Point to Establish Short Exposure:Stop Sell Order on Break < 18.000

Spot: 18.05

Target 1: 17.600 100% Fibonacci Expansion of Late June-Early August Lower-High

Target 2:16.500 October – November Price Support

Invalidation Level:18.85 Friday (Post-Brexit) Close

To receive Tyler’s analysis directly via email, please SIGN UP HERE

The Summer of 2016 has been a boon for the risk-on crowd. Emerging Markets are a clear example of the move to risk-favoring assets that display a high relative yield. Since the morning after the ‘Brexit’ vote was finalized, the price of USD/MXN has fallen (the Peso has strenghened) by nearly 5%.

At the same time, US equities such as the Dow Jones, Nasdaq, and SPX500 have all traded at life-time highs in August. On Monday, the Russian Ruble traded at YTD highs and the Russian MICEX (equity index) traded at lifttime highs too.

Why do the all-time highs in equities and YTD in other EMFX pairs matter?

There is a broad-trend of Dollar selling (and very little USD Buying Pressure) and global push to into high-yield assets. One phrase that’s been tossed around is a barbell strategy of asset allocation that splits diversification between very safe assets and very risky assets.

As you might imagine, the MXN is a higher-yielding currency that is also positively correlated to the price of WTI Crude Oil (CFD: USOil) that has also been on a run-lately. The high-yield has been a large part of the appreciation in EMFX, and weakness in USD that this trade seeks to benefit from should the flows into high-yielding assets continue.

As of mid-August, Fed Fund futures are showing a pricing in of a Federal Reserve Rate hike at the February meeting following by another in early 2019. Should this expectation get pushed back, which seems to have been happening for the last year, the MXN may continue to beneift.

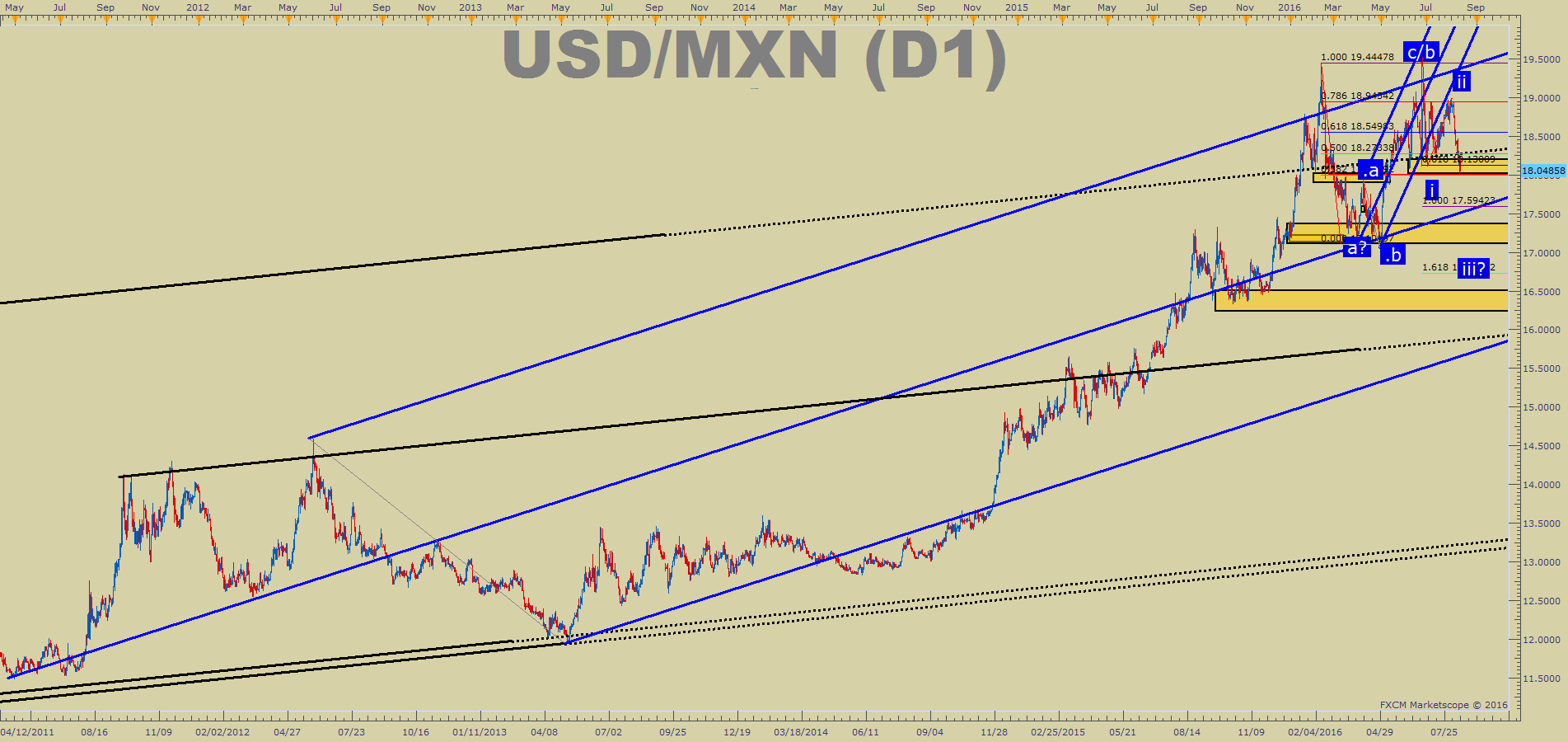

USD/MXN Could Begin Accelerating Lower Below ~18.000 Support

Key Technical Levels:

USD/MXN–Trying To Break Through Important Support of ~18.000

2nd Resistance: 18.620 Weekly R2 / 61.8% Retracement of AugustRange

1st Resistance:18.3712 Weekly Pivot / 38.2% Retracement of August Range

Spot: 18.05

1st support: 17.98 Weekly S1 Pivot Level

2nd support: 17.1000 April 29 Low

Trade Setup:

I am looking to sell USD/MXN on a close below 18.00. Initial targets currently sit at 17.100 and would be followed by a move down toward the late-2015 lows of ~16.5000. There is a 161.8% Fibonacci Expansion target that sits in the middle of those targets at 16.72732. A trailing stop would be used above an opposing up-fractal on the daily chart.

From an Elliott Wave perspective, USD/MXN looks to be in the early stages of a wave 'iii' of a larger 'C' wave. Such moves tend to be sharp and move aggressively against the prior trend to such a degree that they wash out the prior trends optimism. Should this anticipated wave count play out, the lower bound target of ~16.5000 could be exceeded.

The trade is aligned with a favorable risk: reward ratio that our Traits of Successful Traders report found to be one of the best things a trader can do to ensure long-term sustainability in your trading.