Talking Points:

- Despite the retreat in US markets and President Trump's grievances, the market is still pricing in around a 70% chance of a hike

- An unexpected hold on rates would deliver the biggest Dollar impact and could earn a short-term bounce for the S&P 500

- Much of the focus will fall to the interest rate forecasts which are expected to severely reduce forecast for 3 hikes in 2019

Are you watching the FOMC rate decision and its impact on the market? You should. Join us as we cover it live starting 15 minutes before the actual policy decision. Sign up on DailyFX Webinar Calendar.

The Most Important Fed Decision Since Its First Hike Back in December 2015

The Federal Reserve is due to announce its final determination on its monetary policy bearings for the year later today. This is due to be the most important decision for the world's largest central bank since it began to actively tighten its policy back in December 2015. That hike was the first move to reduce accommodation in years - since the group started to rapidly cut rates in response to the greatest financial crisis and economic slump for the global economy stretching back to the Great Depression. The importance in that particular event was what it represented as a systemic course correction following years of the same bearing. If expectations come to bear at this meeting, it will reflect the same - though this time it will be a curb on a uniquely hawkish setting relative to its global peers. According to forecasts, the FOMC (Federal Open Market Committee) is still expected to hike its target interest rate range by 25 basis points at this meeting to 2.25 - 2.50 percent. That would be the fourth increase for the year which is an impressive pace even compared to previous cycles where other central banks were following their own hawkish path. Yet, the possibility that the Fed is forced to abandon this last move should not be written off. The probability afforded to this hike has been reduced from near certainty to around 70 percent according to swaps and Fed Fund futures. Forecasts for subsequent policy into 2019 is more explicit. Where the market preempted expectations of the three quarter-percent hikes the Fed eventually landed on in its September forecast, it is now showing that pace as near-impossible and serious debate of even a single hike over the year. The recent, sharp drop in capital markets has clearly had a serious impression in expectations.

FOMC Scenario Table

Which Component of this Comprehensive Event Carries the Most Weight?

As far as complexity goes, the upcoming Fed meeting is as multifaceted as they come. This is not just reflecting on what the policy officials themselves have to weigh in on, it is reference to the complication that speculative interests add to the event. For the Fed's part, the rate decision is perhaps the most straightforward element of the entire effort. Through the probability of a hike has dropped to approximately a 70 percent probability from near certainty just a few months before, it is still the presumed outcome. If the Fed wanted to cause the biggest jolt, it would announce no change to the benchmark rate, which would roil the Dollar and generate exceptional volatility for the S&P 500 (not just a straight light higher) which is why the Fed is unlikely to seriously entertain the option. Digging deeper, the monetary policy statement that accompanies all rate decisions will be something of a redundancy to the unique elements of this 'quarterly' event. Given the focus for the markets is forecasting the pace of tightening over the coming year and beyond, the Summary of Economic Projections (SEP) will be the most picked over aspect of this event. The central bank will update a range of forecasts which are important to monetary policy determination: growth, employment and inflation. However, it is the outlook for rates that carries the most direct influence. On that front, the chances that the Fed maintains its forecast for three hikes through the coming year as was projected at the September SEP is very unlikely. Swaps suggest even one hike over the coming year is only approximately a 40 percent probability - there must be serious concern over the economy and/or financial markets. Finally, there is Chairman Powell's press conference to consider. For many, this will be a write off as they will get what they think is most crucial in the rate decision and SEP. That would be a mistake. In his remarks, Powell will give reasoning and the criteria for which forecasting can change. He can also raise more systemic concerns like financial stability which is a theme that should be isolated.

Chart of Fed Rate Forecasts through June 19, 2019 from Swaps (Daily)

What the Dollar and Dow Will Take from US Monetary Policy

The Fed rate decision is important in economic and financial terms on multiple levels, but it will matter little to most unless it moves markets enough to create opportunity - or to strip it away. From the Dollar, there is a technical position that looks ripe for a breakout with even potential for either a bullish or bearish resolution. It would be exceedingly difficult to leverage a full-tilt Dollar rally. A hike alone would not earn the Greenback a charge that could clear any meaningful resistance as it is already the presumed outcome. The practical source of further bullish progress would be a hawkish rate forecast through the coming year. Maintaining expectations for three hikes in 2019 is a virtual impossibility according to swaps and other derivatives. Therefore, if this option is priced out of the market, seeing it come to pass would translate into favorable repositioning for the Dollar. Then again, the same scenario that could be presumably beneficial for the currency for modest yield advantage (another 0.25 or 0.50 percent yield over a year is not much in the grand scheme of things), could otherwise be the trigger to capsize risk trends. The S&P 500 and Dow have already slipped through technical support levels that could readily be described as critical to trend - 'necklines' on head-and-shoulders patterns. A genuine threat to growth and speculative reach could in turn prompt mass deleveraging. Alternatively, benefit for equities and other capital markets to be found in a pause in gradual monetary policy tightening is not likely to stand as serious foothold for persistent gains for capital markets. Slightly reducing the peak in lending rates has a material impact on access to capital, but it won't systemically alter the opportunity and risk appetite in the market that is already severely stretched. Then again, it may be enough to simply earn the seasonal December coasting that we have come to assume. We focus on the importance of this final Fed decision of the year in today's Quick Take video.

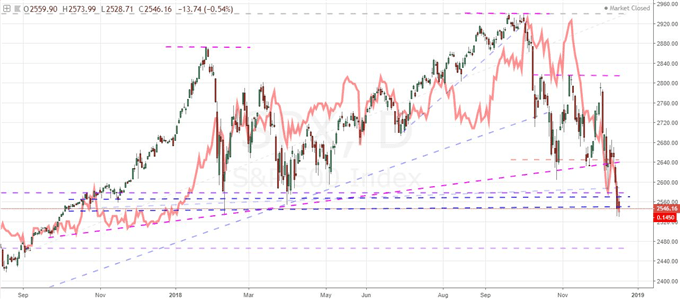

Chart of the S&P 500 and Yield Forecast Differential Between Dec and Jan 2019 (Daily)