Talking Points

- According to overnight swaps, there is a 0.5 percent probability of a hike at today’s BoE meet

- BoE meetings have become more accessible with simultaneous statements and quarterly reports

- Retail speculative traders have 1.6 times the shorts on GBPUSD and 2.95 times shorts on EURGBP

See how retail traders are positioning in the majors in your charts using the FXCM SSI snapshot.

In the past Bank of England rate decision were throw away events. The central bank has not altered policy in a meaningful way in years; and if there were no changes, the group gave little-to-no insight into its reasoning. We wouldn’t see a meaningful breakdown of reasoning and fodder to thereby speculate on future timing until the minutes were released two weeks later. How things have changed.

Following in the footsteps of the Fed, ECB and BoJ; the BoE has adopted the effort to increase transparency – and shape markets through forward guidance – by taking steps to boost communications. Now, a more meaningful policy statement is released alongside the decision with the vote count. This upcoming decision is even more remarkable though as it happens to fall on the Quarterly Inflation report release. This is the most insight we can garner from the central bank without an actual policy change.

Market Expectations

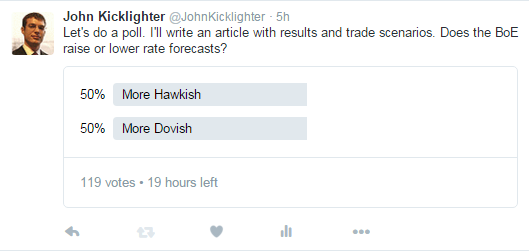

Heading into the event, what is the expectation for the outcome – which in turn sets the stage for how the market is positioned? Looking to overnight swaps, there is a staggeringly small probability of a surprise hike priced in (0.5 percent). The interest is not in whether they hike today, but ‘when’. We can measure that by assessing whether their bearing is more hawkish or dovish. With that in mind, I conducted a Twitter poll, and among the 119 traders that cast a vote by the time this article was written, half expected the BoE to be more hawkish, and half expected them to be more dovish.

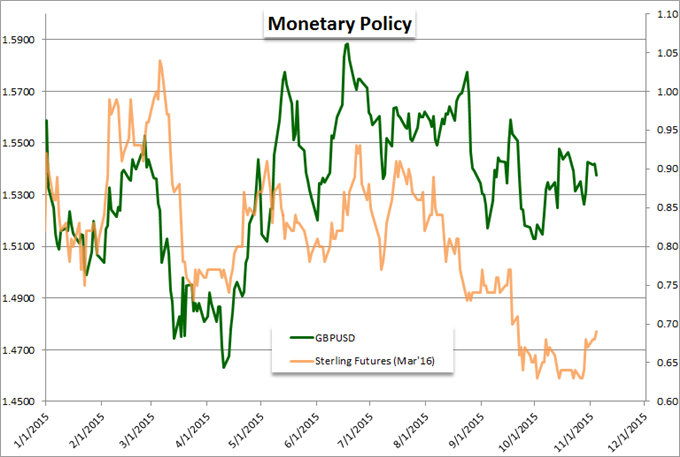

If the market is split on the outcome of a major piece of event risk, there is a hefty percentage of the ranks that will likely be caught by surprise and likely attempt to reposition for the update. How strong the speculative adjustment is depends on how clear the forecast comes through. That means we need to see evidence to push back or move forward the likely timeframe for liftoff. As can be seen below, the Short Sterling Futures contract for March 2016 has started to regain traction, but this hasn’t be a feasibly liftoff time frame from the market’s perspective since mid-September.

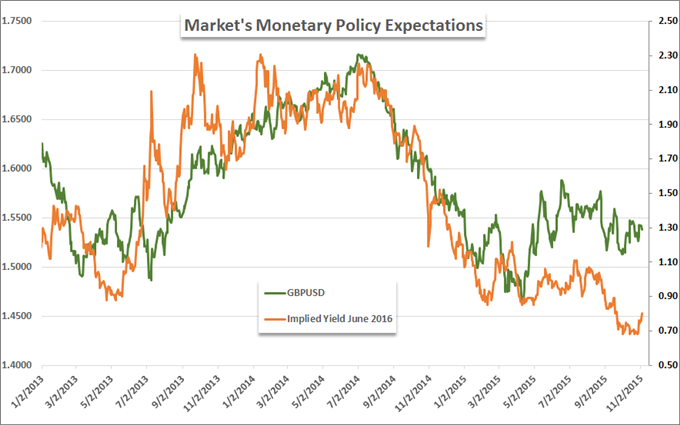

Looking further out the ‘curve’, the market once again believes that a hike will be realized by June 2016. This is still significantly more dovish than what was expected from the Pound in the previous years. Moving forward that time frame to something more commensurate with the Fed for liftoff and pace could generate a considerable amount of strength for the Sterling, especially against counterparts that are in a distinctly dovish position.

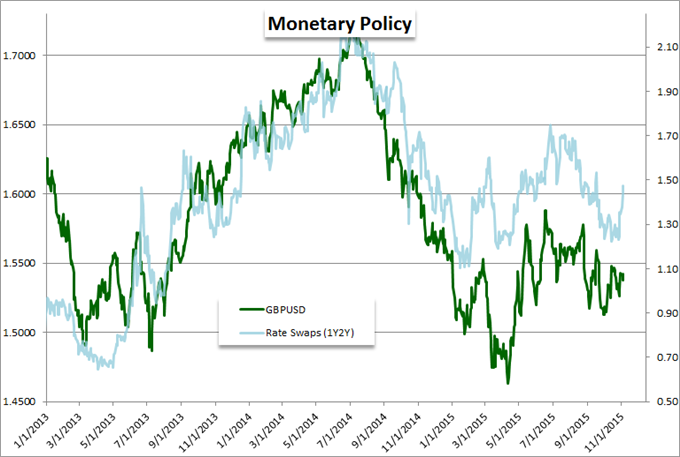

For pace, the 1-year-2-year swap suggests that the follow through after the first hike is also regaining traction. While the few central banks that are hawkish emphasize this path of tightening – versus just the timing of the first move – the market has yet to emphasize this view. That will change when the timing of liftoff for the US, UK and others becomes more certain.

What to Look For

In this more detailed event, there will be particular areas to look for rate speculation. The summary of the discussion will prove secondary to the vote count. Previously, there was one official that called for a hike while the balance (8) voted for no change. If this ratio changes, it will be a distinct hawkish or dovish shift.

A more comprehensive and longer view of monetary policy will come from the Quarterly Inflation report. This is similar to the Fed’s quarterly event where forecasts are upgraded – an exceptionally market moving event itself. Insight into the forecast for economic activity and inflation, notes on fears over external factors, appreciation for other policy groups’ bearings will tell us the BoE’s tolerances and thereby their likely time frame for tightening.

Pairs for Different Scenarios

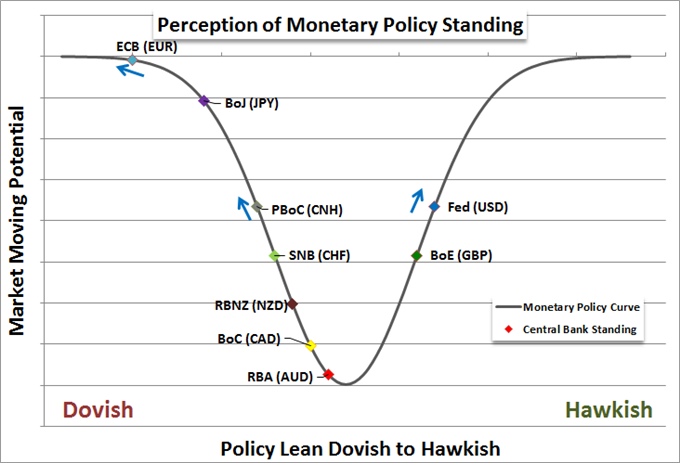

Not all pairs are created equal. Depending on whether there is a dovish or hawkish shift, there are will be pairs that are better positioned to take advantage of the change. Contingent on the direction, pairing the move to a more disparate counterpart will offer fundamental leverage to the development. Below we have the general monetary policy standings of the major central banks.

If the view from the Bank of England is downgraded, those pairings that are better positioned to take advantage of the development are not counterparts that are even more dovish. A delayed BoE rate cut does not represent an exceptionally weak position to a currency that is being guided by rate cuts or is under a major QE program. A ‘weak Pound’ view is best served against a strong counterpart. In the standings, the Dollar is the most distinct contrast with debate over a Fed hike in December heating up.

As we can see in the SSI Snapshot below, retail trader already have 1.61 times the number of long positions to shorts. That bullish bias would be significantly undercut if the BoE eases back on its view. This, it should be noted, is not an extreme reading for the GBPUSD SSI though.

Alternatively, if the BoE gives reason to upgrade the rate forecast, pairing a long-Sterling view to dovish counterparts will amplify the fundamental impact. On the Policy scale, the Pound stands above move. That said, one of the most dramatic contrasts can be made to the Euro. The ECB President this week followed up on their recent policy decision to reiterate the warning that they will revisit the question of a QE upgrade in December. Despite this disparity – already quite extraordinary – retail traders hold nearly three times the number of longs to short (2.98 SSI).