The Bank of England (BoE) started the cycle of tightening monetary policy by hiking the UK Base Rate by 15 basis points to 0.25%, the first-rate hike in over three years, at the last Monetary Policy Committee (MPC) meeting of 2021. And additional rate hikes are already penciled in by economists for 2022 as UK inflation hits extreme levels last seen over 10-years ago.

The BoE hiked interest rates in December by 15 basis points to 0.25%, despite the ongoing surge in new Covid-19 cases. Many in the market had pushed back this rate hike until the next meeting in February 2022 on fears that the UK government may introduce harsh lockdown measures at a time when the UK economy is finally pulling out of the pandemic crisis of the last two years. The announcement of a new, virulent Covid-19 variant, Omicron in late November took the market by surprise and dampened any prevailing rate hike expectations. However, it seems like the BoE has chosen to look through these fears and have chosen to concentrate on official UK labour and inflation data instead.

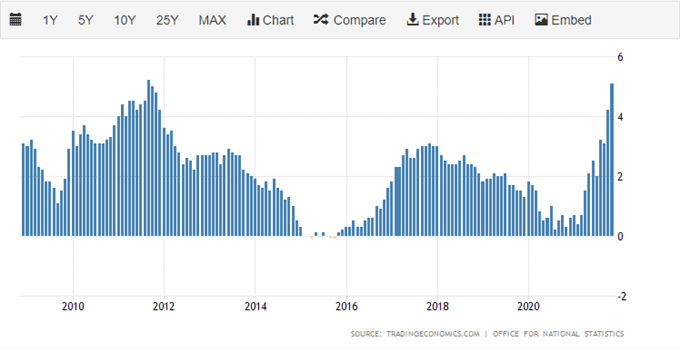

UK headline inflation is now running at 5.1% on an annualized basis, the highest level since September 2011, according to the November Office for National Statistics report, as the cost of goods in the inflation basket surge.

UK headline inflation (Nov), Office for National Statistics

Source: TradingEconomics.com/Office for National Statics

The current level of UK inflation is more than double the Bank of England’s target rate of 2% and with higher inflation expected over the next few months, the BoE has been forced to act to get ahead of the situation.

The UK Labour market is also robust with the employment rate rising to 75.5%, while the unemployment rate has fallen to 4.2%. In another sign that inflation may become a longer-term problem, from August to October 2021, annual growth in average total pay including bonuses rose to 4.9%. The tight conditions seen in the UK labour market over the last few months was expected to loosen when the UK furlough scheme ended in September but this has not been the case and the jobs market remains very tight.

It is against this backdrop that the BoE decided to hike rates and with both inflation expected to remain high, and the labour market to remain tight, the UK central bank will have to hike rates again in the coming quarters. It is likely that the BoE will hike the base rate by 25 basis points at its February 2 meeting with further hikes possible in March or May and beyond. This backdrop will underpin Sterling against a range of currencies, especially the Euro and the Japanese Yen, as the interest rate differential between these low yielding currencies and Sterling widens. Sterling hit a multi-month low of 1.3160 against the US dollar recently and this is likely to be the low for some time with the US not expected to lift rates until mid-2022. With the Bank of England now firmly on a path of tightening monetary policy, Sterling-pairs have room to move higher over the next three months.