Indices Talking Points:

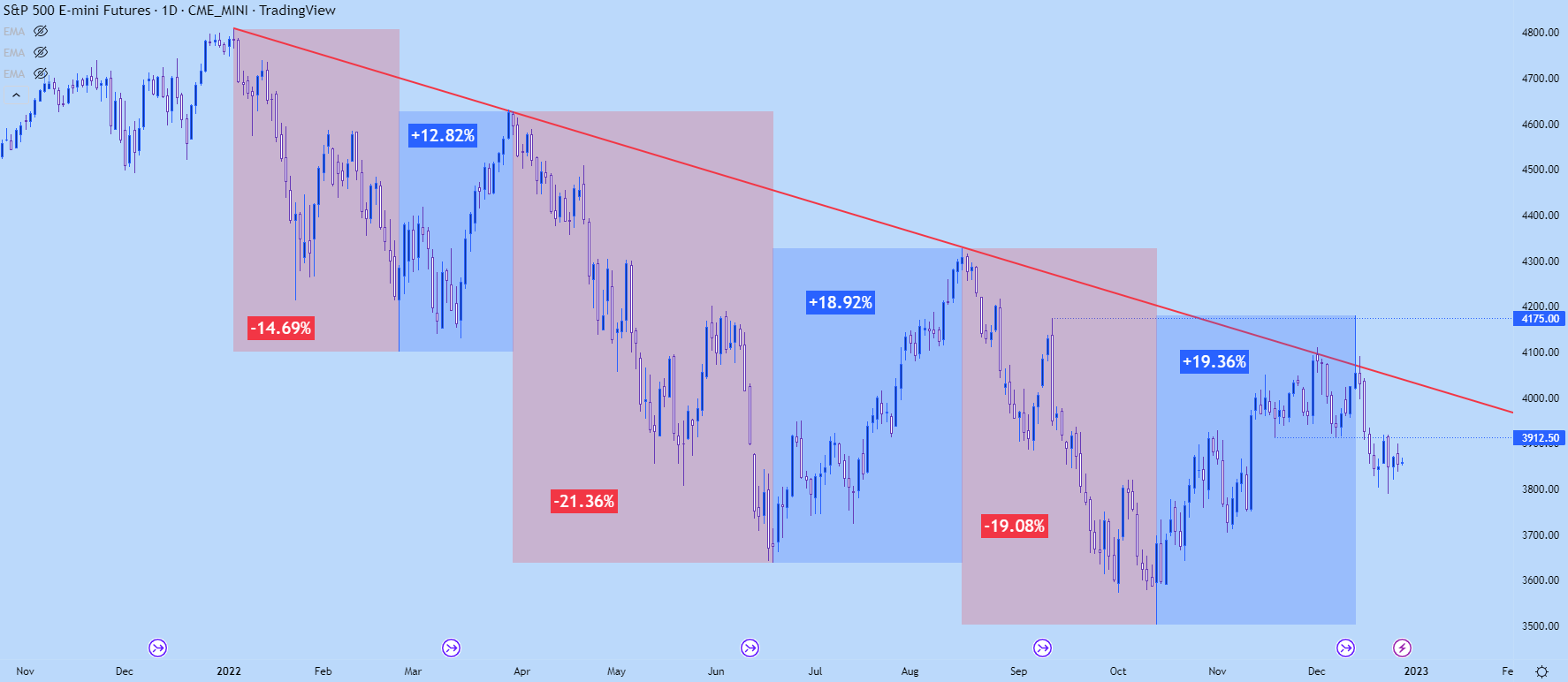

- The S&P 500 set its all-time-high on January 4th of this year after which bears went on the attack.

- The bearish theme came in waves this year even with a hawkish fundamental backdrop. The counter-trend moves from June-August and October-December were powerful, racking up 18.92% and 19.36% bullish trends inside of the overall 2022 trend that’s seen the S&P lose -19.76% on net (as of this writing).

- The big question for next year is whether the worst is over and whether the Fed is nearing a pivot. That doesn’t look to be the case from where we’re at, but things can change quickly, illustrated by the fact that Dec 2021 saw the Fed forecast 2-3 rate hikes for this year and by June, they were doing three 25 bp hikes at each meeting until December when the scaled back to a 50 bp hike.

- The analysis contained in article relies on price action and chart formations. To learn more about price action or chart patterns, check out our DailyFX Education section.

While 2020 was filled with the pandemic, 2021 was very much a response to the pandemic as re-openings around-the-world and massive stimulus outlays helped to keep economic growth running higher. But, also throughout last year there was the build of inflation that, for a long time, the Federal Reserve dismissed as transitory. The bank stood by and watched as CPI flared up to 3% and then 4%, eventually 5%. By the time we got to November of 2021, CPI had already scaled up to 6.2% for the prior month of October, and finally a shift began to show.

At his re-nomination hearing in November of 2021, Jerome Powell made a very public proclamation to ‘retire’ the word ‘transitory.’ This was seen as the head of the Central Bank waving the white flag on inflation, admitting that it wasn’t in fact transitory and instead would need to be countered with tighter economic policy rather than just standing idly by and hoping that matters corrected themselves.

Up to that point, the Fed had forecast one single rate hike in 2022. A form of lift-off, if you will, and that was highlighted in the dot plot matrix at the September 2021 FOMC rate decision. After Powell’s comment in front of Congress in November, it became apparent that change was afoot and at the December rate decision, the Fed bumped that expectation up to 2-3 hikes in 2022. Markets were still pretty unmoved, at least initially, as the S&P continued to work up to a fresh all-time-high.

But that feel good mood didn’t last for long into the New Year. The S&P 500 topped on January 4th and that’s when news of Russia lining the Ukrainian border with tanks started to take a toll. Inflation was already problematic, but the threat of disruption to Europe’s breadbasket made that quandary even more troublesome.

This led to some fast re-pricing in Q1 which, ironically, saw the S&P set its Q1 low on the day that Russia actually invaded (Feb 24th).

The S&P 500 held near the lows going into the March rate decision, with a strong rally developing in the back-half of the month after the Fed’s first hike. Then, as the calendar turned into Q2 bears were back in droves again.

Bears controlled the matter from the April open into the June FOMC rate decision, when the Fed went for their first 75 bp hike in 40 years. But, after that meeting is when the S&P started to rally, and then put in an 18.92% move over the next two months. That lasted all the way until August.

In August, Powell had enough of the bullish up-trend and made it a point to make his point at the Jackson Hole Economic Symposium. This triggered another bearish leg that ran all the way into October 13th. That’s when markets started to bounce in hopeful anticipation of some form of pivot. That led to a run of 19.36% from the October 13th lows into the December 13th highs.

Collectively, this has made for a banner year for swing traders as the S&P 500 has shown six different swings on the daily chart of more than 12% with four running more than 18.92%.

S&P 500 Daily Price Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

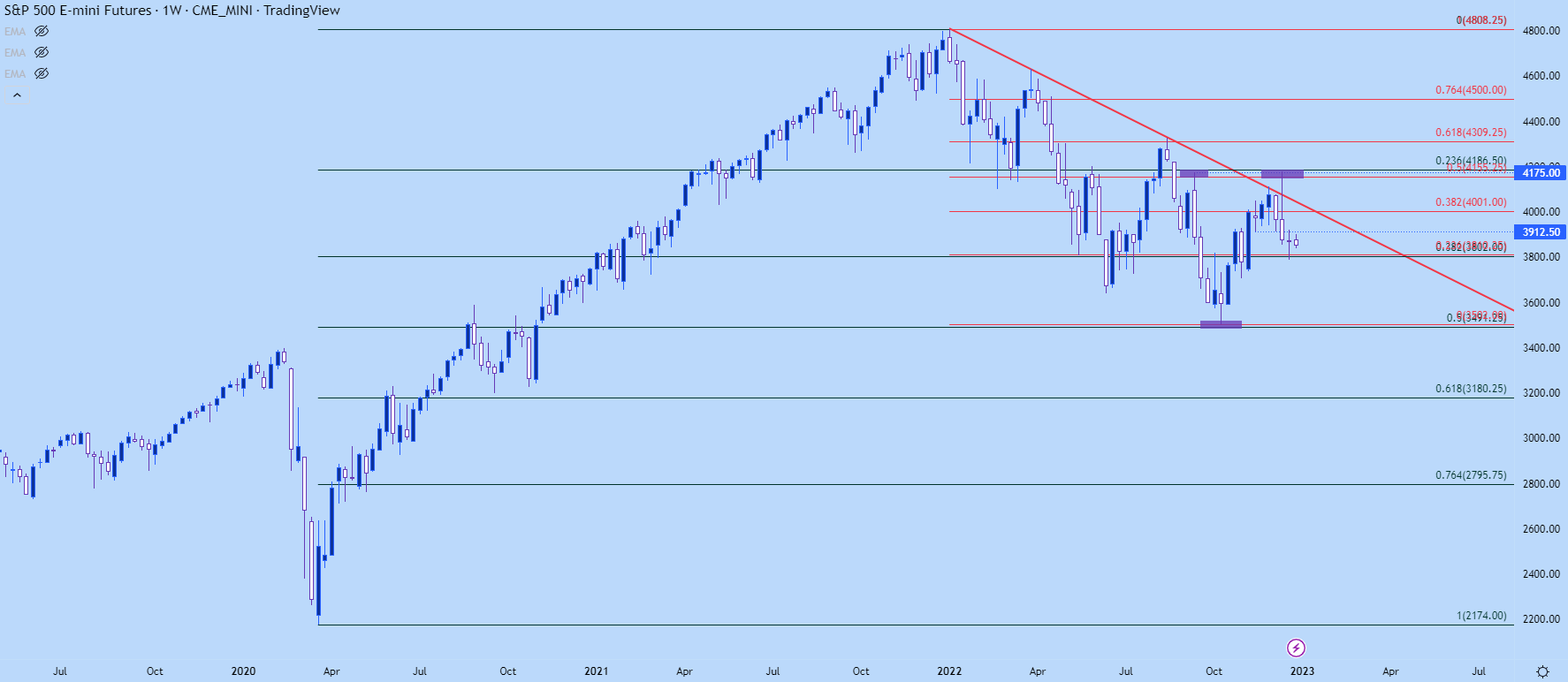

S&P 500 Longer-Term

Taking a step back, we can see a few levels of importance. The low for this year was just a couple of points above the 50% marker of the pandemic major move, which is around the 3500 level. That’s where the pivot on October 13th showed, on the back of a higher-than-expected inflation print. The fact that a counter-intuitive response showed there illustrates just how important that support was, as an oversold market was aggressively squeezed until there was a short-term bullish trend to work with.

That move ran all the way until test of the 50% marker of this year’s sell-off, which plots around 4155. This is confluent with the September swing high, setting up a possible double top formation, which is often tracked with the aim of bearish breakdowns, looking to the ‘neckline’ as the low point between the two tops.

Currently, the S&P is holding support above a confluent spot on the chart, plotted around the 3802-3810 level, which is both the 38.2% Fibonacci retracement of the pandemic move and 23.6% of this year’s sell-off.

S&P 500 Weekly Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

Nasdaq Leads Lower, Lags Higher

When markets contract, risk is punished and that’s on display in the tech-heavy Nasdaq, which has led the way-lower throughout the year while lagging on those bounce moves. Notably the Nasdaq topped in November of last year so that dynamic was already on display when we opened 2022.

But, even today, the Nasdaq is down by more than 34% from the January highs while the S&P is down a more paltry +19%.

And there’s a pretty clearly delineated spot on the chart that’s so far helped to hold the lows. This runs between 10,501 and 10,751, each of which are Fibonacci retracement levels, the former of which is the 61.8% retracement of the pandemic move. This bottom of this zone caught the lows in October and the top of the zone helped to hold the lows in November.

If sellers can force a breach in early Q1 trade, the next spot of support is at 10k, which is confluent as a psychological level that’s also a Fibonacci level. The pre-pandemic swing-high is a little lower, around 9763, so collectively this can mark a zone of interest for bearish continuation scenarios going into next year.

Nasdaq Weekly Price Chart

Chart prepared by James Stanley; Nasdaq 100 on Tradingview

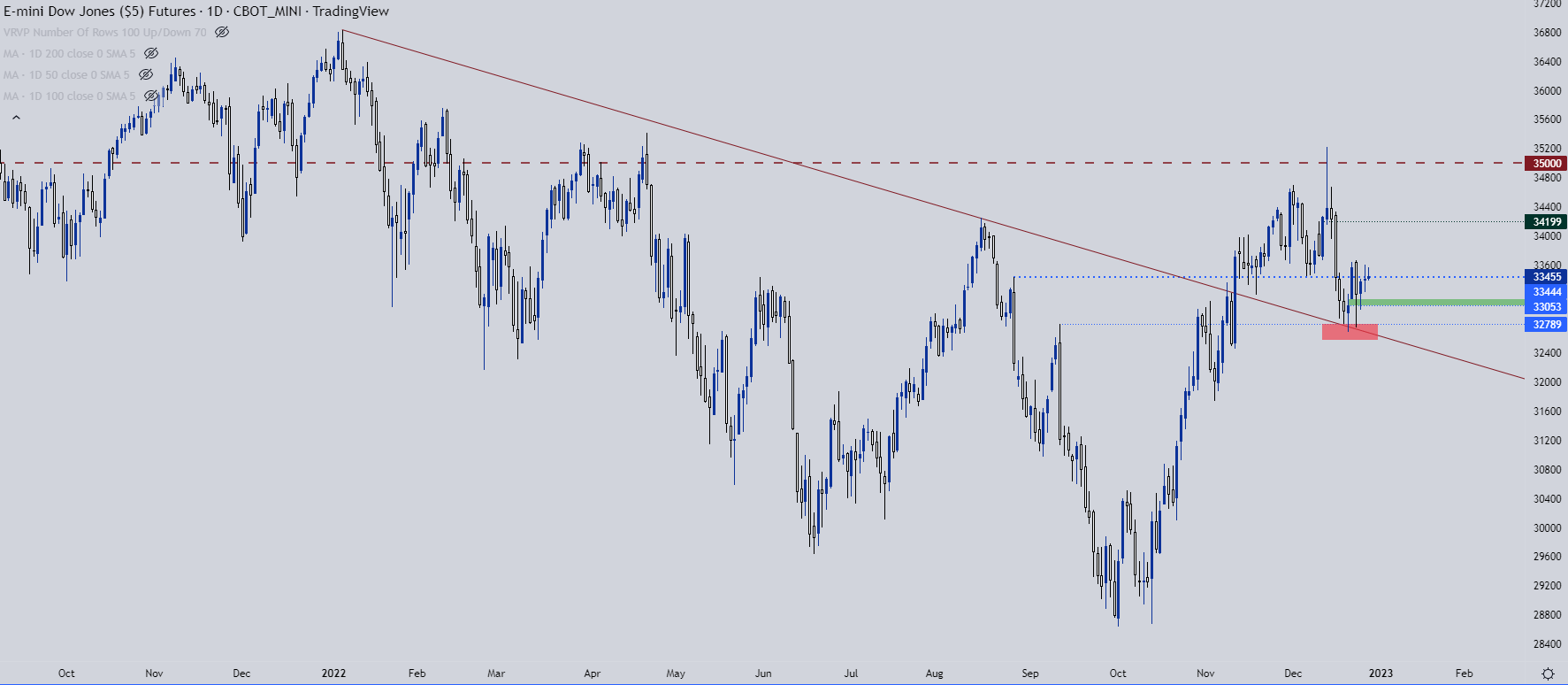

Dow

If you looked at only the Dow on net, you might not think that it was a very pensive year in stocks. At this point the Dow is down just about 9% on the year which pales in comparison to the -34% move in the Nasdaq or the -19% move in the S&P 500.

But, make no mistake, volatility was on full display here in 2022 and Q4 is where matters began to shift, as the Dow is up by 17% from its October low and at one point, was more than 23% above that mark.

At this point the Dow remains the cleanest shirt in the dirty laundry. The big question for next year is whether that’s enough for anyone to actually want to wear it. The index has held a key level of support over the past couple of weeks at 32,789, which was the September swing high that became confluent with a trendline projection last week.

Dow Daily Chart

Chart prepared by James Stanley; Dow Jones on Tradingview

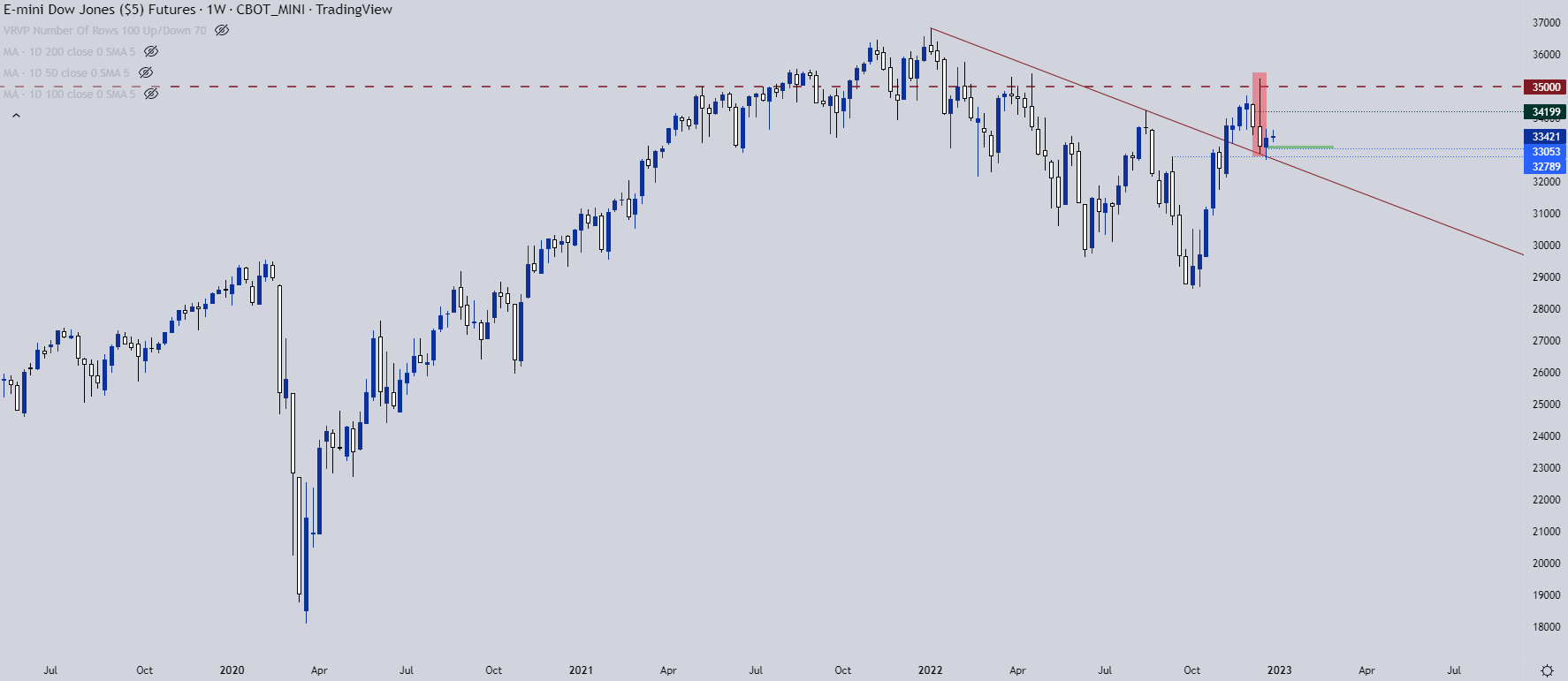

Dow Longer-Term

Taking a step back, and there could be justifiable reversal potential here, namely derived from the bearish engulfing pattern that printed a couple weeks ago. Bearish engulfs signal momentum changes and given short-term price action since the CPI print in December, this would remain a possibility going into 2023.

That resistance reaction happened at a very key spot, the 35k psychological level. And until bulls can take that out, bearish potential will remain as a possibility on a long-term basis, even if there is a case to be made for short-term strength.

Dow Jones Weekly Price Chart

Chart prepared by James Stanley; Dow Jones on Tradingview

--- Written by James Stanley

Contact and follow James on Twitter: @JStanleyFX