Talking Points:

- Apple earnings impress, will this leading company's performance bolster FAANG or even broader risk trends?

- How far will a dovish BoJ pressure the Yen, what is the trend potential from the Euro and Loonie after their data runs?

- Top event risk for Wednesday is the FOMC rate decision but market bias and probable scenarios shape a controlled impact

Do you want to learn how to trade event risk? Download the strategy guide on for trading news events on the DailyFX Trading Guides page.

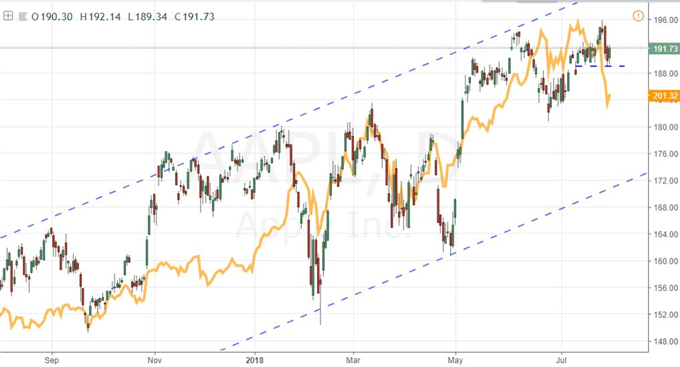

Can Apple Earnings Do Some Heavy Lifting for Sentiment?

We have seen sentiment behind risk trends steadily deteriorate over the past few weeks. Well before the waver is US indices, the discrepancy in risk-leaning assets signaled a loss of traction behind broader investor sentiment. In other words, it wasn't the enthusiasm of the crowds driving market participants to seek out additional yield despite the risks and the tepid promise for tangible returns. Yet, worry started to genuinely slip in with the disappointing showing from the market-leading FANG group's earnings. This collective of top market cap tech stocks (Facebook, Amazon, Netflix, Google) has led the tech sector over the past few years, which in turn has led US indices, that are in turn the best performing of the major speculative asset groups that I follow for market-wide sentiment back to the start of the recovery following the Great Financial Crisis. While the Amazon and Google earnings were generally positive, the weigh of the Netflix and Facebook misses clearly unnerved investors. That said, the unofficial second 'A' in FAANG (Apple) has reported figures that can rouse enthusiasm. Announcing after the bell Tuesday, the world's largest company by market cap beat forecasts on EPS ($2.34 versus $2.18) and revenue ($53.27 billion versus $52.3 billion). If we were looking for a reason to stabilize, this could be it. However, if risk falters despite this showing, it will only serve to magnify the troubles for sentiment.

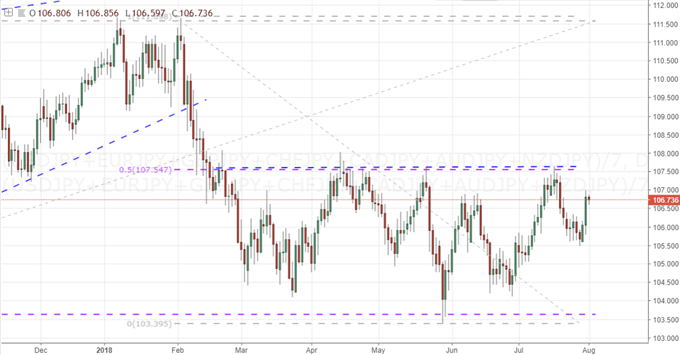

A BoJ Rate Decision that Sinks the Yen, Data Run the Leaves Euro Listless

Earnings weren't the only fundamental theme running this past session. There was a remarkable amount of high profile macro economic event risk on the docket. In the otherwise dense listing of top events, the Bank of Japan's (BoJ) rate decision was one of the top listings. This was less owing to the actual potential of the event, but the hearty speculation heading into it. Following a report referencing unnamed sources last week suggesting the central bank was looking to make adjustments to its policy program that could be construed as tightening, Yen traders were on high alert. What the market registered was not the outlook for rate hikes that we've found this past year from the ECB, but something far more subtle. The BoJ lowered its inflation forecast and said it was adapting its approach moderately to allow for yield fluctuation and to allow it to reduce asset purchases (ETFs for shares) should it deem it time in the future. If we judge harshly, this is status quo which the Yen doesn't have much adjusting to match. Charitably, it actually is a modest adaptation but not enough to support a lasting Yen rally. I think we will quickly revert to the currency's 'safe haven' correlation. For the Euro's run of Eurozone 2Q GDP, consumer inflation and employment data; the data was similarly of an in-line nature. That said, the growth figure was a modest miss (0.3 versus 0.4 percent) while the jobless rate and inflation figure improved slightly. There isn't enough here to charge the Euro which will now set this currency to drift until a broad theme takes control.

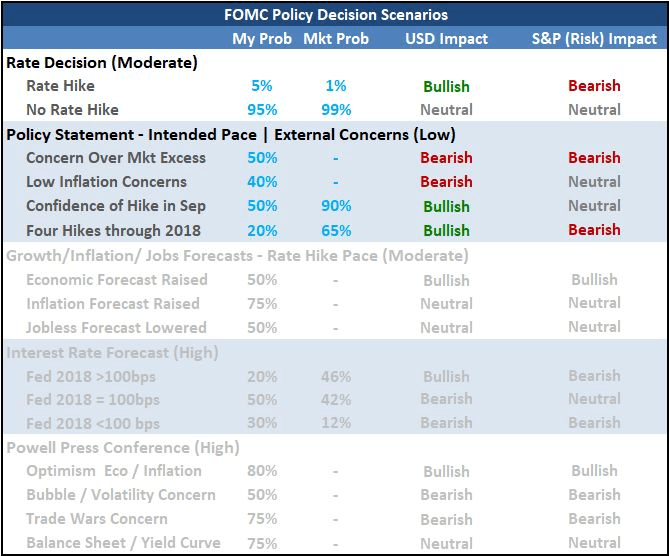

Dollar in a Position for a Break but the Fed Decision is Not an Effective Trigger

Looking out over the next 24 hours, the docket is again loaded with meaningful releases - though there are notably fewer top tier updates than what we had to deal with this past session. Ranking the known event risk, the most threatening (or opportunity-laden depending on your perspective) is the FOMC rate decision. The probability of a hike at this meeting is remarkably clear according to swaps pricing - there is a near-certain 98 percent chance of no change. The group's forward guidance has clearly shaped the market's expectations. Of course, speculation adapts to the environment; and dollar, yield and capital market traders know to look at the nuance in the accompanying monetary policy statement for clues to the bearings moving forward. There is still a heavy speculation for a rate hike in September and a fourth hike for the year by December. There will influence from this meeting one way or the other, but it is unlikely to result in a definitive move for the Greenback. Range-based options for the currency in the interim will be better suited to the general conditions and a shift of focus to the open-ended themes (trade wars) and more volatile event risk (NFPs) will carry greater speculative weight.

Canadian Dollar, Mexican Peso and Oil Prices Slip Their Fundamental Gears

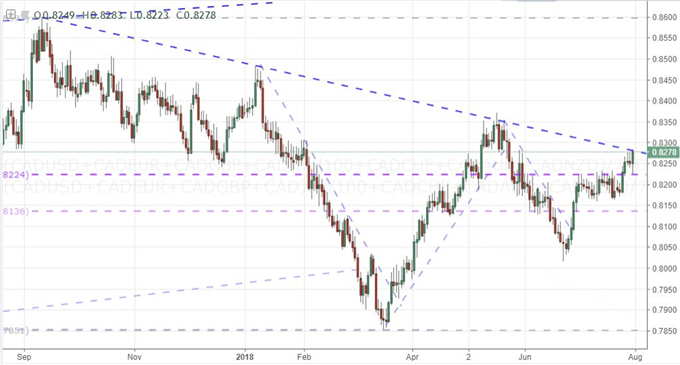

It should come as little surprise in these markets that fundamental themes - no matter how systemic or concentrated - are struggling to forge sustainable trends. This divorce from traditional motivation is perhaps more familiar in some other corners of the market, which in turn lowers aversion to the range and technical-based conditions that outperform in such conditions. For the Canadian dollar, the monthly GDP update this past session offered tangible improvement and resulted in a hefty boost for the currency. However, as the equally-weighted CAD index nears its critical resistance; the ongoing uncertainty over crosswinds like the trouble in US trade negotiations threaten meaningful progress. Have options for scenarios where the CAD advances despite its uncertainties (like USDCAD) as well as those that are well positioned for a retracement (like NZDCAD and CADCHF). Speaking of US trade, Mexico reportedly is making headway in discussions with the United States which removes considerable uncertainty from the county's shoulders, but the weak 2Q GDP showing is deflates the speculative anticipation. Then there is crude oil. The commodity dove through Tuesday; but as intense as the decline was, the day's volatility fell well within the larger trend channel. With inventory figures tomorrow, anticipation for volatility is high; but the potential for genuine trend should be set appropriately low. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.