Gold Price Forecast Overview:

- Despite sizeable price swings in global equities and FX markets, gold prices continue to consolidate below their yearly high.

- Gold volatility’s relationship with gold prices has started to normalize, which should be supportive of higher gold prices.

- According to the IG Client Sentiment Index, gold prices may soon breakout higher.

Gold Prices Prove Steady on Sturdy Fundamental Moorings

Revolving concerns that the global economy may not be ready to emerge from the veil of The Great Lockdown have proven instrumental to keeping gold prices afloat over the past several weeks. Despite very encouraging May US retail sales figures, alarming headlines out of China – Beijing is closing all schools as the coronavirus has spread anew – and data suggesting that positive test case rates and hospitalizations rates are increasing in the United States have kneecapped risk appetite.

The backdrop of increasing macro uncertainty caters to one of the talking points from the Federal Reserve’s June policy meeting last week, which was that interest rates would be staying at current levels for the foreseeable future, perhaps through 2022. Fresh signs that the global economy’s two largest economies, the United States and China, are not ready to re-open and begin the path to normalcy has provoked another reach for safe havens.

WHY DO ‘REAL YIELDS’ MATTER TO GOLD PRICES?

The shifts in US Treasury yields following the June Fed meeting speak directly to one of the most important fundamental underpinnings of precious metals’ rallies: environments that produce falling real yields tend to be the most bullish. On the other hand, environments that produce rising real yields tend to be the most bearish for precious metals.

Real yields are inflation-adjusted yields: in this case, the US Treasury 10-year yield minus the headline inflation rate. Why does this matter? Investing is all about asset allocation and risk-adjusted returns. On the asset allocation side, it’s about achieving required returns given the investor’s wants and needs.

If inflation expectations are rapidly increasing, you would expect to see fixed income underperform: the returns are fixed, after all. Why would you want to have a fixed return when prices are increasing? On a real basis, your returns would be lower than otherwise intended.

Rising US real yields means that the spread between Treasury yields and inflation rates isincreasing. If precious metals yield nothing (no dividends, coupons, or cash flows), they would be ill-suited to hold when US real yields rose. And vice-versa: falling US real yields tend to be supportive of higher gold prices.

Gold Volatility Continues to Drop, However

Gold prices have a relationship with volatility unlike other asset classes, even including precious metals like silver which have more significant economic uses. While other asset classes like bonds and stocks don’t like increased volatility – signaling greater uncertainty around cash flows, dividends, coupon payments, etc. – gold tends to benefit during periods of higher volatility.

Heightened uncertainty in financial markets due to increasing macroeconomic tensions increases the safe haven appeal of gold. But with signs that the US economy is rebounding faster than anticipated (V-shaped recovery, anyone?) and the Federal Reserve intent on keeping the liquidity spigot open for the foreseeable future, the winds of an inflationary US economic environment are starting to blow through financial markets.

Read more: How Do Politics and Central Banks Impact FX Markets?

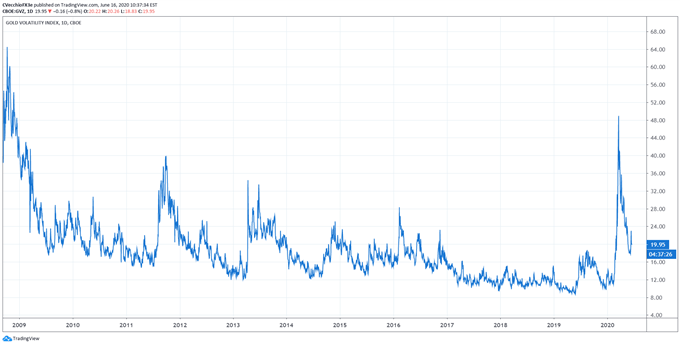

GVZ (Gold Volatility) Technical Analysis: Daily Price Chart (October 2008 to June 2020) (Chart 1)

Gold volatility (as measured by the Cboe’s gold volatility ETF, GVZ, which tracks the 1-month implied volatility of gold as derived from the GLD option chain) is trading at 19.95, still less than 25% of the absolute high set in mid-March near 85.50. We still maintain the belief that, given the current environment, falling gold volatility is not necessarily a negative development for gold prices, whereas rising gold volatility has almost always proved bullish.

As such, the 5-day correlation between GVZ and gold prices is 0.15 while the 20-day correlation is 0.06; one week ago, on June 9, the 5-day correlation was 0.14 and the 20-day correlation was -0.78; and one month ago, on May 19, the 5-day correlation was -0.78 and the 20-day correlation was -0.42. The recalibration of the 20-day correlation suggests that the traditional positive relationship between gold prices and gold volatility is beginning to normalize.

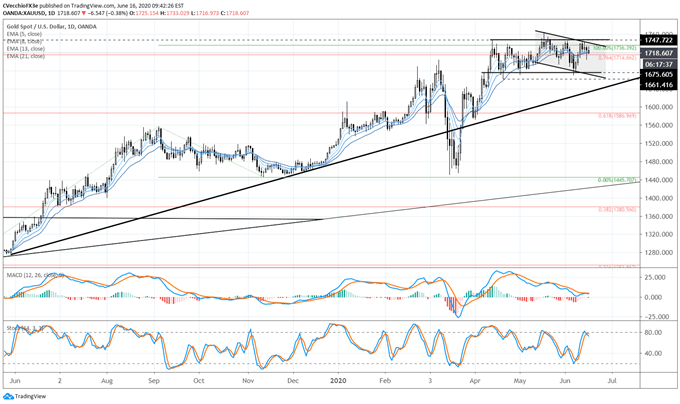

Gold Price Technical Analysis: Daily Chart (June 2019 to June 2020) (Chart 2)

On May 18, gold prices were able to climb to a fresh yearly high, following through on the prior Friday’s breakout from the sideways range carved out between the April 14/2020 high at 1747.72 and the April 21 swing low at 1661.42. This was expected, as we noted ahead of the breakout that “given that gold prices rallied into this consolidation, the market retains an upside bias.”

It still holds that gold price action remains in a sideways consolidation; contextually, having rallied into this consolidation, gold prices would still retain an upside bias. The measured move, derived from the high/low range between 1675 and 1748, calls for a move towards 1821 should resistance break.

Failure to achieve a topside breakout through 1748, and instead produce failure below 1675, would give gold price action the hallmark of a topping pattern, insofar as the measured move lower would be targeting 1602.

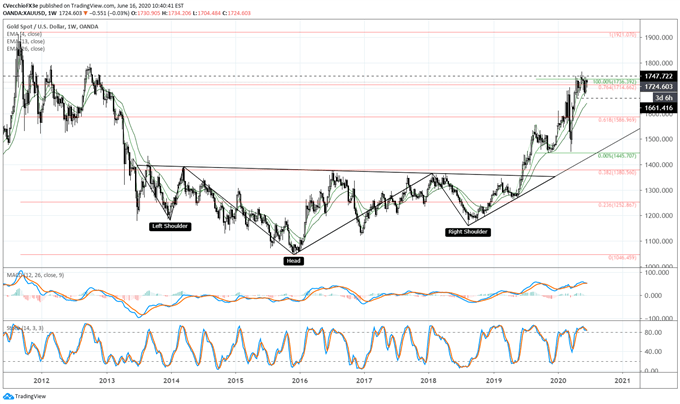

Gold Price Technical Analysis: Weekly Chart – Inverse Head and Shoulders Pattern (June 2011 to June 2020) (Chart 3)

Gold prices have made significant progress within the confines of the multi-year inverse head & shoulders pattern, achieving their highest level since November 2012 earlier this week. It thus still holds that the rally into and through the 76.4% retracement (1714.66) must be viewed in context of the longer-term technical picture: the gold price inverse head and shoulders pattern that was triggered in mid-2019 is still valid and guiding gold price action.

Depending upon the placement of the neckline, the final upside targets in a potential long-term gold price rally, if drawing the neckline breakout against the August 2013 high at 1433.61, calls for a final target at 1820.99. This dovetails neatly with the measured move on the daily timeframe looking for gold prices to rally into 1834.02.

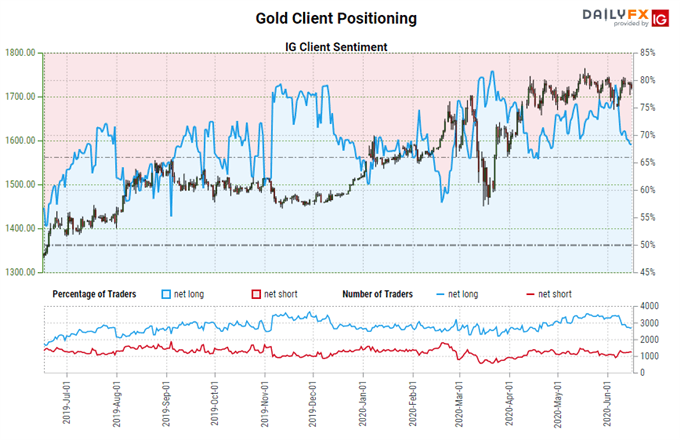

IG Client Sentiment Index: Gold Price Forecast (June 16, 2020) (Chart 4)

Gold: Retail trader data shows 68.01% of traders are net-long with the ratio of traders long to short at 2.13 to 1. The number of traders net-long is 2.22% lower than yesterday and 21.43% lower from last week, while the number of traders net-short is 1.10% lower than yesterday and 2.85% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests Gold prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current Gold price trend may soon reverse higher despite the fact traders remain net-long.

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist