Deteriorating GDP Forecasts Aided by China’s Easing Covid Policy

Crude oil fundamentals will become even more of a delicate balancing act for producers, with the most prominent of these being OPEC+, as deteriorating global growth forecasts are weighed up against renewed optimism around China’s new reopening measures.

Most forecasting agencies whether it be a major central bank, the International Monetary Fund (IMF) or any other large institution anticipate lower GDP growth for 2023 on the back of a year that necessitated aggressive interest rate hikes. Higher interest rates remain essential in lowering inflation but also disincentivizes borrowing for expansionary projects and lowers general spending in the economy. In Q1 of next year, major central banks should near the end of the rate hiking cycle and embark on holding rates at elevated levels until conclusive evidence of lower inflation materializes or the economy heads into a tailspin.

However, China’s recent relaxation of its zero Covid lockdowns has provided a fresh wave of optimism for the economy of the world’s largest importer of oil and for general economic sentiment, which is likely to improve as a result. The table below highlights the modest oil demand growth figures and GDP estimates by OPEC, the Energy Information Administration (EIA) and the International Energy Agency (IEA), respectively.

Crude Oil Suffering as Central Banks Fight Inflation

An aggressive push from global central banks led by the US Federal Reserve to rein in a dramatic rise in inflation has translated to a sharp downgrade of the baseline economic growth outlook. A survey of economists by Bloomberg now puts worldwide GDP growth at just 2.5 percent next year, down from 3.6 percent as recently as early March.

The real yield on 2-year Treasury bonds rose from -3.01 to 1.77 percent over this period. This is as monetary tightening drove up nominal rates while pulling down priced-in inflation expectations. That puts the real cost of near- to medium-term borrowing within a hair of the 2018 peak at 1.9 percent. At the time this was reached, it was the highest level since early 2009.

The rapid rise in lending rates makes funding economic activity of every kind more expensive. It is then hardly surprising that expected growth rates have plunged, pulling cyclically sensitive crude oil prices down in tandem (albeit with a brief detour in early 2022 as the Russian invasion began). The Fed has loudly signaled unwavering commitment to continue brisk tightening in the coming months, keeping these dynamics in play.

Global Oil Demand Growth and GDP Estimates for 2023

| 2023 | OPEC | EIA | IEA |

|---|---|---|---|

| Oil Demand Growth(mbpd) | 2.25 | *1.16 | 1.7 |

| GDP Growth | 1.50% | **1.3% | ***3.6% |

| * According to EIA short-term outlook | |||

| ** Based on Oxford Economics Forecast | |||

| *** According to 2019-2025 growth assumptions based on IMF WEO |

OPEC+ Targets Further Supply Cuts in 2023, Biden Looks to Replenish SPR

OPEC+ continues on its current path of targeting output cuts of 2 million barrels per day (bpd) as it attempts to restore stability to the market after prices declined more than 40% since the March peak. After an initial impulse, WTI prices have actually continued lower until early December. In OPEC’s latest monthly report for November, the group confirmed the actual drop in output for the 10 OPEC members amounted to 744,000 bpd, well below its 1.27 million bpd share of the total 2 million bpd cut. Therefore, the total supply cuts appear not to be as bad as originally thought but this needs to be considerer alongside the anticipated loss of 1 million bpd or more of Russian supply as a result of recent EU sanctions and the $60 price cap. In Q1, accumulated output cuts may support oil prices.

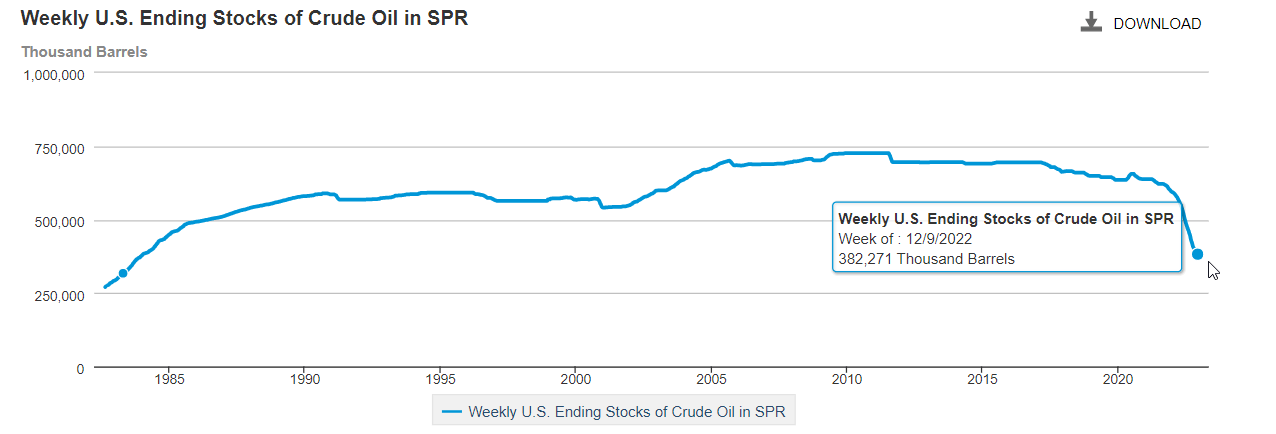

Potentially, there could be further wind in the sails for oil, as U.S. President Joe Biden expressed his willingness to step away from Special Petroleum Reserve (SPR) sales and look to replenish the stockpile which is likely to see a lift in oil prices. The Biden administration previously mentioned a preference to replenish stocks between $67 and $72 as SPR reserves reach multi decade lows. The most recent chart from the U.S. Energy Information Administration depicts just how sharp the near 180 million barrels drawdown has been on total reserves.

Weekly Chart of US Crude Oil Inventories in the SPR