Talking Points:

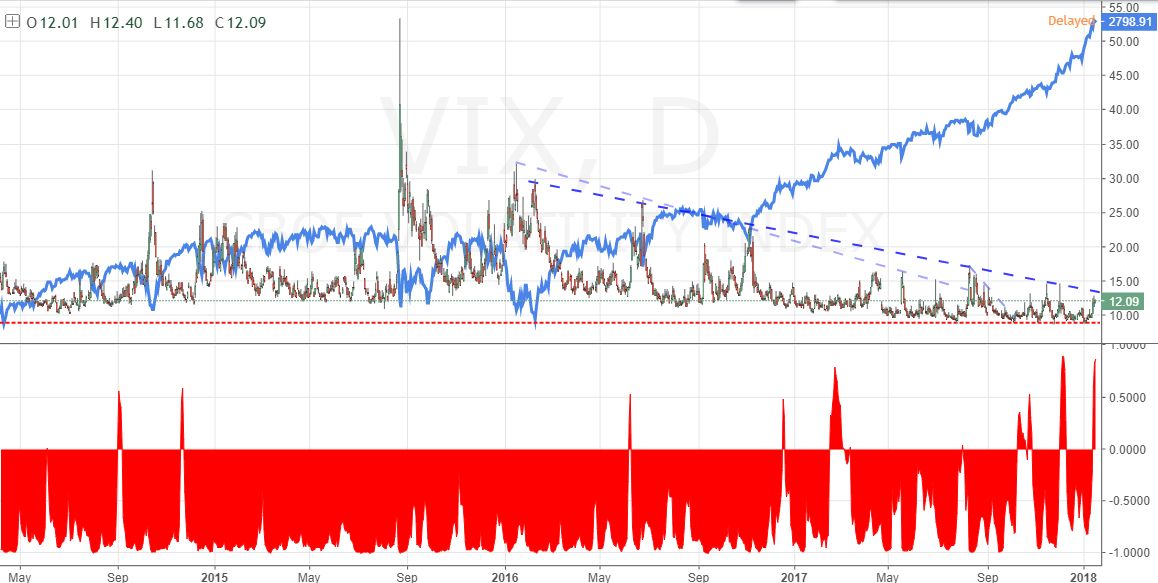

- The 10-day correlation between the S&P 500 and VIX has turned positive - a generally rare occurrence

- The 0.87 correlation coefficient reading between the two has only been higher four times in the past 20 years

- Extreme complacency, the rise of volatility products and years of ever-greater exposure has led to yet another abnormal signal

What is the 1Q fundamental and technical forecast for the US Dollar? Are DailyFX analysts interested in any Dollar-based exposure as top trades for 2018? Sign up for the 1Q forecast and Top Trades guides on the DailyFX Trading Guides page.

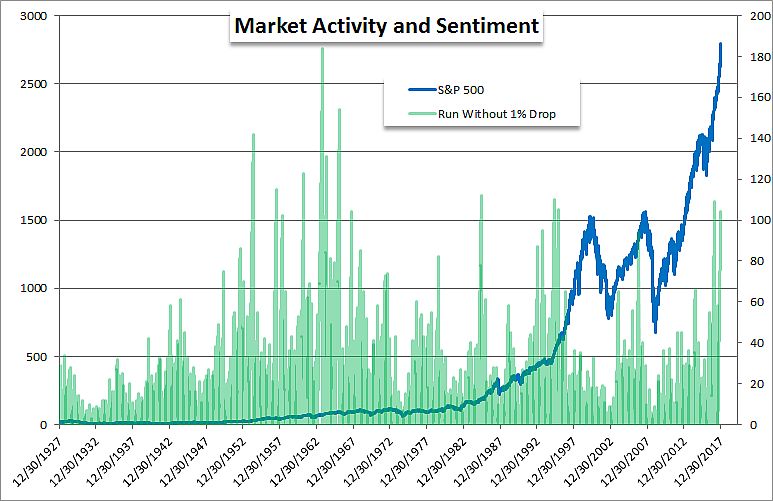

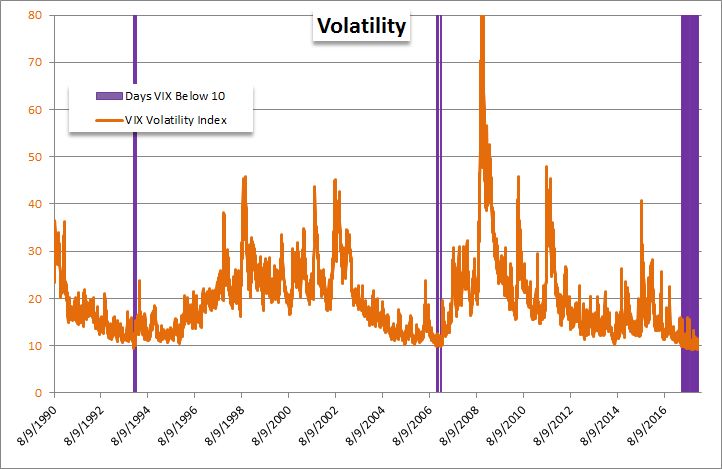

Historically, the benchmark US equity index the S&P 500 and the VIX volatility index move in opposing directions. In fact, they not only offer mirror performance to each other, they typically do so with the a matching intensity. In other words, if the stock market rises slowly, the VIX often deflates slowly. If the equities plummet, the volatility measure surges. That is what we refer to as a strong, negative correlation. It is very unusual when we see this relationship flip to a positive reading and rare that they move in robust concert. It seems we are facing one of those rare instances now. The natural contrary relationship between the market and volatility is natural to their use. Shares are the rudimentary portfolio's 'high return, high risk' option. The volatility index has been labeled the 'fear index' but it earned that title because of the correlation established well before the not-so-clever marketing. The volatility indicator is derived from options on the S&P 500 with a 30 day duration. While options are a speculative tool for many, they are traditional a hedge instrument for the underlying. Further, in pricing these insurance products, everything is known with the exception of the anticipated volatility of the underlying ahead. That is the implied volatility. As markets decline, fear of more rapid losses rise and the cost of the insurance escalates. When markets rise quietly, most deem protection unnecessary and the costs drop precipitously.

We can see the natural inverted relationship between S&P 500 and VIX with an overlay of charts, but the sheer intensity is best served by a statistical measurement. The correlation coefficient is a common tool for just this purpose. If you look at the 10-day rolling correlation, you quickly see that there is typically a reading between -0.8 and -1.0 which indicates a persistent, strong negative correlation. Yet, it is not always that way. Infrequently, we see the connection move into positive territory - usually amid a strong surge in volatility or charge in underlying shares. Yet, where we stand today is at a far greater extreme. The (positive) 0.87 reading is the highest positive reading we've seen since December 5th. That alone would make this seem far less consequential if not for the fact, that we don't have another comparable reading until all the way back to December 31st, 2003. In fact, in the past two decades, there are only four other times that we've seen this orientation at this intensity. That would clearly suggest something is amiss. But what?

It is tempting to say that this is a signal for something more ominous and formidable. Given the relentless climb in capital markets over the years and the skepticism that has grown out of the complacency, there is a natural interest in looking for signs that 'the end is near'. I personally believe that markets are oversaturated with risk and that there is far more to lose than gain in adding or even holding exposure. That said, picking tops is an effort fraught with too many false starts as rational analysis does not fit irrational risk chasing. Nevertheless, this relationship flip is remarkable. It reflects upon the over-indulgence in equities. It also reflects in the securitization of volatility products which has drawn fantastic interest from those that are hoping to find in abundance what they have so lacked through the market: meaningful movement to trade on. What has resulted is the same debase, short-term speculative stretch that you get in everything else. And, the fact that there is a zero bound in volatility doesn't seem to dissuade exceptional exposure. Why should we take note of this market relationship? How much of a proactive signal does it offer? Where and how should we trade should markets indeed heed the warning? We discuss all of that in today's Quick Take Video.

To receive John’s analysis directly via email, please SIGN UP HERE