Dollar, Fed, Inflation, SPDR S&P 500 ETF and EEM ETF Talking Points

- The S&P 500 eased back from its record high close Monday while the EEM emerging market ETF dove to a fresh 12-month low, but both are beholden to event risk ahead

- Though it is still more than a day away, the FOMC is casting a long shadow over the markets, cooling intent for speculative positioning until the group’s course is announced

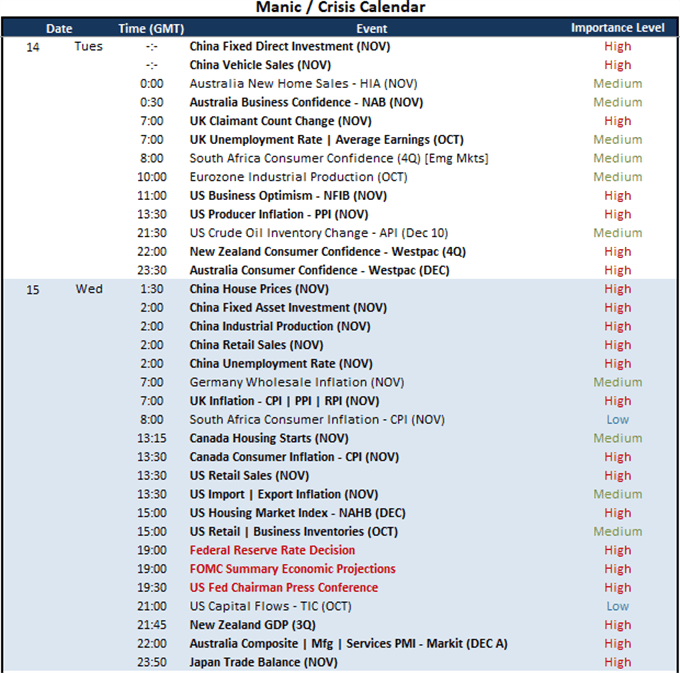

- While the Fed decision is the top event risk on tap, there are a number of high profile events ahead with critical technical patterns and Tennet-level liquidity conditions

Risk Appetite is Easing into Wednesday Fireworks, but the S&P 500’s Slip is a Check

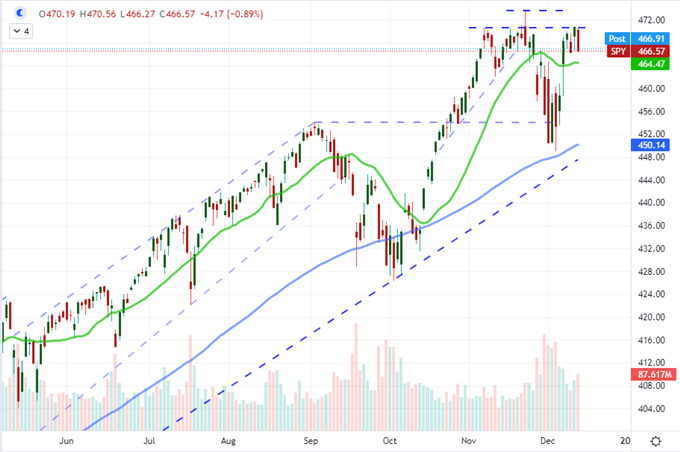

It is no secret that the market is finding its attention pulled decisively forward, awaiting confirmation from the Fed that it will accelerate its normalization effort to head off growing risks. That distraction alongside the unusual liquidity situation of seeing a flush of top-shelf scheduled event risk before two weeks of holiday-type trading conditions makes for quite the landscape to trade through. However, for the attentive and adaptive market participant, these are circumstances that can still be navigated. For a benchmark like the S&P 500, the pullback from a record high close this past session registers less as a reversal of conviction and more of a ‘path of least resistance’ pullback. It took more conviction that the market is not willing to back to forge fresh record highs than to spill off some of the bullish pressure – while noticeably still holding the floor of the recent range down to 4,665 (or the equivalent 465 on the SPDR ETF below). A further break lower would represent the most pre-FOMC excitement that I would expect possible, but anticipation is still working against momentum.

| Change in | Longs | Shorts | OI |

| Daily | 1% | -1% | 0% |

| Weekly | 15% | -13% | -1% |

Chart SPDR S&P 500 ETF with 20 and 100-Day SMAs with Volume (Daily)

Chart Created on Tradingview Platform

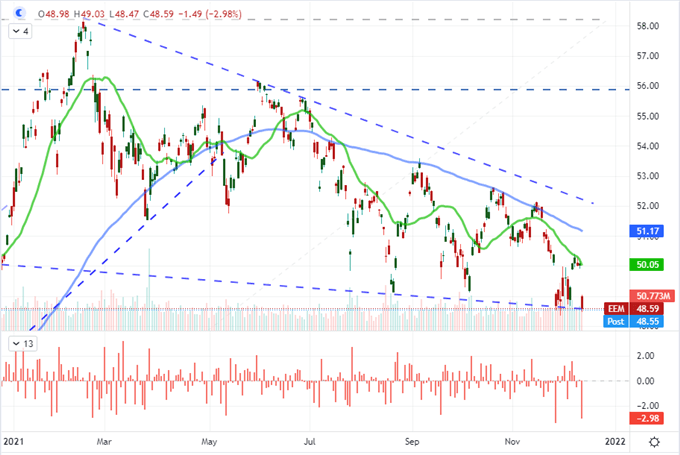

If you don’t happen to based your perspective of global risk appetite on a single – albeit very prominent – speculative measure, there seems to be a considerably more discount being applied to markets with a monetary policy sensitivity across the financial system. Global equities are -3 percent off their record highs according to the Vanguard World ETF (VT) and the Vanguard FTSE All World ex US ETF (VEU) is comfortably -6.5 percent below its June peak. Among assets more sensitive to yields, carry trade has generally flagged and junk bonds (HYG) are in the middle of their wide range of the past three months. The most remarkable measure of inflation and policy expectations though is probably the iShares MSCI Emerging Market ETF (EEM) which closed at its lowest level since November of last year. The local price pressures paired with the prospect of higher financing costs for loans from the developed world are clearly taking their toll.

Chart of EEM Emerging Market ETF with 50 and 100-Day SMA and 1-Day ROC (Daily)

Chart Created on Tradingview Platform

Seasonality for December, This Week and the Next 36 Hours

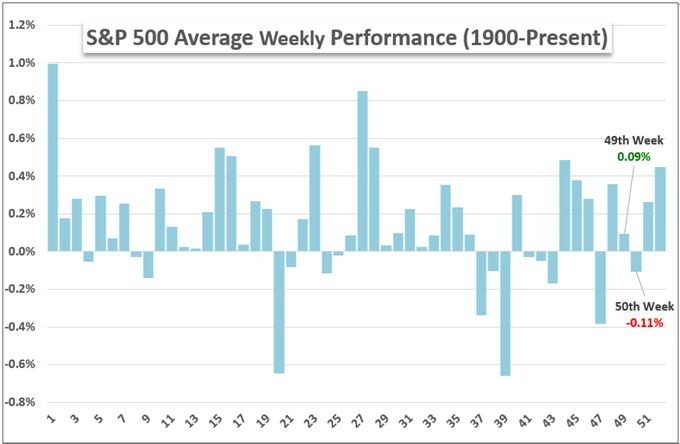

While I am watching the economic docket moving forward for its unique catalysts – along with the headlines for those matters that are not conveniently scheduled – I remain convinced that the most important feature of this market remains the uniquely transparent liquidity conditions moving forward. Through the month of December, we host the expectations of a steady slide in volume and volatility associated with holiday trading conditions weighted towards the end of the month as well as the subsequent risk appetite that is expected to follow such conditions. Through this particular week, seasonality suggests (via the S&P 500) that this is the only five-day stretch that has averaged a loss going back to 1900 – not a surprise given the run of data that comes out before market closers. And, far more specifically, the next 36 hours will be a reflection of the market’s anticipation for the Fed decision (due Wednesday at 19:00 GMT). Whether the market needs to adjust to expectations or is fully discounted, whether the market decides it is simply not important or is the decisive current, we will learn through the lead up and announcement.

S&P 500 Seasonal Weekly Performance

Chart Made by John Kicklighter with Data from Bloomberg

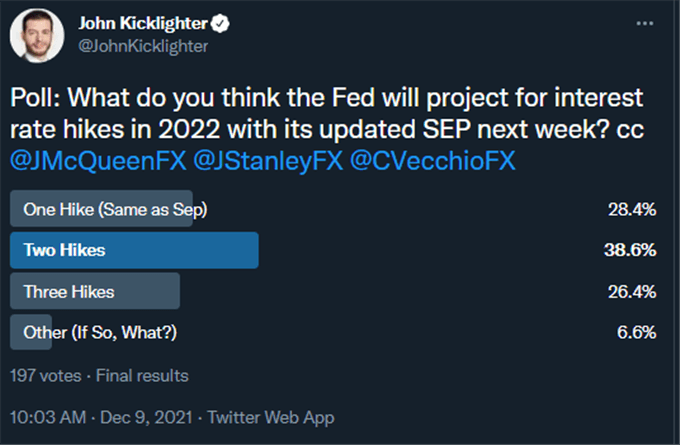

Speaking of expectations, I refer again to the poll I took last week in Twitter asking traders what they believe the Federal Reserve will announce in its Summary of Economic Projections (SEP). This was admittedly before the US consumer price index (CPI) data hit the wires, which may have resulted in an even more hawkish view among the masses. That said, the majority suspect two hikes specifically in 2022 which tends to match the projections we see priced into Fed Fund futures and swaps. Keep in mind what the expectations for the market are moving into the event. The central bank attempts to avoid surprises as much as possible, and that effectively deflates volatility. That said, I don’t think it is fully possible to come ‘exactly in line’ with expectations to the point of seeing a disinterested market.

Twitter Poll: What do You Think the FOMC’s Forecasts for 2022 Interest Rates Will Show

Poll from Twitter.com, @JohnKicklighter

The Dollar and the Data

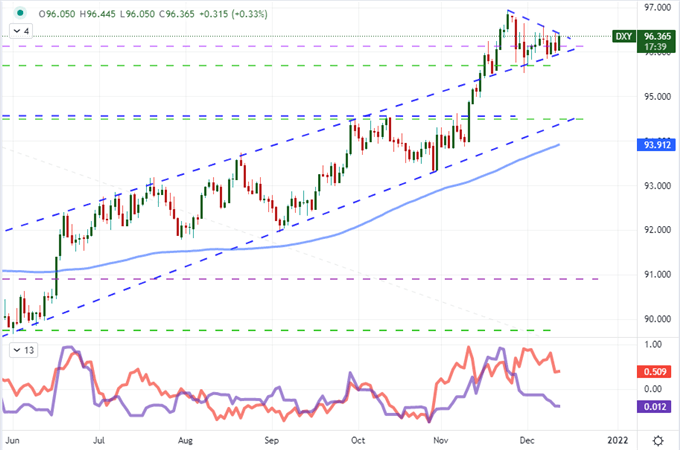

While the US indices and risk assets in general are a great litmus test for how the markets are assessing the situation around US and global monetary policy forecasts, I will be paying just as close attention to the US Dollar. The technical pattern says it all: pressure is building and speculators are looking for guidance on the next leg. It is possible that we get a ‘break of necessity’ before the Fed. This would insinuate that volatility has been overwhelmed by liquidity, but follow through is unlikely to show up before the critical vent. Remember, there is a carry consideration here which could benefit the Dollar for expected return (providing the FOMC does accelerate) but there is also an exposure as a yield forecast inflated asset that could suffer from general fallout of generally low return trades even if Chairman Powell in crew speed it up a little.

Chart of DXY with 100-Day Moving and 10-Day ATR and Historical Range (Daily)

Chart Created on Tradingview Platform

Not everything is about the Fed – though most of the market moving potential rests with the event or at least needs the allowance to come with it passing. If you are looking to the lead up through this coming session, I would not point to many data points that can reasonably stir localized market movement in this kind of environment. The upstream inflation figure from the US (PPI) and NFIB business sentiment report are likely to report on inflation concerns, but that is nothing new. Perhaps the UK employment statistics can rouse a little more attention given the Bank of England rate decision on Thursday is arguably more contentious than the Fed’s call the day before.

Calendar of Major Macro Economic Events

Calendar Made by John Kicklighter