S&P 500, FOMC, Dollar, GBPUSD and USDJPY Talking Points:

- The Market Perspective: USDJPY Bearish Below 146; EURUSD Bullish Above 1.0000; Gold Bearish Below 1,680

- The closely watched FOMC rate decision this past session offered yet another hefty 75bp rate hike while the policy statement seemed to offer dovish succor…until Powell reinforced the hawks

- A hawkish Fed will influence the market interpretation of the BOE rate decision as well as the US ISM service sector report and NFPs along with more systemic themes

The FOMC Throws the Market for a Loop

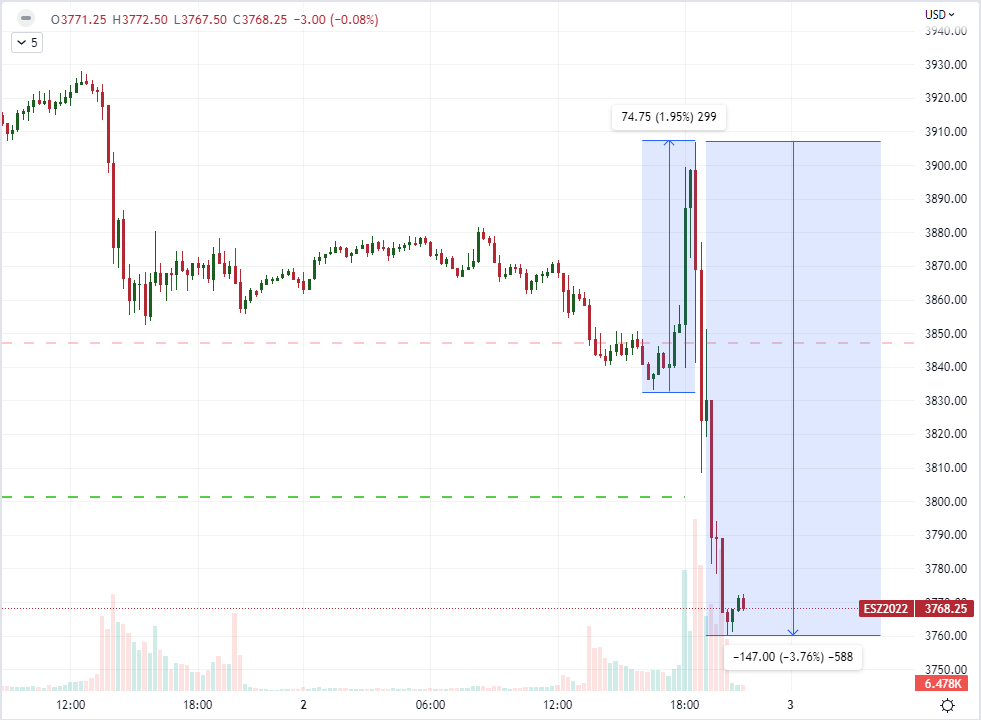

How can a 75 basis point (bp) rate hike from the Federal Reserve be viewed as a ‘mundane’ outcome? If the outcome is heavily priced in well in advance. That was the case with the fourth such hike of that magnitude in a row from the world’s largest central bank. Yet, the volatility that followed the event from the S&P 500 and Dollar (among other assets) indicates that the outcome wasn’t fully scoped by the market. While I am keeping close tabs on the continued tumble of the relative strength of the Nasdaq 100 (the ‘growth’ index) relative to the Dow Jones Industrial Average (the ‘value’ measure), my default convenient one-look measure of sentiment seemed to paint the picture all on its own. The S&P 500 in the immediate aftermath of the FOMC announcement of its 75 basis point hike to the benchmark range – 3.75 to 4.00 percent – experienced a hearty 2.0 percent rally from the lows established shortly before the release. Yet, after Chairman Jerome Powell’s press conference a half hour later, the collapse began with a second phase that measured an approximate -3.8 percent drop from the session highs. The question now is how far this adjustment stretches and whether it spill into the broader risk picture.

Chart of S&P 500 Emini Futures with Volume (15 Minute)

Chart Created on Tradingview Platform

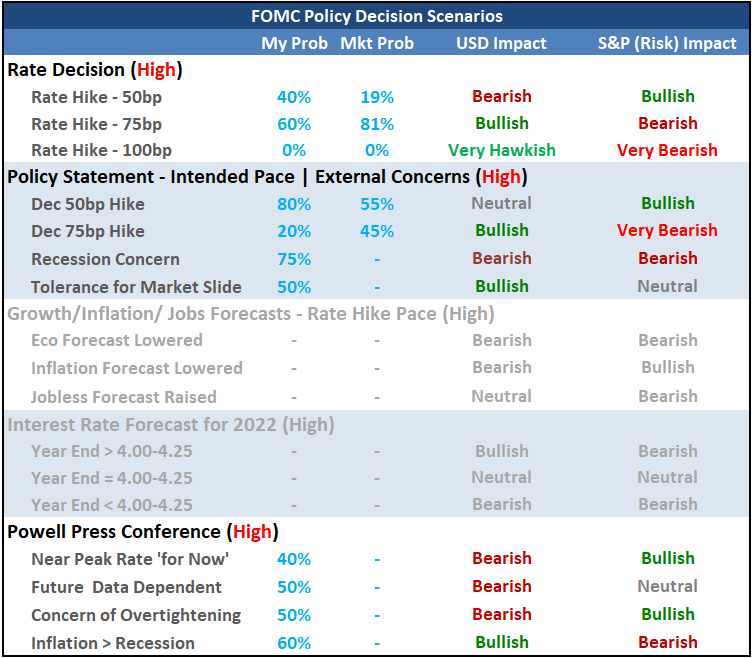

What was it about the FOMC rate decision Wednesday afternoon that warranted such an extreme market response? In general, it is those fundamental elements that are unexpected and realized that ultimately have the greatest influence over the market. So, while the fourth meeting with a 75bp rate hike is an extraordinary event in historical terms, the Eurodollar’s fully discounting the outcome and Fed Fund futures largely pricing it in meant that the outcome was generally priced in. The adjustment started to come in with the monetary policy statement released at the same time as the announcement on rates that added a section referencing “determining the pace of future increases…taking into account the cumulative tightening of monetary policy, the lags with which monetary policy affect economic activity…”. That is an ‘out’ for a hawkish central bank that will eventually have to step back from an aggressively hawkish pace, but the market would consider it an indication of imminent transition. If the event had ended there, the bullish glow could have persisted; but it clearly did not.

Table of FOMC Scenarios with General Influence on the Dollar and S&P 500

Table Created by John Kicklighter

When Fed Chairman Jerome Powell stepped up to the podium to begin his press conference, he dove right into the warnings over the importance of tackling inflation before it became a systemic problem. The markets have seen that rhetoric before and would have absorbed it without breaking the bullish assumptions if not for the subsequent clarifications in the Q&A portion of the presser. Initially, sentiment started to change when Powell remarked that there was still “some ways to go” while warning about histories lessons of loosening too early. He went on to say that the ultimate high water mark for rates was “higher than previously expected” and it was too premature to think or talk about pausing rate hikes. That translates into a likely path of more than two more hikes – though scale is open to interpretation. The peak rate in 2023 measured through Fed Fund futures certainly did push to new contract highs while the S&P 500 registered its worth FOMC day performance of 2022 with a 2.5 percent drop that clears some immediate technical support.

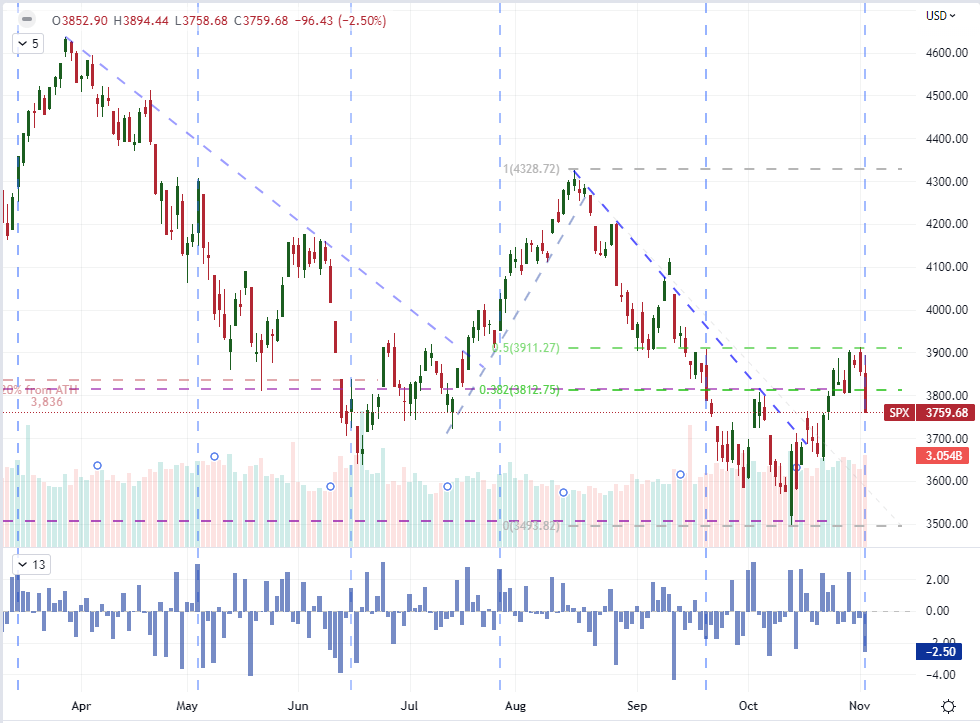

Chart of S&P 500 with Volume (Daily)

Chart Created on Tradingview Platform

USDJPY and Subsequent Event Risk: The After Effects of a Hawkish FOMC View

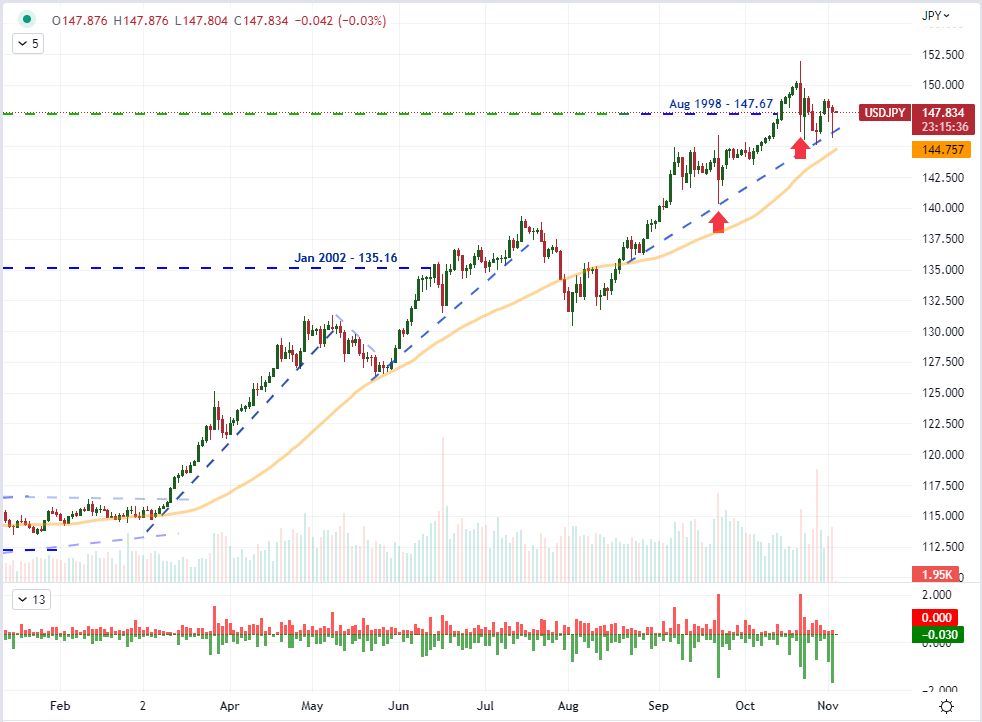

While many traders’ interest in the Fed rate decision (and other high profile events) begins and ends with short-term response to the stated outcome, there are serious after effects that we should account for going forward. An upgrade in the hawkish view from the world’s largest central bank translates into a marginal boost for the US Dollar against most of its major counterparts that are put at a greater marginal disadvantage in relative rate forecasts. The exception of course is USDJPY where the Bank of Japan (BOJ) left its own policy stance at the extreme opposite end of the spectrum last week with a maintenance of its zero rate policy and yield curve control. Japan’s authorities were likely hoping for some external relief from the principal counterpart since they are not altering course locally, but that has clearly been frustrated. The resultant response from the exchange rate was the biggest intraday reversal – leading to the biggest ‘lower wick’ – since January 2019. This may eventually pressure authorities to exact their next intervention effort sooner rather than later.

Chart of USDJPY (Daily)

Chart Created on Tradingview Platform

Another side effect of a relentlessly hawkish Federal Reserve is the skewed perspective it will lend to the market when absorbing the subsequent run of event risk and developments around systemic themes. Following the warnings made by Powell over the implications of unrelenting inflation, he went on to respond to a question that he believes the window for a ‘soft landing’ had indeed narrowed. That will intensify the scrutiny over recession signals – where many believe we have already navigated into the rough waters – while also putting greater onus on global counterparts in their own fights.

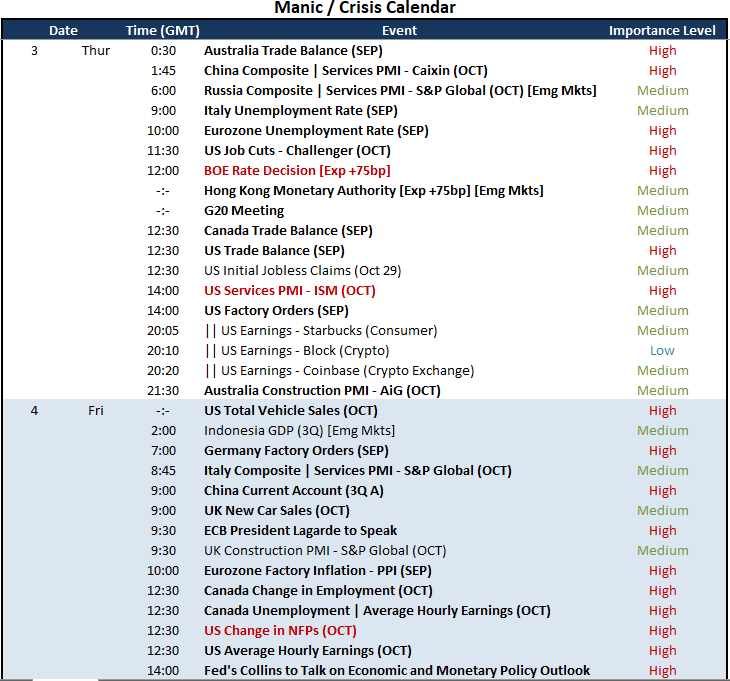

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

A Special Focus on GBPUSD and ISM Services

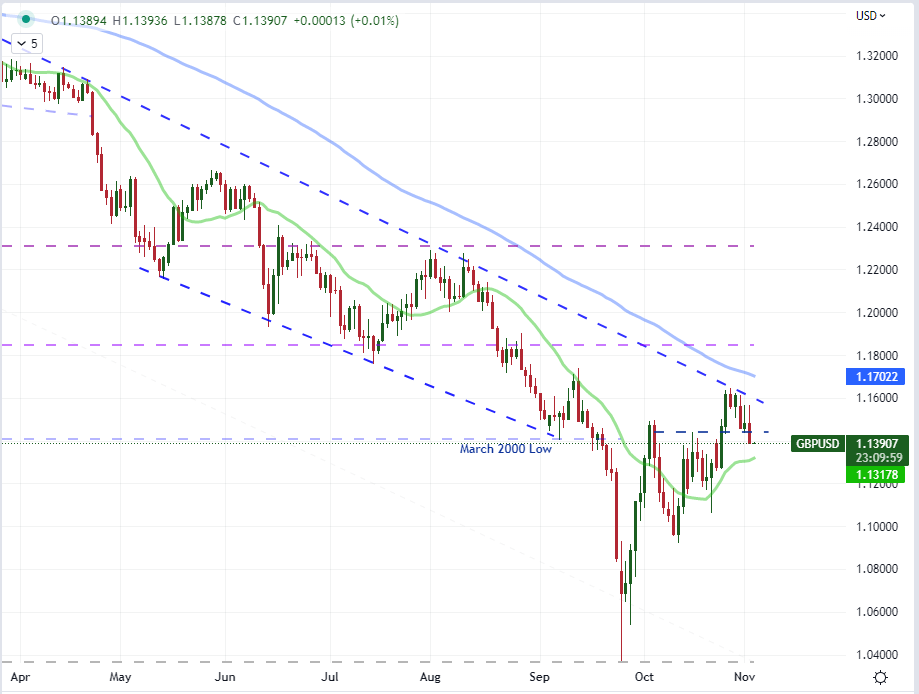

Looking further into Thursday trade, the backdrop of the Fed’s decision will make the forthcoming Bank of England (BOE) rate decision that much more interesting. Following a ‘disappointment’ by the central bank at its last meeting, the group is expected to hike by 75 basis points today in the London session – what would be the biggest increase in decades. If that move is realized it would not compliment the central bank’s own views that the economy is destined for a recession – if not already mired in the contraction. So, how would the Pound respond to such an outcome? Would it be a yield boost relative to the Dollar or a sign that central banks are being forced to cinch growth to combat unrelenting inflation?

Chart of GBPUSD Overlaid with 20 and 100-Day SMAs (Daily)

Chart Created on Tradingview Platform

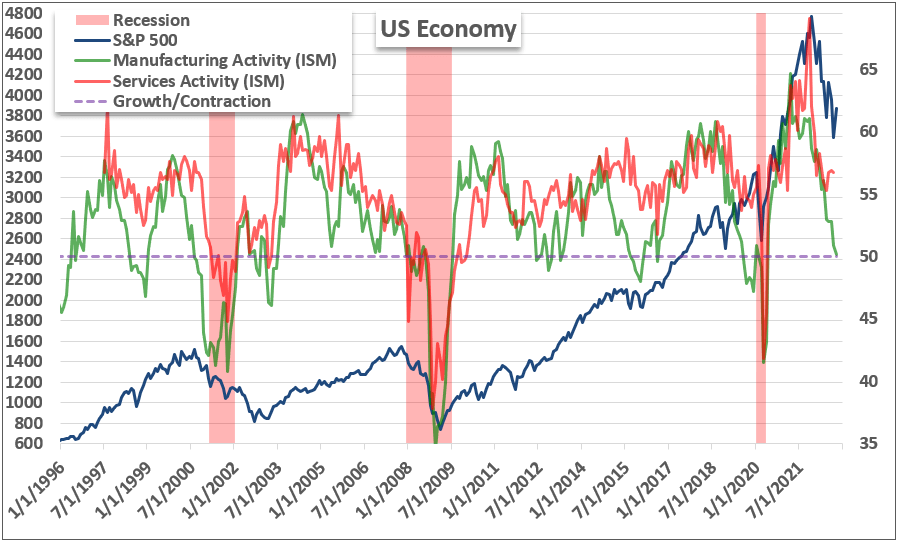

Another event that has gained in prominence in my estimation after the FOMC rate decision is the forthcoming ISM service sector activity report. Earlier this week, the manufacturing report slipped to 50.2 – marginally above the growth/contraction line and a cool reminder that the economic outlook is precarious at best. Yet, in terms of economic representation, factory activity accounts for approximately a quarter of output for the country while services account for three quarters of growth and jobs. If this figure manages to beat expectations, it will likely see its impact throttled, but a disappointment could hit hard. Keep in mind we also have the NFPs on Friday.

Chart of the ISM Service and Manufacturing PMIs Overlaid with S&P 500 and US Recessions (Monthly)

Chart Created by John Kicklighter with Data from ISM

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team