US Stock Market Key Points:

- TheS&P 500, Dow, and Nasdaq 100 churned for much of the session and finished lower as prices pushed into key supports.

- Investors continue to adapt for fear of a Fed-induced recession amid rising interest rates

- All eyes are on tomorrow’s University of Michigan Consumer Sentiment after the release of Euro-area inflation numbers.

Foundational Trading Knowledge

Macro Fundamentals

Recommended by Cecilia Sanchez Corona

Most Read: Thursday Market Outlook with Christopher Vecchio | Railroad Strike

U.S. equity indices were range bound for much of the session today but ended lower as investors digested a new set of economic data points that indicate weakening economic conditions in the manufacturing sector and cooling consumer demand. But additional information on the Economic Calendar reaffirmed the resiliency of the labor market, therefore consolidating the likelihood of a 75 basis-point rate increase at the next FOMC meeting.

After churning throughout the day, the Dow and the S&P 500 extended loses in the final hour and finished down 0.56% and 1.13%, respectively. Health, and Financials were the outperforming S&P sectors today. While improved outlook for Netflix and Wynn Resorts from the Consumer Discretionary segment bolstered sector gains, the prospect of rising interest rates boosted the Financials as they are expected to increase profit margins.

In contrast, some of the underperforming segments of the S&P 500 were Energy and Technology. Energy took another hit as the price of Oil continued to drop on Thursday. Concerns over supply have been overshadowed by prospects of lower demand ahead of a possible and significant hike in interest rates which could potentially induce a recession.

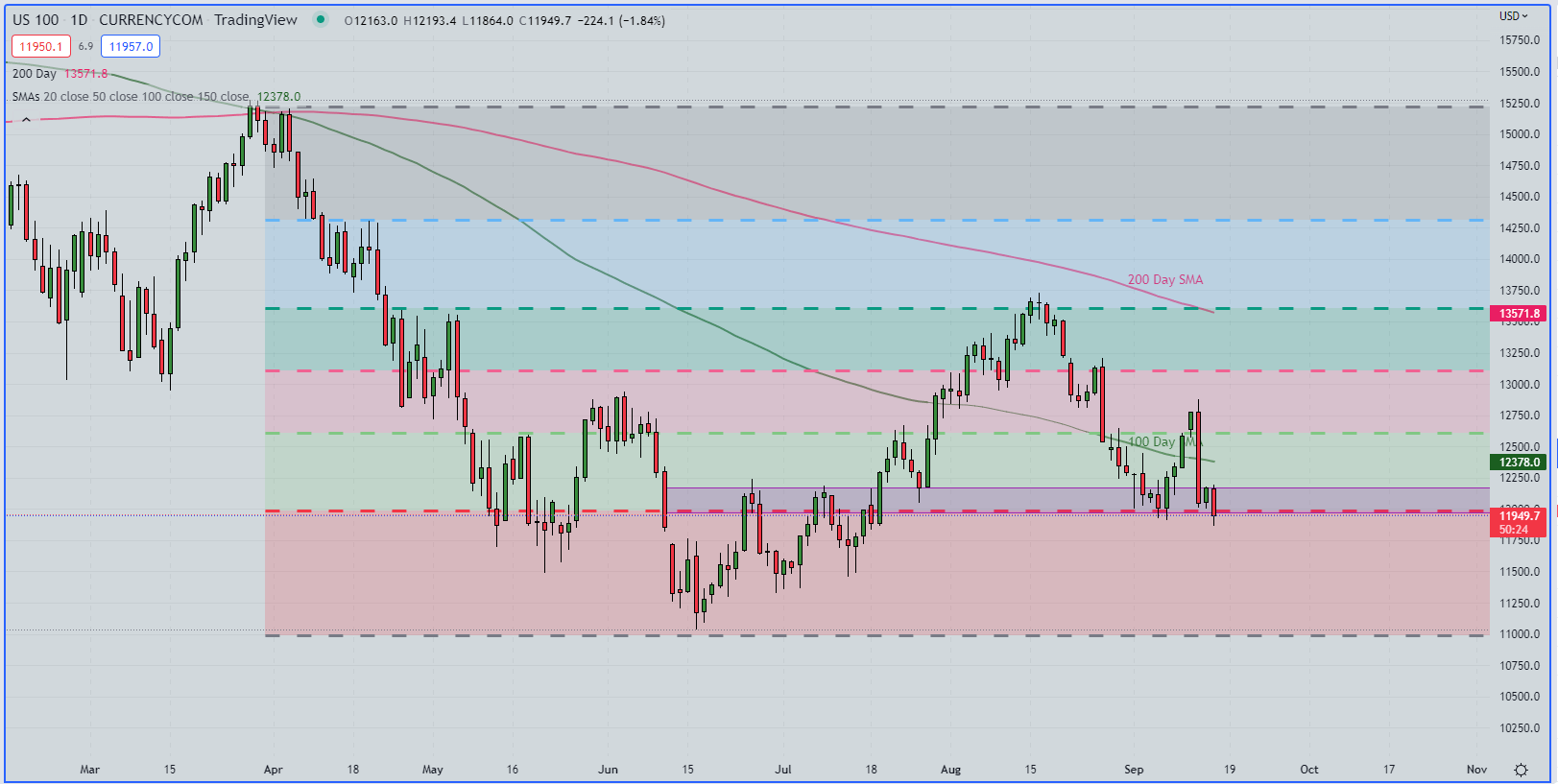

In a related manner, Adobe led losses in the Tech Sector. After announcing the purchase of a startup business while they released a mixed outlook for the fourth quarter, the stock price of the software company plunged by more than 16% today, their largest single-day loss since March of 2020. Likewise, the prospect of an induced recession amid rising interest rates also weighed on the technology sector, and as a result, the Nasdaq 100 pushed below support at the 12k level and fell 1.71% during the session.

Nasdaq 100 Daily Chart

Nasdaq 100 Daily Chart- Prepared Using TradingView

On the economic front, initial jobless claims continued to defy expectations as the number for the week ending in September 10 was better than anticipated, confirming the labor market’s resiliency. And this speaks to Fed hawkishness, as the bank has continually cited ongoing strength in the labor market as a factor in their decision-making processes. Even though the outcome could signal support for the consumer sector, August’s retail sales data depict a different picture.

While the headline figure exceeded expectations, they were negative when automobiles were excluded. Similarly, the prior month’s figure was drastically reduced from 0.0% to a negative 0.4% m/m, indicating a cooling in consumer spending.

In a similar vein, inflation and manufacturing activity also showed signs of deceleration today. Both the Empire State Manufacturing Index and the Philly Fed remained in negative territory, indicating weakening business conditions. Similarly, the prices paid index of the Empire State revealed a decrease in price growth. This new information has modified the implied expectations for the upcoming FOMC rate decision.

Yesterday, markets were pricing in a 34% likelihood of a 100 basis-points rate hike at the Fed’s meeting on Wednesday. Today, these expectations have decreased to 22% at the time of writing.

Looking ahead, all eyes are on tomorrow’s University of Michigan Consumer Sentiment and Euro-area inflation, which is set to be released ahead of the US open.

EDUCATION TOOLS FOR TRADERS

- Are you just getting started? Download thebeginners’ guide for FX traders

- Would you like to know more about your trading personality? Take theDailyFX quizand find out

- IG's client positioning data provides valuable information on market sentiment.Get your free guideon how to use this powerful trading indicator here.

---Written by Cecilia Sanchez-Corona, Research Team, DailyFX