-year yield was handily offset by the US equivalents ‘modest’ uptick. Can this trend sustain beyond the shock value?

| Change in | Longs | Shorts | OI |

| Daily | -2% | 2% | 0% |

| Weekly | 12% | -16% | -6% |

Chart of the USDJPY with 20 and 200-Day SMAs (Daily)

Chart Created on Tradingview Platform

As far as the ‘scale of importance’ aspect of the BOJ rate decision, seeing the most committed of the major central banks ease back from its extreme stance signals that the global fight against inflation is even more pressing than some may have expected. In FX circles, the Japanese currency has been the ‘funding currency’ for carry trade for three decades. To see their capitulation (modest as it may be) is to see the lower end of the range edge up. This adds to more macro considerations in the markets such as the central banks’ near constant reiterations that they will fight inflation even at the expense of market tantrums and mild economic contractions. If we were dealing with full liquidity market conditions, that message may have permeated wider.

Yet, with volumes starting to fade, we wouldn’t see the fallout from the Japanese Nikkei 225 spread much further beyond other major Asian benchmarks like the Shanghai Composite or Hang Seng Index. The S&P 500 put in for its smallest daily range since before last week’s fundamental fireworks and does so above some fairly prominent technical support. The overlapping Fibonacci levels of the October to November leg (50%), August to October leg (38.2%) and March 2020 to December 2021 leg (38.2%) all fall around 3,800. The path of least resistance is to hold that backdrop and return to a range. But some forthcoming data may make a go of the boundaries.

Chart of the S&P 500 with Volume, 100 and 200-Day SMAs, 5 to 20-day ATR Ratio (Daily)

Chart Created on Tradingview Platform

For the final 72 hours of this trading week – and arguably the twilight of the year – there is a breadth of event risk that can generate meaningful localized volatility, but few of these listings have the capacity to tap into the global market’s undercurrent. From a general market structure perspective, the upcoming session’s expiration of international money market assets (Eurodollar’s, FX futures, options, etc), there could be some repositioning that is amplified thanks to significant changes in monetary policy stances and the higher general pace of volatility in the FX market relative to other asset classes. More accessible for more traders though will be the event risk on tap. There is still an opportunity to tap the monetary policy volatility button with Friday’s PCE deflator, but that comes in the very last session before the Christmas weekend. Instead, it would seem that soft landing / recession speculation will be the more active node. Yet another ad hoc survey was released from Bloomberg this past session saying 70 percent of economists expect a US recession in 2023. More tangible insight will come from the economic docket ahead with the Conference Board’s consumer sentiment survey due for release. Overall, this survey has faired much better than the UofM reading, so any negative surprises here may exact more response.

Top Macro Economic Event Risk for the Next 72 Hours

Calendar Created by John Kicklighter

Looking for the capacity of movement given our backdrop conditions, appreciating the liquidity situation and the events that can provoke volatility is important. Yet, there is also the natural influence that comes revision to means. That is just the statistician’s way of saying ‘markets tend to normalize’. That can manifest in volatility moving to an average from extreme highs or lows. It can also see markets that have exhibited strong one-way movements to correct as positions are reduced. I continue to monitor the productive one-sided slide from the Greenback these past six weeks and the recent consolidation is growing more extreme. The 30-period historical range and ATR on the EURUSD (4 hour chart) below shows how remarkable the restrictions on activity. There is potential for a typical break from such a narrow band, but follow through will be heavily influenced by liquidity expectations. If there is any chance of follow through though, I would expect it to be more probably in the ‘path of least resistance’ which is for a move lower back into the past month’s range. The same is also true of pairs like GBPUSD and NZDUSD.

| Change in | Longs | Shorts | OI |

| Daily | -1% | -4% | -3% |

| Weekly | 4% | -10% | -5% |

Chart of the EURUSD with 20-Day SMA, 30 Period ATR and Historical Range (4 Hour)

Chart Created on Tradingview Platform