EURUSD Talking Points:

- EURUSD offered both clear sign of volatility and lack of conviction following the ECB rate decision to hold its policy mix steady

- Dollar will take up the fundamental baton Friday as US 2Q GDP offers the capstone to a week of heavy growth reflection

- Despite a louder 'no-deal' Brexit voice, the Pound may steady while the Australian and Canadian Dollars retreat without design

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

The Dollar and US Equity Rally Finds Lift From Uneven Growth Readings

It is difficult to miss the appetite for US assets. Demand for the US Dollar has shown through the general bull trend of the previous year while a particular bid arose through just the past week. In contrast to the favorite safe haven's advance, the benchmark US indices have similarly projected recovery throughout 2019 and forged fresh record highs through the close of this past week for the S&P 500 and Nasdaq. That is a familiar trend for those that have been monitoring the pace-setter for speculative appetite, but so too should be the contrast this particular segment of the market is drawing to so many other 'risk-based' markets like global equities, emerging markets, global yields, carry trade and more. This is not a simple measure of 'risk on' or 'risk off' but instead a specific appeal for US-based markets.

Chart of S&P 500 to VEU Rest of World ETF Ratio (Daily)

There are a few elements that could reasonably be contributing to a Dollar and Dow bid, but one of the most prominent was on display this past week: relative economic out-performance. It started with the IMF's updated growth forecasts for 2019 which showed a down-tick (-0.1 ppt to 3.2 percent) for the world yet an increase (0.3 ppt to 1.6 percent) for the US in particular. That trend carried forward with the US Composite PMI for July from Markit showing a jump where the Japanese figure languished in contractionary territory (below 50.0) and the Eurozone reading lost traction. Finally, on Friday, the US BEA 2Q GDP reading beat expectations of a 1.8 percent pace with a 2.2 percent post. While there wasn't any global contrast to work with, the market was happy to follow the line.

As a theme, the general health of the global economy will continue to draw attention. For big-picture government data, the 2Q Eurozone (along with French and Italian) GDP updates are due this week. That will clearly be a charge for European shares and perhaps the Euro, but it can also generate some further traction for the Dollar if the data drives capital towards or away from the world's second largest currency. Unless there is an extreme contrast, the favorable winds for the US from growth are likely to die down. This shift in attention may generate some traction for the Euro in general, but EURUSD is likely to find its bearings from other, more pressing means.

Equally-Weighted Euro Index (Daily)

President Trump Reminds That Trade Wars are Still a Severe Burden

Though growth was an effective driver, the hum of trade wars continued to buzz in the fundamental backdrop this past week. The headlines were reserved to reports that US and Chinese officials were meeting once again or overt threats being made between US and European officials over subsidies for their respective airplane manufacturers or lingering threats of auto tariffs. That changed into the close on Friday. US President Donald Trump waited until after the market close Friday to remark that China may not agree to a trade war agreement until after the election hoping for a change in administration. This may be as much a Trump Administration campaign tactic as an earnest evaluation of China's position; but either way, that would equate to a severe economic burden. We'll have to see how market's account for evaluation - if they do at all - come next week.

Another insight from the President that should be accounted for in our estimation of risk going forward is his take on currencies. In a wide-ranging talk, he would once again say the Yuan was 'very low' and manipulated while the Euro was 'not doing well'. The insinuation was that the Dollar was unfairly forced higher by deflated counterparts, but he made the effort to say he supported a 'strong Dollar' policy. Despite these particular remarks, Trump has repeatedly bemoaned the high Greenback and lambasted the Fed for indirectly keeping it propped up - he made effort to critique the central bank Friday saying the GDP beat happened despite the "anchor around wrapped around our neck". What was most interesting were reports that trade adviser Peter Navarro had presented means for devaluing the Dollar in the Oval Office this past week but was rejected. The best way to further destabilized a market already knocked off balance by a trade war is to introduce a currency war.

Chart of Equally-Weighted Dollar Index with Consecutive Candle Count (Daily)

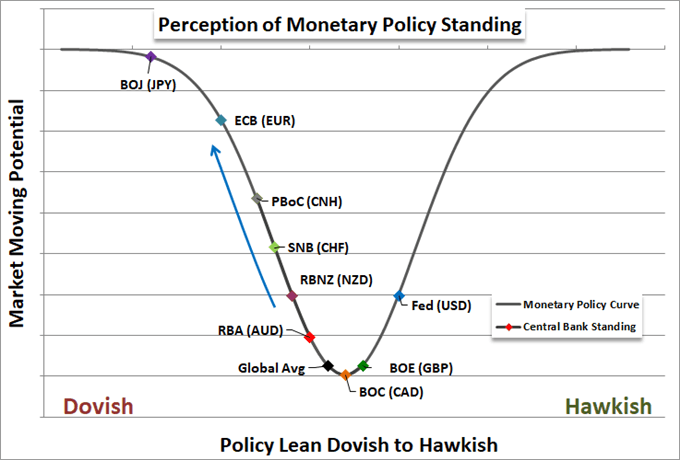

Fed Rate Decision Top Event Risk - As Much for Global Markets as the US

Looking ahead to next week, trade wars may find unexpected winds and GDP will produce swells in areas with less global systemic heft, but monetary policy will line up for a systemic impact with three rate decisions on tap. Following this past week's European Central Bank (ECB) rate decision, the market is keeping close tabs on dovish nuance - the group signaled an intent to ease through rates and/or quantitative methods in upcoming meetings. The Bank of Japan (BOJ) is first up on Tuesday morning and they will almost certainly maintain a position at the extreme end of the dovish scale, which only furthers their loss of credibility but doesn't exactly alter the course of the Yen. The Bank of England's (BOE) meeting on Thursday is dubbed 'Super Thursday' as it includes the quarterly inflation report. As important as that may be for insight on economic forecasts, the central bank is unlikely to alter course until the Brexit situation is clear - a resolution some ways into the future.

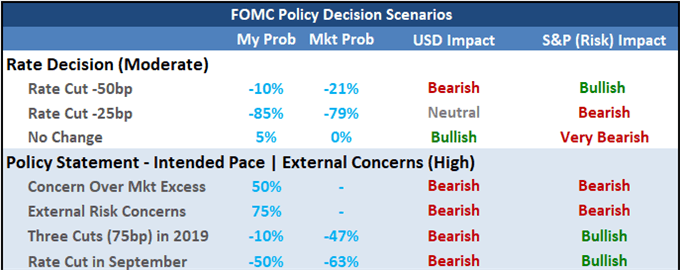

Top central bank insight and event overall is the Wednesday's Federal Open Market Committee (FOMC) meeting. This gathering is expected result in the first rate cut from the world's largest central bank in over a decade. There is certainty of 'at least' a 25 basis point cut at this meeting, but the real point of interest is whether the group feels it necessary to lower the range 50 basis points and/or signal further easing through the end of the year. According to Fed Funds futures, the probability of a half percent cut is 21 percent. The probability that the Fed goes for at least three cuts through year end is set at a 51 percent probability. There is no favorable outcome in this when we think it through. If the Fed bends to speculative will with faster cuts, it will suggest the situation for the market and economy is desperate. If they move slowly, there will be clear disappointment that the pace is well below what was anticipated.

FOMC Scenario Table

Also on the Top Watch List: Gold; Pound and Australian Dollar

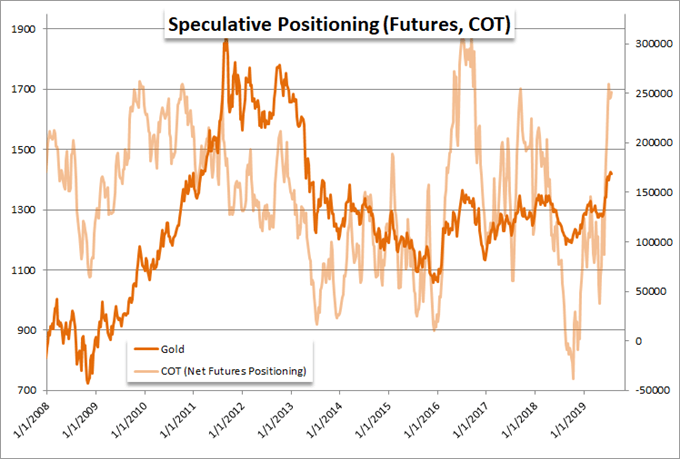

Looking outside the systemic themes, there are a few other key markets I will be watching for independent market movement. Gold is perhaps the most important measure overall. While it carries its own virtues and vices as a vehicle, my interests are more aligned to its use as a signal. The particular safe haven is well suited for an anti-fiat appetite that sent its value soaring in 2008-2011 when easing lead to an surge in stimulus. Accommodation is to be expected, but policy influx that accompanies an appetite for safe havens would speak to a financial backdrop that is extremely fragile - or already collapsing.

Chart of Gold with Net Speculative Futures Positioning (Weekly)

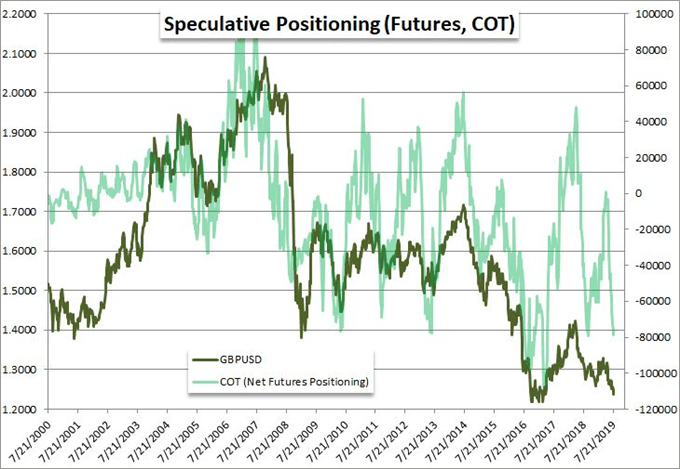

The Sterling is another market of material interest. The currency may not have the weight of the Dollar against this week's fundamental backdrop or the Euro after this past week's ECB rate decision, but anticipation and speculative positioning may very well leverage a skew that resolves to useful moderation. The BOE decision is unlikely to detract from Brexit fears, and the UK-EU divorce is already seen heading towards a messy split. New PM Johnson has reiterated his willingness to pursue a no-deal Brexit, but there is still three months left until time runs out. In the meantime, Parliament can cause problems and a General Election is a meaningful risk. I am watching to see if the added time and extensive speculative lean against the Pound will lead to rebalancing over the week ahead.

Chart of GBPUSD with Net Speculative Futures Positioning (Weekly)

Finally, there is the Australian Dollar. While I see merits to the Swiss Franc and New Zealand Dollar, the Australian currency is one of the more interesting options for reduced fundamental static. There is 2Q inflation data due out of the country this coming week, but the currency is already in a technically vulnerable position. AUDUSD slid six straight sessions through Friday. That isn't record breaking but it does line up to the most persistent tumbles in a few years. A rebound would be well primed on a medium and short-term technical basis. But it is always useful to look for a fundamental cue along the way to help the market along. We disuss all of this in this weekend Trading Video.

Chart of AUDUSD and Consecutive Candles (Daily)

If you want to download my Manic-Crisis calendar, you can find the updated file here.

See how retail traders are positioning in EURUSD, Dow, Gold and other key FX markets, indices and commodities using the DailyFX speculative positioning data on the sentiment page.