Talking Points:

- The S&P 500 closed out its smallest weakly range since 1979 while the VIX further slid below 10 despite North Korea fears

- GBPUSD held back a range of fundamental tides from Fed upgrade to UK downgrade to Prime Minister May's speech on Brexit

- Dollar, Euro, Pound and Yen reflect a mix of key fundamental theme - mon pol, risk, etc - and heavy complacency

How have retail traders changed their positioning in EURUSD, the Dollar-based majors and US equity indexes following the Fed rate decision? Visit our DailyFX Sentiment page to find out.

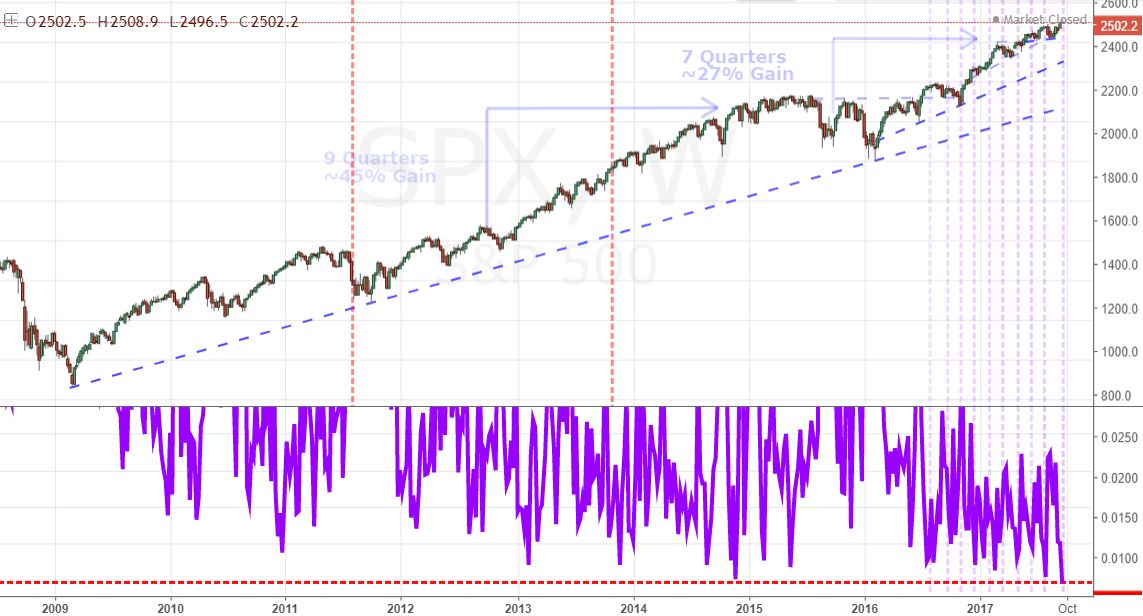

That familiar yet hollow sense of complacency held out for the markets this past weeks. As a benchmark for risk exposure, the S&P 500 slipped a little; but volume was anemic, capital flows remained unsupportive and the week's range was the smallest since 1979. Complimenting this sense of uneasy quiet, the VIX volatility index continued its retreat with a close well below the extreme baseline at 10. The sense of willful disregard this reflects looks increasingly extraordinary in the face of situational (such as the Fed decision), seasonal (September and October are peak volatility months) and structural circumstances (value at record lows while dependency on no volatility at equivalent highs). It is entirely possible that the market's maintain this tenuous calm for weeks or months, but traders need to ask themselves whether it is worthwhile to pursue exposure that depends on such unbalanced conditions. Progress will increasingly prove a struggle and gains tepid, while the risk of a panicked deleveraging will grow. Personally, that is not my cup of tea.

Through the FX market, there is just as much fundamental tumult contrasting a remarkably placid price structure. Following the Federal Reserve's commitment to selling assets off its balance sheet next month and confidence in a third 2017 rate hike later this year, the Dollar has gained virtually no altitude. A laundry list of Fed officials' speeches (including Chairwoman Yellen), consumer sentiment data and the central bank's preferred inflation reading (PCE deflator) will try its hand at reviving the Greenback's charge. From its major counterpart, the Euro, robust Eurozone PMI figures reinforced the rising tide of confidence in the region's economic recovery. The focus ahead will likely follow more systemic and speculative themes with the Germany election over the weekend and ECB President Draghi due to speak a few times. The British Pound is another major that will test its fundamental motivations. This past week ended with the dramatic combination of UK Prime Minister Theresa May's speech on Brexit and Moody's unexpected downgrade of the country's sovereign credit rating. GBPUSD (and other Pound crosses) dropped in the aftermath of both, but critical technical levels still stand. The start of the fourth round of Brexit negotiations and BoE Governor Carney's prepared speeches may start the ball rolling.

Where the core majors are holding fast in the face of systemic developments, the liquid currencies one tier lower are proving more responsive to less global event risk. That can translate into trade opportunities as well. The Australian Dollar's dive following the RBA Governor's remarks about policy limitations have started the crosses down a speculative path. The Canadian Dollar has slowly retreat with rate speculation softening among inflation data and policy talk. It will be the New Zealand Dollar's turn this week with the RBNZ rate decision on tap. Swaps market expect nothing at this meeting, but as we've seen; forward speculation can provide more than enough drive to compensate. Outside of traditional currencies, Bitcoin held up better against a second warning issued by JPMorgan CEO Jamie Dimon over the future of the cryptocurrency market. In contrast, the traditional 'alternative currency' gold closed out a second painful week. We what does the coming week hold for risks and opportunities? That is the focus of the weekend Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE