Talking Points:

- A series of Central Bank rate decisions have taken place over the past day, and the Federal Reserve kicked rates-higher for only the third time in the past ten years.

- Despite that rate hike out of the U.S., the Federal Reserve provided enough dovish innuendo around the move to elicit weakness in the U.S. Dollar.

- If you’re looking for trading ideas, check out our Trading Guides. And if you’re looking for ideas that are more short-term in nature, please check out our Speculative Sentiment Index (SSI) Indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Fed hikes, but stays cautious and keeps rate outlook unchanged: ‘Dovish Hike’

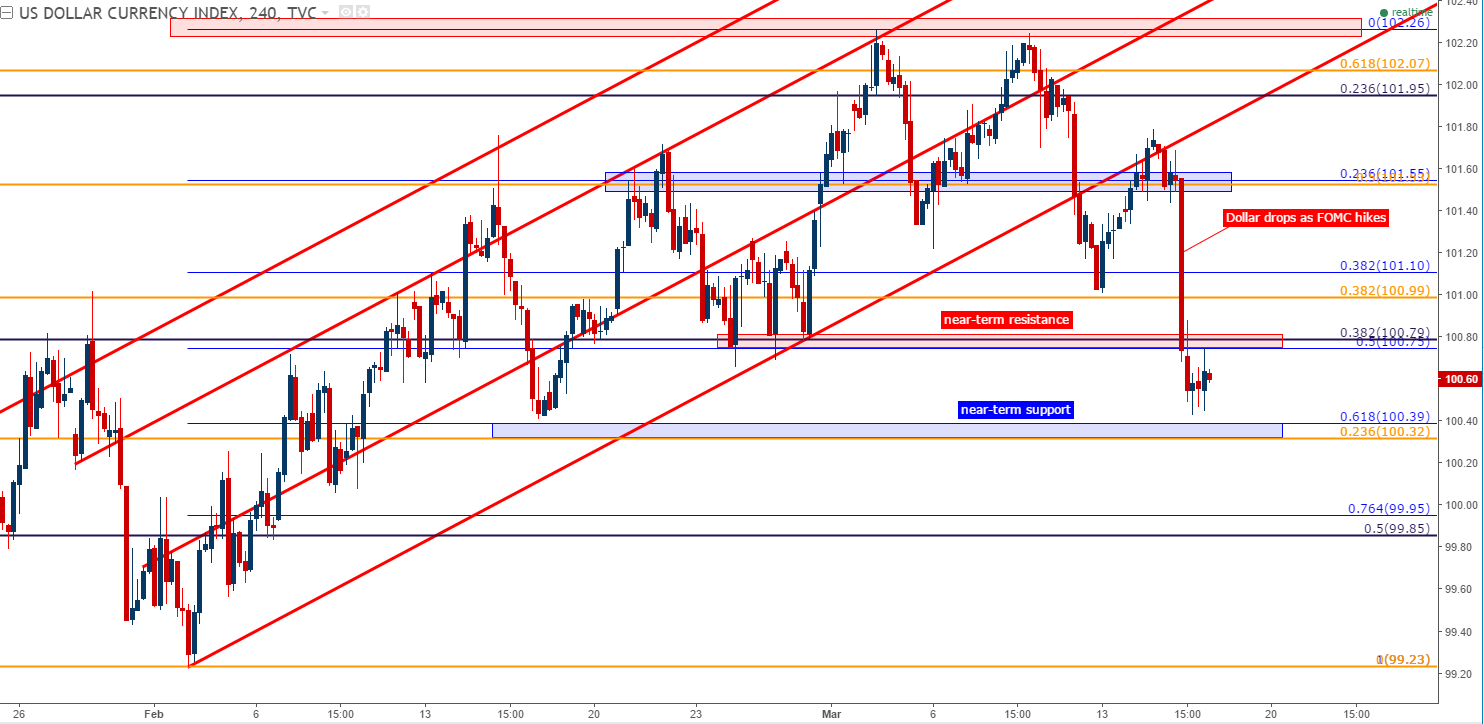

Well, we finally got that non-December rate hike that markets have been looking for. The Federal Reserve posed only the third interest rate hike since 2006 at yesterday’s rate decision; and while the previous two hikes saw equity markets in some form of tumult around the move, yesterday’s has seemed to go through rather smooth, at least thus far. Stocks didn’t crater, the Dollar didn’t jump-higher and for all intents and purposes, most major markets have escaped unscathed despite the very slight tightening in U.S. rate policy.

Given the reaction to the data, it appears as though the ‘pain factor’ for markets would be more aggressive rate hikes (or expectations) from the Fed. Taken from the fact that we had an actual adjustment to rates, but the U.S. Dollar put in a rather-brisk drop while U.S. stock prices shot-higher, this would deductively highlight the fact that markets were cautiously walking into yesterday’s meeting with the presumption that the Fed may increase their expectations for rate hikes over the next couple of years.

This, of course, did not happen, as the Federal Reserve posed a ‘dovish rate hike’ at yesterday’s meeting. On the below chart, we’re looking at the U.S. Dollar after yesterday’s rate hike.

Chart prepared by James Stanley

BoJ Holds

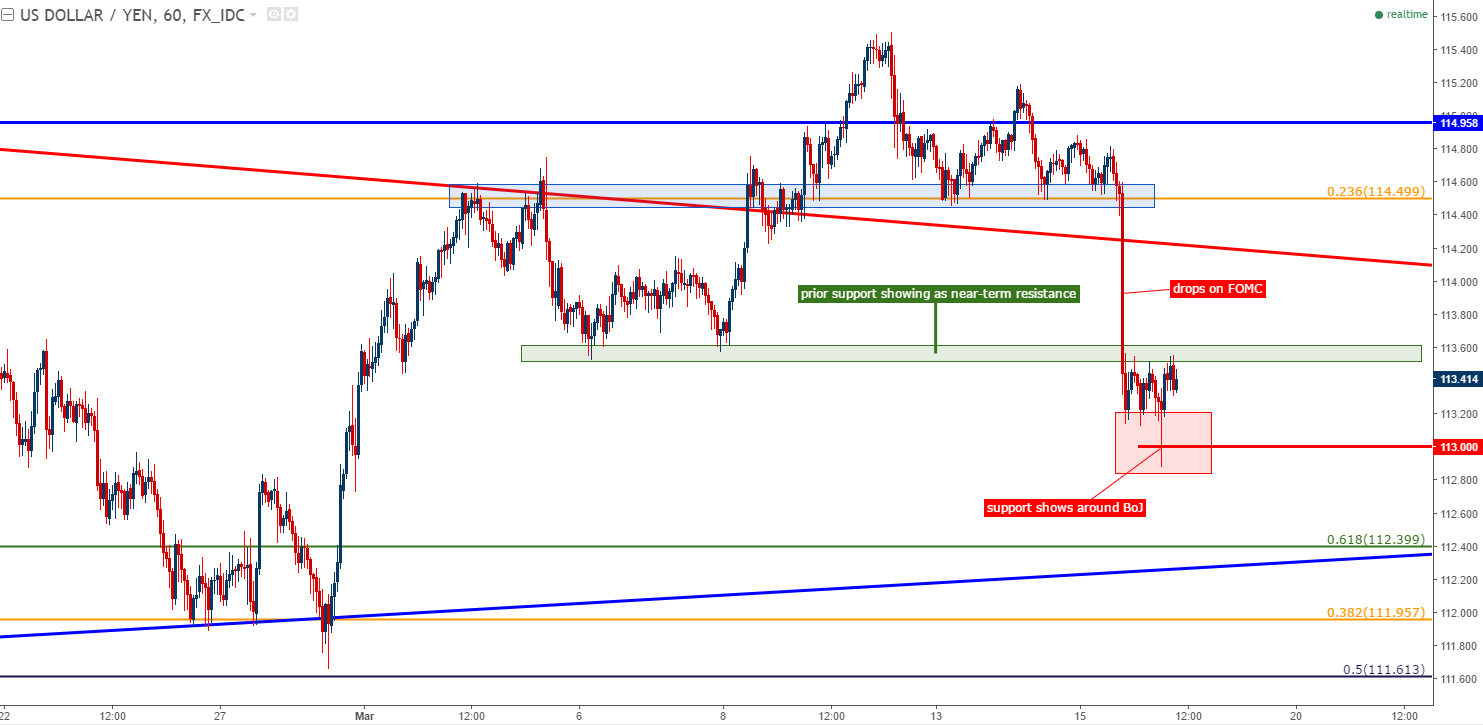

After the Fed’s rate hike yesterday we also heard from the Bank of Japan. There really wasn’t much to hear here as the BoJ appeared as though they just wanted to get through this ‘rate decision’ with a minimum of impact. The BoJ continued to denote that the Japanese economy is on a moderate recovery trend; but strength was lacking to investigate any rate hikes or tightening of policy options. One interesting tidbit was that the BoJ has identified U.S. monetary policy as a risk factor for global markets. So this highlights that the BoJ remains ultra-cautious, and is not quite ready to begin slowing accommodation.

USD/JPY had put in an aggressively-bearish move before the BoJ ever spoke; but as the BoJ rate decision came into markets, support appeared to set around the ¥113.00 handle. But sellers haven’t yet given up, as resistance has shown-up right around old support in the vicinity of ¥113.50.

On the hourly chart of USD/JPY below, we’re looking at these short-term support and resistance levels showing around ¥113.00 and ¥113.50. For those looking to push a top-side approach, they’d likely want to let prices first trade beyond this near-term resistance zone to highlight that bulls may be able to take control and reverse this near-term trend of weakness before looking to take-on exposure.

Chart prepared by James Stanley

The Swiss National Bank Holds, Warns of Inflation, Threatens Intervention

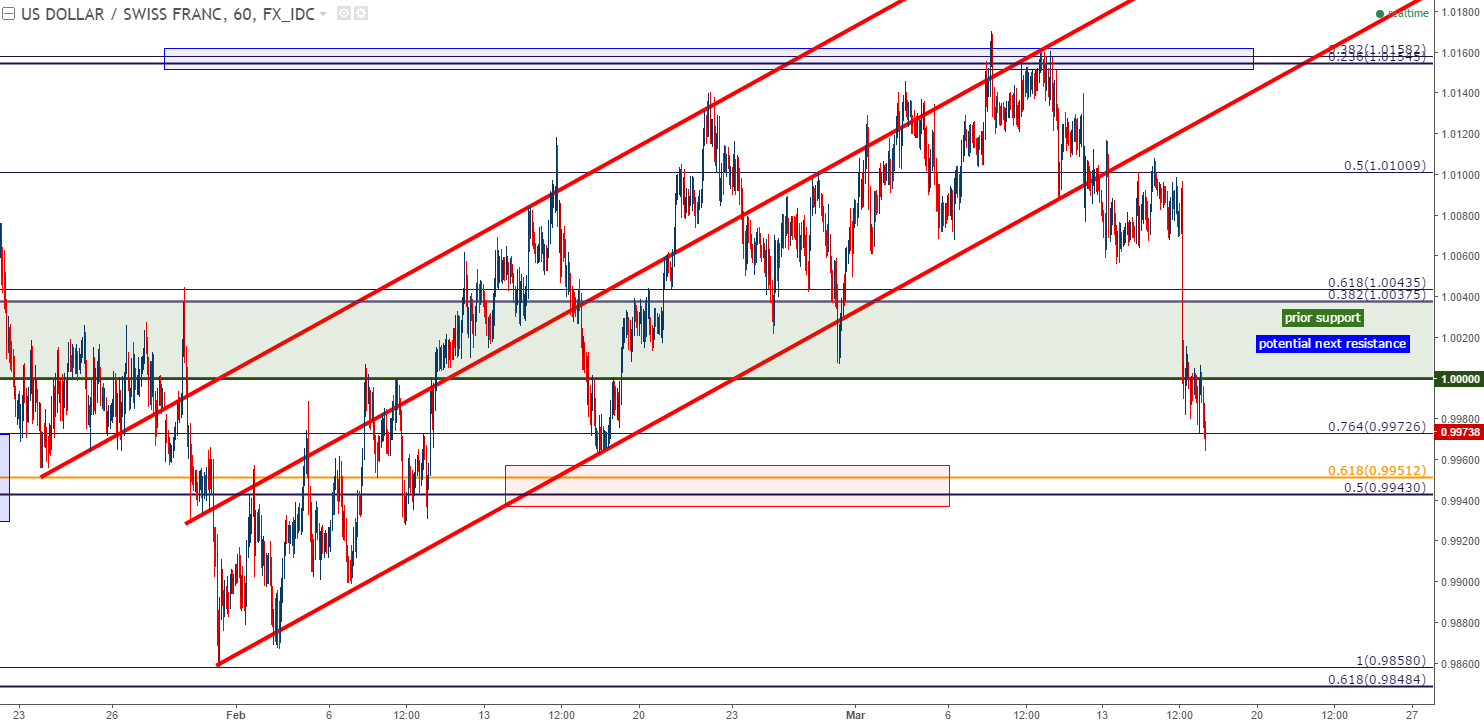

The Swiss National Bank held rates at -.75% at this morning’s rate decision, but SNB President Thomas Jordan seemed quite unpleased with the Swiss Franc’s strength, saying that the currency is significantly overvalued. The bank pledged to execute more FX interventions if need-be to siphon off that Franc-strength.

The net result of this morning’s meeting was even-more Franc-strength. USD/CHF continued its descent that started around yesterday’s Fed meeting, and price action in the pair is now below the vaulted level of ‘parity’.

We had looked at this support level yesterday in our technical article on USD/CHF, and the fact that price action broke through this zone so quickly highlights the fact that the pair may have bearish-continuation potential.

Chart prepared by James Stanley

Bank of England Holds, Warns of Inflation

The Bank of England voted to hold rates flat with an 8-1 vote at this morning’s rate decision. The sole dissenter was Kristin Forbes, who voted for a rate hike.

The BoE acknowledged the elephant in the room for the British economy: rising inflation and the potential for even more given the ‘sharp repricing’ in the value of the British Pound following the dovish campaign from the BoE in response to Brexit. The key phrase from the meeting minutes was pretty telling:

‘With inflation rising sharply, and only mixed evidence on slowing activity domestically, some members noted that it would take relatively little further upside news on the prospects for activity or inflation for them to consider that a more immediate reduction in policy support might be warranted.’

This comes after a months-long saga for the bank in which they’ve wrestled with the prospect of inflation. Ahead of the Brexit referendum, BoE Governor, Mark Carney, warned that decision to leave the E.U. would entail a ‘sharp repricing’ in the value of the British Pound, which could bring on higher rates of inflation, higher rates of unemployment and slower growth. But after the U.K. elected to leave the E.U. in June of last year, Mark Carney didn’t wait around for signs of weakness as he hosted an impromptu press conference just days after the referendum to warn that accommodation from the BoE was coming. This gave another shot of weakness to the British Pound as investors now had the idea that the Bank of England was going to try to proactively-offset economic risks of Brexit with uber-loose monetary policy.

In August, this was delivered in the form of a massive bond buying program, bringing further weakness to Sterling. This eventually led to the ‘flash crash’ in the currency in early-October as there was a dearth of demand for GBP. But in November, the BoE began to acknowledge these stronger inflationary forces, and this finally brought some life back into the currency. But at the bank’s Super Thursday in February, a wrench was throw into that equation when the BoE made the puzzling move of increasing growth forecasts for 2017 by 42% (expecting GDP growth of 2% versus the prior expectation of 1.4%); but at the same time they downgraded forecasts for inflation.

At this point, the British Pound continues to trade in a range near a long-term zone of support around the 1.2000-psychological level. The Bank of England has continued to be extremely dovish, even in the face of rising inflationary forces. This morning’s rate decision highlights that certain members within the MPC may be warming to the idea of slowing-down that dovish accommodation in response to rising inflation; but for any definitive message from the Bank we’re likely going to be waiting for the next Super Thursday event with updated Inflation projections, to be hosted on May 12th.

Chart prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX