Talking Points:

- This morning saw the release of British inflation figures for the month of November, and both headline and core CPI printed above-expectations; but still well-below the BoE’s 2% target.

- Despite the fact that inflation continues below the BoE’s target, the British Pound has been one of the strongest currencies in the world over the past month and a half, and that includes a U.S. Dollar that put in a near-historic move during the month of November.

- If you’re looking for trading ideas, check out our Trading Guides.

To receive James Stanley’s Analysis directly via email, please sign up here.

Earlier this morning, November inflation numbers out of the U.K. were announced with both headline and core inflation figures coming-in above expectations. Headline CPI for the month of November printed at an annualized 1.2% figure versus expectations of 1.1% while Core CPI came in at 1.4% versus the expectation of 1.3%. And while these numbers are still both well-below the Bank of England’s inflation target of 2%, the fact that higher prices are already showing-up after the ‘sharp repricing’ in the British Pound in October exposes the fact that inflationary forces may be gathering momentum in the British economy.

Which brings up a widely-contested issue: What moves currency prices? Can it all be boiled down to just inflation and employment prints? Or perhaps just a Central Bank’s feelings for what they might be doing in the future? No – prices are driven by supply and demand. Now, supply and demand may be impacted by any of the above forces, along with a litany of others; but regardless of the reason or motivations, if there are more buyers than sellers in a market, prices are probably going to go up and if there are more sellers than buyers, prices are probably going to go down.

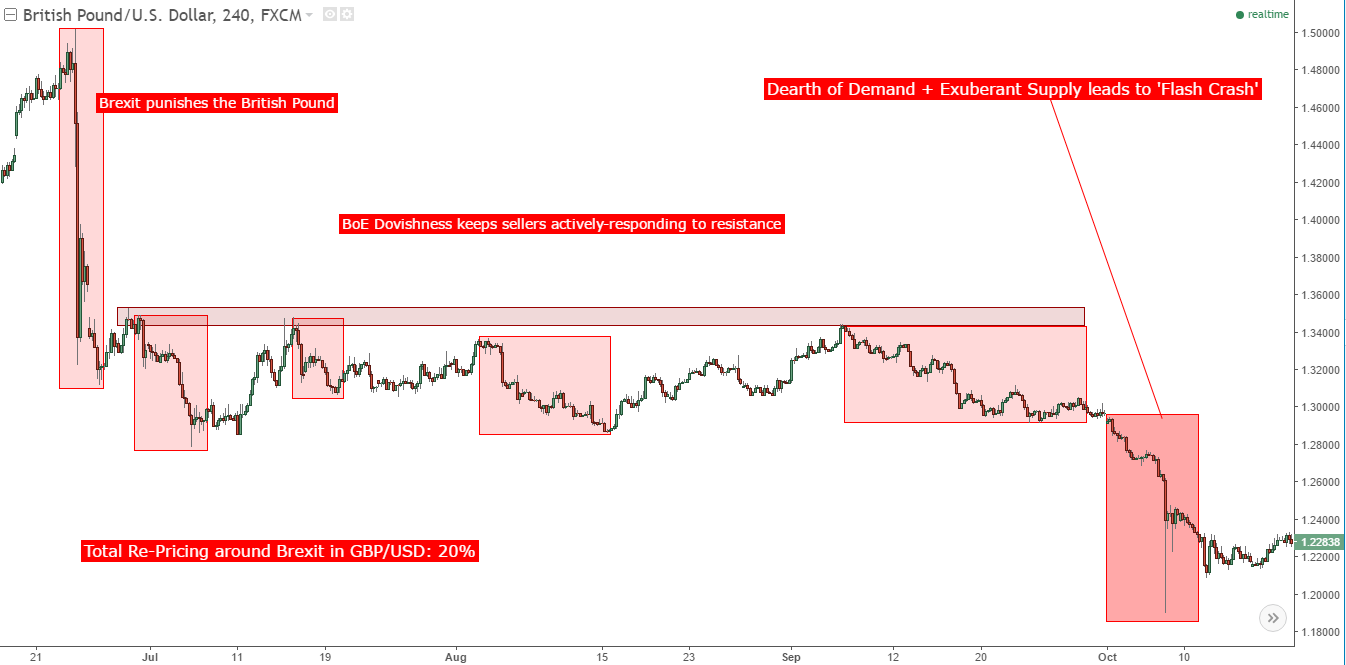

In the British Pound, there was an absolute dearth of demand around the Brexit referendum. After all, the world had never seen an economy divorce from a larger, supra-national economy before; nobody really knew how any of this was going to work, and by many accounts, we still don’t as it appears that we’re months away from Article 50 being triggered to actually begin Brexit negotiations. But when the Bank of England offered extreme-dovish policy in the wake of Brexit, coupling that brute uncertainty around the referendum with ultra-loose monetary policy implications, there was very little reason for anyone to want to buy GBP. This is what led to the flash crash on October the 6th; there was simply no demand, with few meager bids to counter the selling pressure on a Friday - and prices collapsed as overarching supply diminished what little demand might have existed.

Chart prepared by James Stanley

As demand bottoms, so does price. And as prices were forming a bottom throughout October, bears persistently sold the pair at resistance around 1.2300; and this formed a range-like formation in GBP/USD for the final three weeks of October. But while this range was developing, something else related to that massive drop in Sterling prices began to show…

Chart prepared by James Stanley

Ahead of the Brexit referendum, Mark Carney had warned us. Months ahead of the vote, Mr. Carney had said that a decision to leave the European Union would entail a ‘sharp repricing’ in the value of the British Pound, higher unemployment, higher inflation and slower growth: Basically a cocktail of economic demise. This would put the Central Bank in the unenviable position of having to choose how to mold policy. Should the Central Bank try to keep inflation at bay while keeping the currency relatively-strong? Or should the bank look to cut rates to kick-start growth, running the risk of higher rates of inflation while the currency drops in value. So we were warned.

And just days after the Brexit referendum, Mark Carney called an impromptu press conference to announce that the Bank of England would not hesitate to cut rates. A month later, the Bank of England launched another ‘bazooka’ of stimulus, and this served to drive GBP even-lower.

But after this ‘sharp repricing’ in the value of the British Pound, companies importing products to the U.K. began to notice. If the British Pound drops 20% against the U.S. Dollar in four months, companies importing goods into the U.K. see their margins get hit dramatically. If Apple is selling MacBook’s for £2,000; they’re bringing back approximately $3,000 to the United States as of June. Four months later, that same £2,000 MacBook is now bringing back approximately $2,400. In four months, Apple took a hit of $600 on every single MacBook sold.

This is significant: In many cases, a 20% hit to margins is the difference between profitability and losing money. To offset this impact of falling currency prices, we’ll usually see companies raise sales prices. This is the starting blocks of inflation, and it usually takes some time to continue pricing-through an economy, but once it starts, it can be difficult to stop.

And this is what appeared to change the near-term behavior in GBP. At the Bank of England’s most recent Super Thursday batch of announcements, the bank began to change their tune on inflation, guiding future expectations-higher in response to the building momentum after the ‘sharp repricing’ in the value of the British Pound. The Bank of England made that announcement on November the 3rd, at which point GBP/USD broke-above that previously-established level of resistance and continued to run-higher.

Chart prepared by James Stanley

Since that top-side breakout in Cable in early November, matters haven’t really been the same. We did get one more support test of that prior zone of resistance, but even with a near-record move in the U.S. Dollar, the British Pound kept its pace, and was one of the few currencies that was stronger than the Greenback in the election-month of November.

To get a better look at the British Pound, we can pair it up against a currency that has shown some element of weakness of recent in the Japanese Yen. This pair has moved-up over 2,000 pips since the lows of the election night, and this may be a better example of GBP-performance since early November as this removes the bullish breakout in the Greenback from the equation.

Chart prepared by James Stanley

Conclusion

Does this mean that the British Pound is going to continue to go-up? No. Nothing predicts the future, whether it’s inflation, unemployment, trade figures or anything else. The future is always uncertain; but by collectively piecing together the aspects that we do know, we can begin to form a thesis. Those aspects are as follows:

- The British Pound experienced a ‘sharp repricing’ around the Brexit referendum

- This means that importers are going to take a rather significant hit to margins

- Businesses are rather pragmatic in that they don’t like to lose money

- Businesses will probably raise prices. This could lead to more inflation down-the-road.

- Demand has begun to build in the British Pound as it appears sellers are drying-up, and buyers are beginning to take control (as evidenced by last month’s strength)

- This morning brought even more evidence that inflation is continuing to run-higher

These elements have collectively-served to build demand; and that higher-demand is pushing prices-higher. So, yes, Brexit is scary and uncertain and, still, we don’t have many concrete answers for how this is going to be executed. But based upon the facts that we do know, this is a bullish market, at least for now, and traders will likely want to approach it as such.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX