GBP Talking Points:

- UK GDP grew by 0.3% in May, above expectations of just 0.1%, and April 3-month GDP is revised higher potentially avoiding contraction in Q2

- Despite a small push for Sterling, both EURGBP and GBPUSD are nearing levels last seen in January 2019 when GBP was at year lows

- Manufacturing and industrial production manage to grow slightly in May but global trade wars and slowing growth continue to weigh on the industry

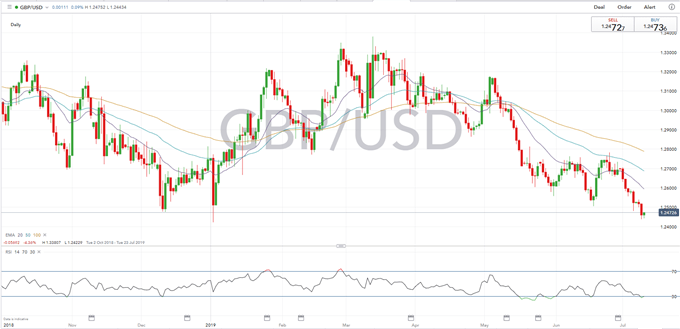

Sterling faced some sell off pressure in the opening of the European session as investors awaited key manufacturing and growth figures to be released. GBPUSD is nearing year-lows as continued political uncertainty keeps sterling in a downward spiral. The pair is currently trading around 1.2455, close to its 1.2422 dip experience in January 2019, its lowest level since the aftermath of the Brexit referendum. The pair then managed to correct higher as monthly GDP figures showed that the UK economy managed to correct previous losses and grew 0.3% in May, above expectations.

EURGBP followed suit with an initial push higher for the pair which was later corrected on the release of the data. The pair is currently trading around 0.8999, its highest level since January 11.

PRICE CHART: GBPUSD DAILY TIME FRAME (OCT 2018 – JULY 2019)

UK GDP grew 0.3% in May, above expectations of just a 0.1% growth, and the April 3M/3M figure has been revised upwards from an initial contraction of 0.3% to a growth of 0.4%, which was partly due to the unwinding of stockpiling on the back of the Brexit deadline being pushed back. The upward revision could mean that the economy could have avoided a contraction in the second quarter of the year, which was initially feared, with growth for the first half of the year running below potential, and fears of a possible recession increasing. Inflation dropped slightly in May, but it remains close to its target of 2%, easing the pressure to increase rates and falling closer in line with the dovish tone from most of the other Central Banks. Key focus will be on next week’s CPI figures as a further drop in inflation could increase the likelihood of a rate cut in the next MPC meeting.

Manufacturing and industrial production figures for the month of May continue to show the struggles manufacturers are facing on the back of slowing growth and trade wars. YoY manufacturing production in May showed no growth has been experienced from this time last year as expectations were for a 1% growth. Monthly manufacturing showed that the industry managed to pick up in the last month, with a change of 1.4% from the previous month, when it experienced a drop of 4.2%, but the figure was still below expectations of 2.2%. Industrial production showed slight growth both in the monthly and yearly figure, but they were both still below expectations. This data comes after manufacturing PMIs for the month of June came in at 43.1, much lower than expectations of 49.3, as client confidence is dampened by heightened economic and political uncertainty.

Economic landscapes in a “sea of change”

Bank of England Governor Mark Carney warned investors last week that global economies face a shock as global trade tensions have shifted market expectations towards interest rate cuts by most central banks. His comments led to an increase in bets that the BoE will cut rates by the end of the year as markets price in the need for more monetary stimulus.

Industry experts have warned that the British economy is facing its slowest growth since the 2008 recession, falling behind other G7 countries. The uncertainty surrounding the Brexit outcome continues to drag on investment as the deadline was pushed back from March to October. The extension of the exit date has meant that companies and households have been on “preparation” mode for almost a year now, pushing back consumption and spending until the uncertainty dissipates, which is damaging the economy.

Not only is lacklustre data dragging down on sterling, as the race to become the next tory leader and prime minister only adds to the concern. The current political landscape seems to be more about who is the toughest candidate to stand up to the European Union to achieve a new deal or follow through with a no-deal harsh Brexit, which markets still consider to be the worst possible outcome. Rather than working towards building up consumers’ confidence in the future of the British economy by finding possible ways to dissipate the fallout from the UK’s divorce from the European Union, both candidates seem to be tied up in a game of trying to prove who is the biggest “macho” out of the two, which is not going to help in reviving investment.

Recommended Reading

Eurozone Debt Crisis: How to Trade Future Disasters – Martin Essex, MSTA, Analyst and Editor

KEY TRADING RESOURCES:

- Just getting started? See our beginners’ guide for FX traders

- Having trouble with your strategy? Here’s the #1 mistake that traders make

- See our Q3 forecasts to learn what will drive FX the through the quarter.

--- Written by Daniela Sabin Hathorn, Junior Analyst

To contact Daniela, email her at Daniela.Sabin@ig.com

Follow Daniela on Twitter @HathornSabin