EQUITY MARKET OUTLOOK:

- S&P 500 begins the week with a positive bias after the U.S. central bank moves to restore confidence in the banking system

- The Federal Reserve establishes a lending facility for U.S. banks in need of liquidity following the fallout from SVB’s collapse

- What happened with Silicon Valley Bank and how did the crisis get out of control?

Most Read: Gold Price Shines as US Dollar Tanks on Sinking Yields from SVB Bailout. Higher XAU/USD?

The S&P 500 is rebounding on Monday, bolstered by sinking Treasury yields following the Fed’s decision to unveil a large loan plan to provide funding for struggling banks in the wake of last week's precipitous collapse of Silicon Valley Bank (SVB).

Before discussing the Fed’s actions, it is important to understand what happened to SVB and how we got here.

SVB SAGA

SVB’s was shut down by regulators last Friday and put into receivership for insolvency. Prior to its demise, the California-based lender had been in business for about 40 years, catering to a very specific clientele: technology and healthcare startups backed by venture capital and private equity firms. This meant an unusually high dependence on funding from a niche sector: the first red flag.

After the pandemic, when interest rates were pinned near zero percent to support the economic recovery and the world was awash in fiscal and monetary stimulus, SVB experienced exponential growth; in fact, financial records show that its deposits soared from $61.76 billion at the end of 2019 to $189.2 billion at the end of 2021.

As deposits outpaced loan issuance, SVB stashed the extra cash in bonds (Treasuries, mortgage-backed securities, etc.) to earn a return on capital, a common business model in the industry. However, the bank took this practice to a whole new level, perhaps assuming that borrowing costs would remain depressed for a long time, allowing its investment portfolio to swell to 57% of total assets, well above the 24% average among U.S. lenders.

When inflation made an unexpected appearance last year and began climbing at a breakneck speed, the Federal Reserve responded forcefully, launching its most aggressive tightening campaign in decades. The rapid rise in interest rates caused bond prices to plummet, given their inverse relationship, catching SVB, which had gobbled up huge amounts of fixed-income securities, wrong-footed and with massive unrealized losses.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

If bonds are held to term, a fall in their price due to adverse rate movements during their lifespan is meaningless, they are only temporary unrealized losses, as the nominal value of the investment will be fully recovered at maturity if there is no default. The problem for banks arises when they are forced to offload their holdings at a loss because of an urgent need to raise capital. This sealed SVB’s fate.

With the economy in weak health and interest rates at their highest level in 15 years, startups had been burning cash at a fast clip, steadily tapping their deposits to sustain their businesses in the face of an increasingly hostile and frosty fundraising environment. These companies were SVB’s biggest customers, so the situation was obviously problematic.

As withdrawals accelerated in the run-up to SVB's debacle, the institution had to shore up its finances quickly to stem the bleeding. For that reason, management had to dispose of a big chunk of the fixed-income portfolio at a heavy loss, declaring a $1.8 billion write-down on the sale of $21 billion worth of securities and announcing that additional measures may be needed to raise capital.

SVB’s actions shattered confidence and sparked panic, paving the way for a major bank run. When it was all said and done, depositors had initiated withdrawals of $42.0 billion from the institution by the end of Thursday, creating a negative cash balance of nearly $1.0 billion and leading to insolvency. This became the second-largest bank failure in U.S. history.

A similar fate struck Signature Bank on Sunday, with regulators closing the commercial lender after a torrent of deposit outflows.

WILL THE BANKING CRISIS SPREAD?

SVB's implosion was largely idiosyncratic: poor risk management and a highly concentrated depositor base contributed to the bank's downfall. However, the Fed's rapid hiking cycle also bears some responsibility, as it caused funding costs to reset higher, squeezing lenders. In this sense, the situation was beginning to become systemic, forcing the U.S. government to intervene.

WHAT DID THE FED DO AND IS IT ENOUGH?

The Federal Reserve on Sunday adopted emergency measures to shore up the U.S. banking system and avert a broader crisis after the second-largest bank failure in U.S. history. To stem fears of contagion, the central bank established a funding program, backstopped by $25 billion from the U.S. Department of Treasury to support depository institutions facing liquidity constraints and difficulties meeting their obligations to customers.

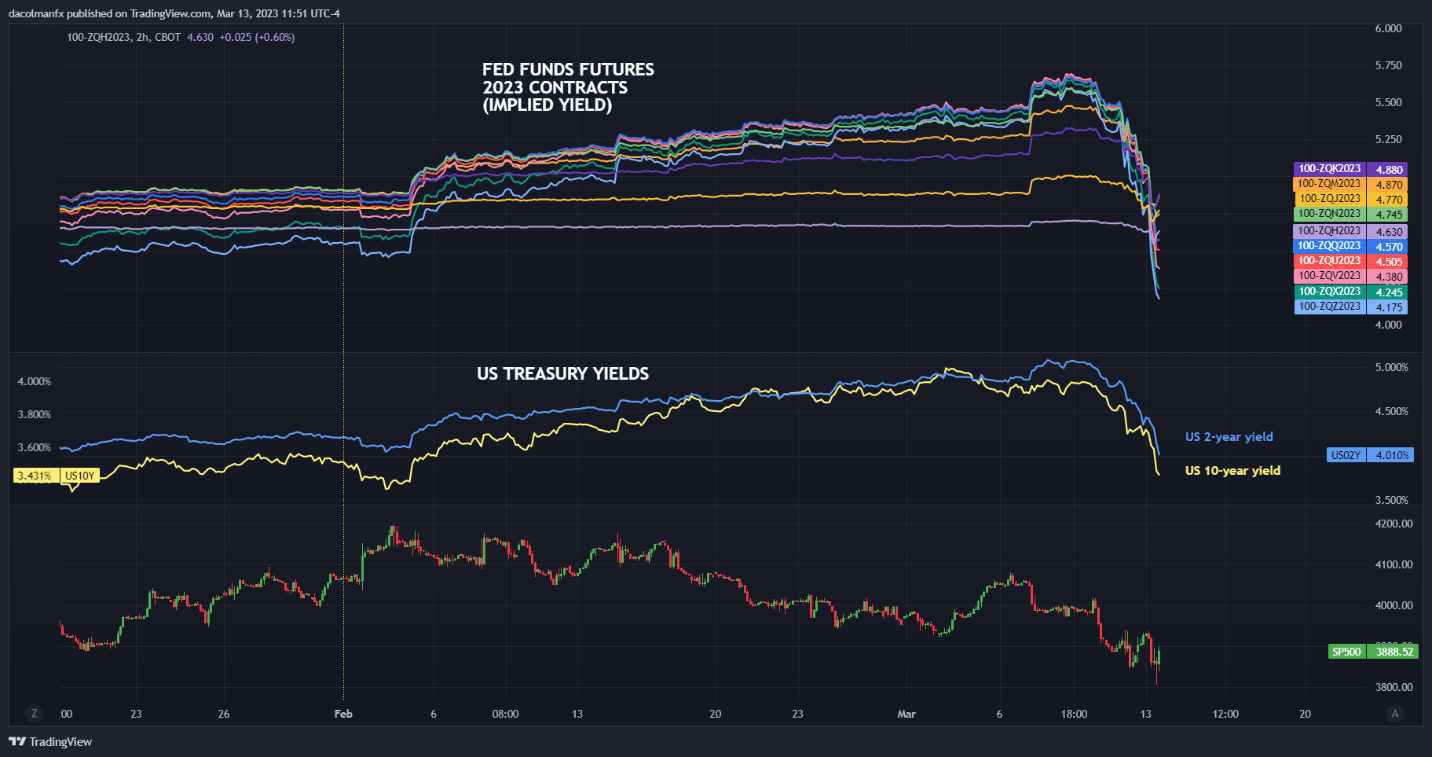

The Fed’s response has calmed some nerves, but its actions may be insufficient as bank stocks have continued to get battered. U.S. lenders, sitting on unrealized losses of $620 billion on their fixed-income portfolio, may need to raise more liquidity if deposit outflows keep increasing, so the system remains vulnerable.

On the other side of the coin, financial stress may prompt the FOMC to embrace a less hawkish stance and possibly pause its hiking cycle to prevent a “credit event”. We will find out more in the coming days and weeks, but for now, volatility is likely to stay elevated. Against this backdrop, the S&P 500 will remain on weak footing, with the index biased to the downside.

FED FUNDS FUTURES CHART VERSUS YIELDS